Content available in English and Spanish (scroll down)

TTR DealMaker Q&A with Rebaza, Alcázar & De Las Casas Partner Alberto Rebaza

Alberto Rebaza – Rebaza, Alcázar & De Las Casas

Alberto Rebaza is founding partner and managing partner of Rebaza, Alcazar & De Las Casas law firm. Partner leads to mergers and acquisitions and corporate areas. In addition to his masters, he has studies at Georgetown University and England.

Alberto has been consistently considered by legal rankings as a leading lawyer in M&A, Banking and Finance. These publications include Chambers & Partners, IFRL 1000, Who’s Who Legal and LatinLawyer, among others. Also, Chambers & Partners called him “as the leading voice for large financial transactions and M&A”.

He has been a speaker at different conferences in Dublin, San Paulo, Bogota, Santiago, Panama City, Barcelona, NYC, Ciudad de Mexico, Bogota, Singapur, among others.

He has also been director in several companies and organizations such as Edegel (Energy), Rigel Peru (Insurance), Liderman (Services), Amrop (Services), IPAE, Pesquera Alexandra (Fishing), YPO, among others.

Very much involved in the arts world, Alberto is vicepresident of the Lima Museum of Art (MALI), member of the international patronage committee of the Museo Reina Sofia and member of the Latin American Circle at Guggenheim Museum in NYC.

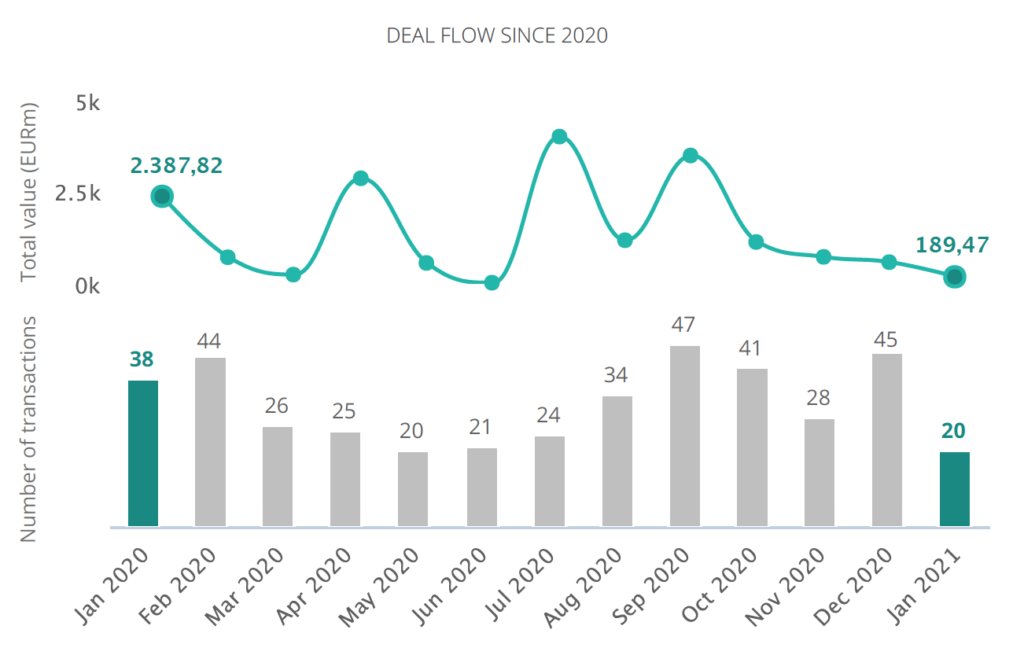

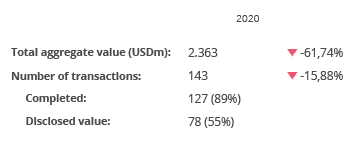

TTR: In 4Q20, M&A volume returned to ‘prepandemic’ levels in Perú, with a total of 27 deals. How do you interpret this upward trend compared to 2Q20 and 3Q20? What can we expect in terms of transaction volume in 2021?

A. R.: The increase of M&A transactions in 4Q2020 is the result of local economy reactivation, which was done in four phases and the last one began to be implemented in October 2020. The economic uncertainty decreased and allowed the resumption of M&A processes left on stand-by or processes that were slowed down in the previous quarters and the signing and/or closing of such transactions prior to the end of 2020.

An additional incentive for the parties to close M&A transactions last year was to prevent their process from being subject to a merger control process under the Peruvian law of merger control, which will likely come into effect within the 1Q2021.

Considering the new mandatory isolation imposed by the Peruvian Government and the uncertainty of its extension due to the health crisis, it is possible that M&A processes that began at the end of 2020 or this year, will slow down due to difficulties in providing information in connection with due diligence processes or to fulfill certain covenants for signing and/or closing. Also, the uncertainty regarding the beginning of the massive vaccination against COVID-19 and the Peruvian general elections that will take place in April may also slow down M&A transactions. However, it is possible that the large-scale transactions that have been negotiated, will be expedited despite the referred difficulties, in order to avoid the Peruvian merger control procedure and -maybe- being part of the first merger control procedure before INDECOPI, Peruvian public entity in charge of merger control review, in order to obtain authorization for closing.

TTR: Although financial services led M&A transactions in Peru, deal volume in the sector fell 16% relative to 2019. What is the outlook for this sector in the medium term, given the bullish prospects for Fintech in Latin America?

A. R.: The economy sector with the lowest negative variation compared to 2019 was the financial and insurance sector, followed by the real estate sector. Considering that approximately 70% of the Latin America population is unbanked or underbanked and also that fintechs have promoted the development of certain digital financial services for this target market, representing a significant challenge for financial institutions, it is possible that this sector will continue attracting interested parties for M&A or Venture Capital transactions. Regarding the latter, loans granted by fintech has gained a lot of momentum both in businesses funded by local investment funds, as well as large foreign banks. Also, new fintechs that give loans as an advance payment of salary are a very interesting alternative to bank loans of the same kind.

Financial institutions have as strategy to vertically or horizontally integrate startups that have developed financial products and services that complement their services and products. We have also seen the interest of venture capital funds or corporate venture capitalists to acquire equity or finance fintechs. For example, in 2018 we advised Grupo Crédito on their first investment in Culqi, a

Peruvian fintech and the following year we advised them on the second local investment of another Peruvian fintech, Wally.

TTR: Deal volume related to online businesses grew by 80% in 2020, bucking the general downward trend across all other sectors. What will be the main drivers of consolidation in this segment in 2021?

A. R.: The pandemic has raised awareness not only in large companies, but also in governments (for example, the Peruvian Tax Authority and Public Registries, among other Peruvian public entities, implemented automation and digitization of processes, among others) that there are deficiencies in the telecom sector and internal processes do not allow to provide services or offer products remotely.

Companies that were unable to carry out their activities remotely suffered heavy losses and implemented severe measures to try to counter the negative effects of the pandemic. However, companies that integrated their operations with new technologies and that were able to fully or partially develop their activities remotely, were seen as attractive in the M&A market. Some of the economy sectors that have had to adapt more quickly to survive are commercial stores and restaurants, which have devolped or contracted platforms for delivery. In the financial industry, at the corporate and personal banking level, great advances have also been seen in this regard.

The investment in equity of companies that provide digital services or that can contribute to the provision of B2C, B2B or B2B2C services is likely to continue growing this year and will be consolidated due to the need for other market agents to provide remote services in order to continue operating its business or integrate new lines of business that contribute to the development of its corporate purpose.

TTR: What are the prospects for the M&A market in Latin America in 2021? Which three sectors and which three countries will undergo most consolidation?

A. R.: The future of M&A transactions relies mainly, among other factors, on the massive vaccination against COVID-19. Some countries have already started the immunization process, while others -as Peru- are still awaiting the arrival of vaccines. This process will imply the beginning of resuming economic activities at pre-pandemic levels, which will lead to the recovery of the local, regional and global economy.

The industries that will have the most consolidation in terms of M&A transactions are likely to be technology, consumer and industrial activity. Main industries involved in the largest number of Latam M&A transactions in 2020.

The recovery of economic activities to pre-pandemic levels is vital in order to attract more activity in M&A. During 2020, in Peru, companies in the technology, financial and insurance, agribusiness and pharmaceutical sectors turned out to be the most resilient to the effects of the pandemic and companies in the distribution and retail sector, with adequate innovation, were interesting prospects for transactions of M&A.

Considering that last year Brazil, Mexico and Chile were the countries with the highest transaction volume, it is possible that such countries will undergo most consolidation. This in view of the implementation of the immunization process against COVID-19, which is the main factor affecting the economy nowadays. Another factor that impacts the M&A market is the lack of agreement on the valuation of businesses or assets; however, some companies are including within their budget and projections for this year the effect of the pandemic, which allows buyer to measure the risk of its investment and to sincere its expectations and the target’s value.

TTR: What will be the main challenges for Rebaza, Alcázar & De Las Casas in its M&A advisory work in Peru in 2021?

A. R.: Despite the pandemic’s negative effects (which is undoubtedly a factor that will continue to be a challenge in M&A transactions this year) and the political uncertainty due to the upcoming general elections, one of the main challenges in 2021 will be to implement the merger control mechanism in transactions. This new procedure will imply an increase in the transaction costs of the parties, because prior to the authorization (and the time that this implies), an economic and legal analysis must be carried out in order to determine if an application should be submitted -in order to obtain the approval of the transaction- before the Technical Secretariat of the Commission for the Defense of Free Competition of INDECOPI (Peruvian public entity in charge of merger control review) in case (i) the threshold established in the Peruvian law of merger control and its regulations that will be published within 1Q2021; or (ii) the buyer decides to voluntarily notify the transaction. Likewise, with this new regulation, transactions must include standstill provisions considering the the aforementioned regulations, such as limitations on the exchange of sensitive information, covenants on the conduct of the business until authorization is obtained, among others.

We are certain that our Competition – Antitrust team will provide legal advice with the standard of excellence inherent to our law firm- to all our clients interested in participating in M&A transactions that may be subject to merger control. We are very confident about succeeding in this new challenge due to our comprehensive preparation, which has resulted from analysis of regulations and doctrine of foreing jurisdictions with merger control systems, as well as meetings held with other regional actors with experience in merger control (i.e. Chile, Argentina and Colombia), and also the extrapolation -to this new regulation- of our know-how in matters of merger control applied to transactions in the electricity industry, in which we have provided legal advised advising to buyers.

Spanish version

Alberto Rebaza – Rebaza, Alcázar & De Las Casas

Alberto Rebaza es socio fundador y managing partner de Rebaza, Alcázar & De Las Casas. Es co-líder del área de fusiones y adquisiciones. En adición a su maestría en la Universidad de Virginia, cuenta con estudios en Georgetown University y en Inglaterra.

Alberto ha sido permanentemente considerado por los principales rankings legales como abogado líder en M&A y Banca y Financiamiento.

Ha sido expositor en conferencias en diferentes ciudades tales como Dublin, San Paulo, Bogotá, Panamá, Barcelona, NYC, Ciudad de México, Bogotá, Singapur, etc.

Asimismo, ha sido director en diversas empresas y organizaciones como Edegel (Energía), Rigel Perú (Seguros), Liderman (Servicios), Amrop (Servicios), IPAE, Pesquera Alexandra (Pesquería), YPO, etc.

Muy involucrado en el mundo de las artes; Alberto es vicepresidente del Museo de Arte de Lima, miembro del comité de mecenazgo del Museo Reina de Sofía y miembro del Latin American Circle del Guggenheim Museum en Nueva York.

TTR: En el cuarto trimestre de 2020, el número de transacciones de M&A en Perú ha vuelto a los valores ‘prepandemia’, con un total de 27 deals. ¿Cómo interpreta esta tendencia al alza con respecto al segundo y tercer trimestre del año?, ¿qué perspectiva podríamos tener para 2021?

A. R.: El incremento de operaciones en el cuarto trimestre del 2020 es el resultado de la reactivación de la economía local, la cual estuvo segmentada en cuatro fases y la última empezó a implementarse en octubre de 2020. La incertidumbre económica disminuyó y permitió que procesos de M&A que fueron dejados en stand-by en los trimestres anteriores se retomaran o procesos que estaban ralentizados, se cierren antes del término del ejercicio.

Un incentivo adicional de las partes para cerrar transacciones de M&A el año pasado fue prevenir que su proceso se encuentre sujeto a control previo en el marco de la Ley de Control Previo de Concentraciones Empresariales que, probablemente, entre en vigencia dentro del primer trimestre del 2021.

Tomando en cuenta la nueva cuarentena impuesta por el Gobierno Peruano y la incertidumbre de su extensión ante la crisis sanitaria, es posible que los procesos de M&A que se iniciaron a finales del año pasado o este año, se ralenticen debido a dificultades para proporcionar información en el marco del due diligence o para cumplir determinadas condiciones para la firma y/o cierre de la transacción. La incertidumbre sobre el inicio del proceso de vacunación masiva para inmunizar a los peruanos contra el COVID-19 y las elecciones generales que se llevarán a cabo en abril, también puede ralentizar las operaciones de M&A. No obstante, es posible que las transacciones de gran envergadura que se vienen negociado se agilicen a pesar de estas dificultades, a fin de evitar entrar al procedimiento de control previo de concentraciones empresariales y -quizás- ser parte del primer procedimiento frente a INDECOPI a fin de obtener la autorización para el cierre de la transacción.

TTR: Si bien el sector financiero y de seguros lideró la actividad de operaciones M&A en Perú, se reflejó una caída del 16% con respecto a las cifras de 2019 ¿Cuál es el futuro de este sector en el mediano plazo, teniendo en cuenta las perspectivas optimistas en el sector Fintech en América Latina?

A. R.: El sector con menor variación porcentual negativa respecto al 2019 fue el sector financiero y de seguros, seguido por el de real estate. Considerando que aproximadamente el 70% de la población de América Latina carece de una no tiene acceso o tiene acceso deficiente a servicios financieros, que las fintechs han impulsado el desarrollo de ciertos servicios financieros digitales para ese mercado objetivo y que ello representa un desafío importante para las instituciones financieras, considero que este sector seguirá atrayendo interesados para transacciones de M&A o Venture Capital. Con relación a esto último, el otorgamiento de préstamos por fintech ha tomado mucho impulso tanto en negocio fondeados por fondos de inversión locales, como grandes bancos de exterior. Otro punto interesante es la aparición de fintech que dan créditos en la modalidad de adelanto de sueldos, y que son una alternativa muy interesante frente a los créditos bancarios del mismo tipo.

Esto se suma a la estrategia de entidades financieras para integrar vertical u horizontalmente a startups que han desarrollado productos y servicios financieros que complementan los servicios y productos ofrecidos por las grandes entidades financieras. También hemos visto el interés de fondos de venture capital o corporate venture capitalists de adquirir equity o financiar fintechs. Por ejemplo, en el 2018 asesoramos a Grupo Crédito en su primera inversión en Culqi, una fintech peruana y al año siguiente los asesoramos en la segunda inversión local de otra fintech peruana, Wally.

TTR: Transacciones relacionadas a empresas cuya actividad se lleva a cabo por Internet crecieron en 80%, siendo el único segmento con un comportamiento al alza en Perú en 2020: ¿Cuáles serán los principales motores de consolidación en este segmento en 2021?

A. R.: La pandemia ha generado conciencia no sólo en las grandes empresas, sino también en los gobiernos (por ejemplo, a nivel de la automatización y digitalización de los procesos en la Administración Tributaria, Registros Públicos, entre otras entidades públicas) de que existen deficiencias en el sector de telecomunicaciones y procesos internos que no permiten prestar servicios u ofrecer productos de manera remota.

Las empresas que no pudieron llevar a cabo sus actividades de manera remota han sufrido grandes pérdidas y adoptaron medidas severas para tratar de contrarrestar los efectos negativos de la pandemia. No obstante, las empresas que integraron sus operaciones con nuevas tecnologías y que pudieron desarrollar total o parcialmente sus actividades de manera remota, fueron vistas como atractivas en el mercado.

Alguno de los sectores que han tenido que adaptarse con mayor rapidez para sobrevivir son las tiendas comerciales y restaurantes, las cuales han adoptado por desarrollar o contratar plataformas para pedidos por delivery. En la industria financiera, a nivel de banca corporativa y personal, también se han visto grandes avances en este aspecto.

La inversión en equity de empresas que provean servicios digitales o que puedan contribuir a la prestación de servicios B2C, B2B o B2B2C es probable que siga creciendo este año y se consolide debido a la necesidad de otros agentes del mercado de recurrir a servicios remotos para poder continuar con la prestación de servicios que es inherente a su negocio o integrar nuevas líneas de negocio que coadyuven con el desarrollo de su objeto social.

TTR: ¿Cuáles son las perspectivas del mercado M&A en América Latina para 2021?, ¿Cuáles pueden ser los tres sectores y los tres países con mayor fortaleza en términos de consolidación?

A. R.: El futuro de las transacciones de M&A depende principalmente, entre otros factores, de la vacunación masiva contra el COVID-19. Algunos países ya empezaron con el proceso de inmunización, mientras que otros -como Perú- aún están a la espera del arribo de vacunas. Este proceso implicará el inicio de retomar las actividades económicas a niveles pre-pandemia, lo cual conllevará a la recuperación de la economía local, regional y global.

Es probable que los sectores que tendrán una mayor consolidación en términos de transacciones de M&A sean el de tecnología, consumo y actividad industrial. Principales sectores involucrados en el mayor número de transacciones de M&A en el 2020 en Latino América.

La recuperación de las actividades económicas a niveles pre-pandemia es vital para efectos de atraer más actividad en M&A. Durante el 2020, en Perú las empresas del sector tecnológico, financiero y seguros, agroindustria y farmacéutico resultaron ser las más resilientes a los efectos de la pandemia y las empresas del sector distribución y retail, con una adecuada innovación, fueron prospectos interesantes para transacciones de M&A.

Considerando que el año pasado Brasil, México y Chile fueron los países con mayor volumen de transacciones, podrían ser este año los países con mayor fortaleza en términos de consolidación. Ello considerando la implementación del proceso de inmunización contra el COVID-19, que es el principal factor que afecta a la economía actualmente. Otro factor que afecta al mercado de M&A es la falta de acuerdo en la valorización de negocios o activos; sin embargo, algunas empresas están incluyendo dentro de su presupuesto y proyecciones para este año el efecto de la pandemia, lo cual permite al comprador medir el riesgo de su inversión y sincerar el valor de la compañía y las expectativas del comprador.

TTR: Para Rebaza, Alcázar & De Las Casas, ¿Cuáles podrían ser los principales retos en operaciones de M&A en Perú durante 2021?

A. R.: Dejando de lado la pandemia y los efectos negativos que ha generado (lo cual sin duda es un factor que seguirá siendo un reto en las operaciones de M&A durante este año) y la incertidumbre política por las próximas elecciones generales, uno de los principales retos en el 2021 será implementar en las transacciones el mecanismo de control previo de fusiones y adquisiciones empresariales. Este nuevo procedimiento implicará un incremento en los costos de transacción de las partes, debido a que de manera previa a la autorización (y el tiempo que ello implica), se deberá efectuar un análisis económico y legal a efectos de determinar si se presenta una solicitud de aprobación de la transacción ante la Secretaría Técnica de la Comisión de Defensa de la Libre Competencia de INDECOPI (entidad competente en materia de control de fusiones y adquisiciones empresariales) en caso (i) se superen los umbrales establecidos en la Ley de Control Previo de Concentración Empresarial y el reglamento que se publique; o (ii) el comprador decida notificar voluntariamente la transacción. Asimismo, con esta nueva regulación, las transacciones deberán incluir obligaciones de “standstill” considerando lo previsto en la normativa antes referida, como por ejemplo limitaciones al intercambio de información sensible, regulaciones sobre la conducción del negocio hasta obtener la autorización, entre otros.

Tenemos certeza de que nuestro equipo de Libre Competencia brindará asesoría legal -con el estándar de excelencia que es inherente a nuestra firma- a todos nuestros clientes que se encuentren interesados de participar en un M&A y se tenga que aplicar la nueva ley en materia de control previo a la transacción correspondiente. Confiamos plenamente en que nuestra preparación para afrontar este nuevo reto ha sido integral, lo cual ha resultado de análisis de regulaciones y doctrina de otras jurisdicciones con sistemas de control previo, reuniones con otros actores de la región con experiencia en control previo (i.e. Chile, Argentina y Colombia), así como la extrapolación -a esta nueva regulación- de nuestro know-how en materia de control previo de las transacciones en el sector eléctrico en las que hemos participado asesorando a partes compradoras.