Volume de Fusões e Aquisições sofre queda de 22% em 2020

Volume de transações no sector Imobiliário sofre redução 16%

Estados Unidos reduziram suas aquisições em Portugal em 67%

Volume de investimentos de Venture Capital sofre queda de 33%

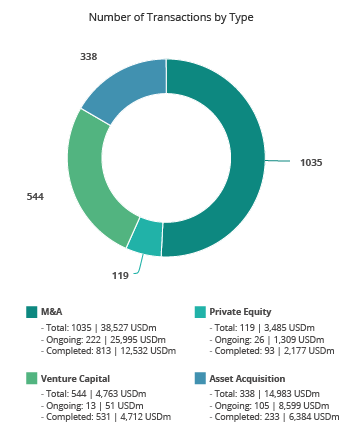

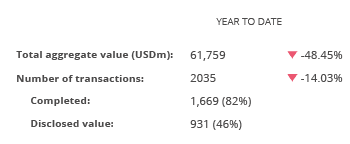

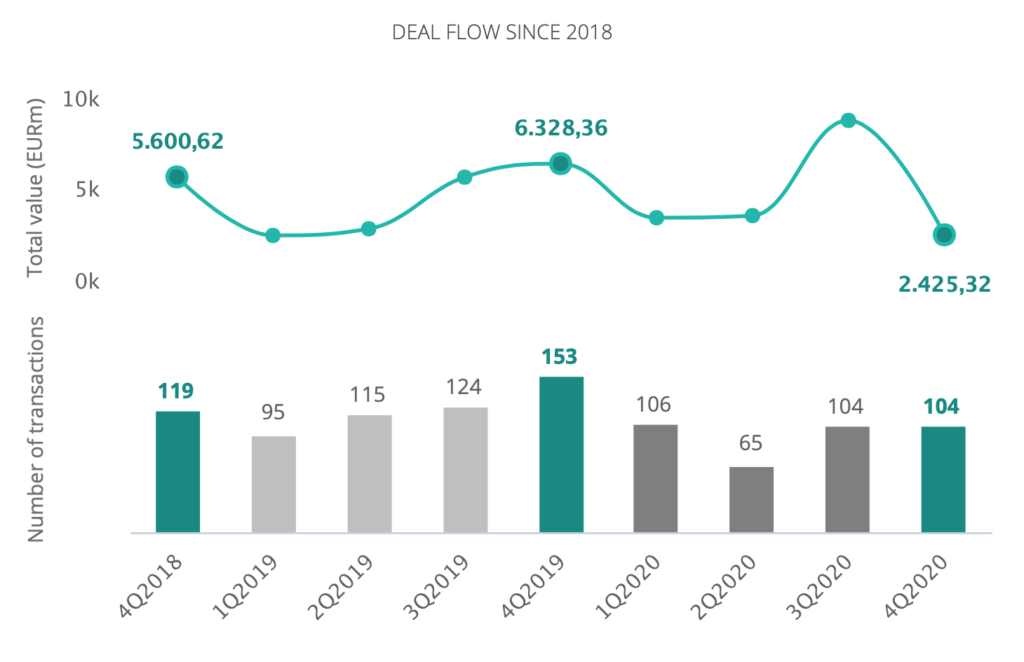

O mercado transacional português registou em 2020, 379 fusões e aquisições, das quais 182 tiveram valore divulgados que somaram EUR 18bi, segundo dados do TTR. Isto representa um aumento de 5% do valor movimentado e uma diminuição de 22% no volume de transações em relação ao ano de 2019.

No quarto trimestre do ano se registaram 104 transações, que apesar de representar uma redução de 32% em em relação ao 4T19, mantêm a tendência de alta observada no terceiro trimestre.

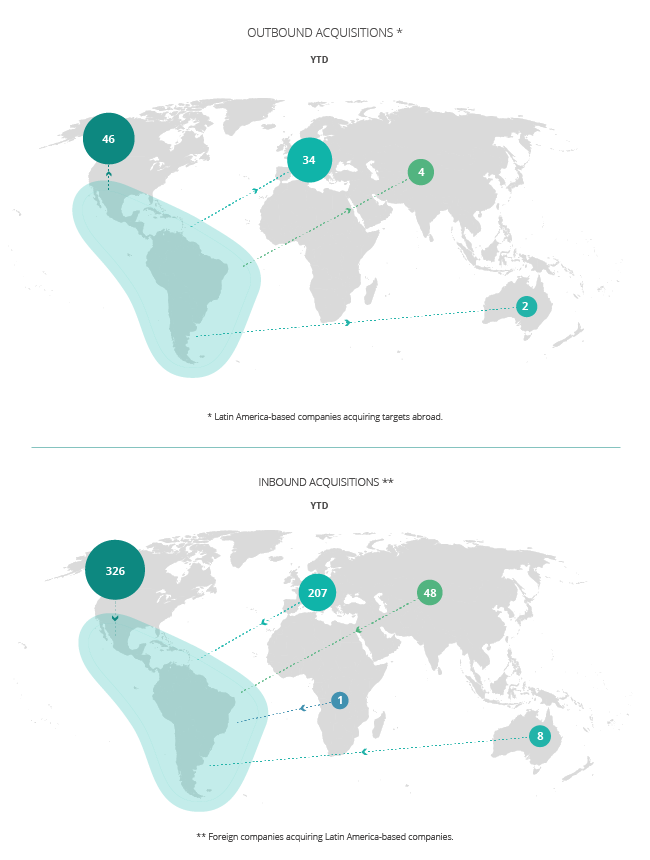

Âmbito Cross-Border

No que se refere às transações cross-border, houve uma redução generalizada na atividade em 2020, os Estados Unidos reduziram suas aquisições em Portugal em 67%, enquanto os Fundos de Private Equity e Venture Capital estrangeiros reduziram seus investimentos em Portugal em 33%, e até mesmo o sector historicamente mais atrativo para empresas estrangeiras, Tecnologia, sofreu queda de 13%.

A Espanha continua sendo o principal investidor em Portugal e esteve envolvida em 34 operações até o fim de dezembro, o segundo país que mais investiu em Portugal em 2020 foi a França com 22 transações, e o terceiro mais ativo foi o Reino Unido que esteve envolvido em 21 operações.

Em relação à atuação portuguesa no exterior, Espanha é o destino favorito na hora de realizar investimentos, com 16 transações registadas até o fim de dezembro. O segundo lugar onde Portugal investiu mais em 2020 é o Brasil com seis transações.

Private Equity

Em 2020, os fundos de Private Equity estiveram envolvidos em 29 transações, das quais 12 tiveram valores divulgados que somam EUR 4,2bi. Estes números representam uma queda de 41% no número de negócios e um modesto aumento de 3% no valor total.

Venture Capital

Os fundos de Venture Capital movimentaram um total de EUR 881m em 2020, aumento de 117% em relação a 2019. Foram 56 transações representando uma redução anual de 33%. O setor mais ativo foi o de Tecnologia com 27 transações, redução de 40% na comparação anual.

Transação do trimestre

A transação destacada pelo TTR no 4T20 foi a aquisição de 81,1% da Brisa, por parte do consórcio formado por APG, NPS – National Pension Service e Swiss Life Asset Managers. A operação do setor de infraestrutura movimentou EUR 2,4bi.

A transação contou com a assessoria legal em lei portuguesa dos escritórios Morais Leitão, Galvão Teles, Soares da Silva & Associados, VdA – Vieira de Almeida, Abreu Advogados e Campos Ferreira, Sá Carneiro – CS Associados ; A assessoria financeira ficou por conta da Caixa BI, Rothschild, Millennium BCP, EY Portugal e DC Advisory Partners.

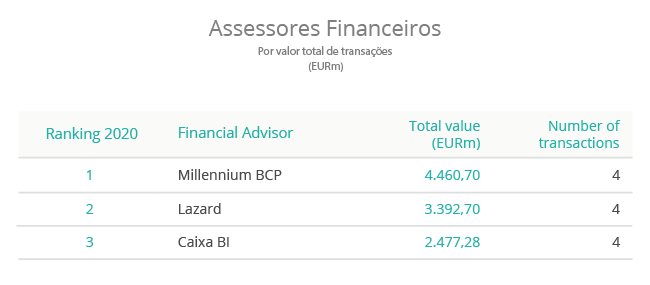

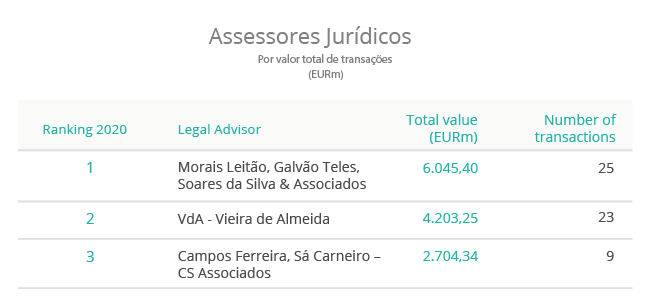

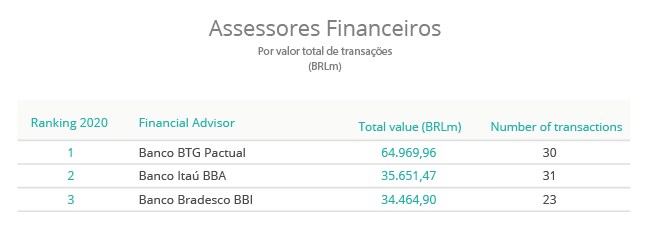

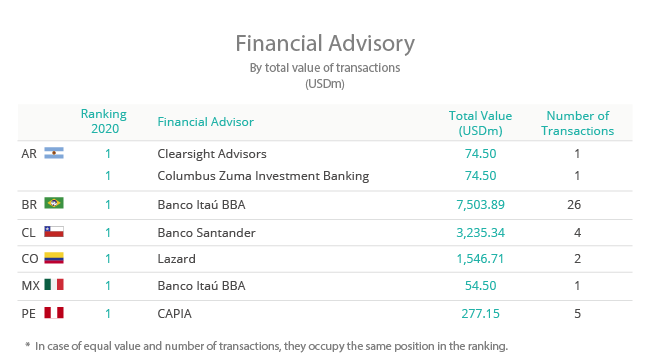

League Tables

O informe publica os rankings de assessores financeiros e jurídicos até dezembro de 2020 en M&A, Private Equity, Venture Capital e Mercado de Capitais, onde se informa a atividade das firmas destacadas pelo valor total das mesmas.