TTR y DLA Piper Martínez Beltrán publican el informe ‘Transacciones Corporativas en el Sector Salud’

Agosto 2020

Transactional Track Record (TTR), plataforma de inteligencia empresarial líder que provee información clave del mercado transaccional de la Península Ibérica, América Latina y el Caribe, en alianza con la firma legal colombiana DLA Piper Martínez Beltrán, han publicado el informe especial ‘Transacciones Corporativas en el Sector Salud’: un resumen que destaca las oportunidades, retos y perspectivas para Colombia en el mercado de Fusiones y Adquisiciones en el Sector Salud a través del conocimiento y la visibilidad de los dealmakers más destacados de este segmento en el país.

En el segundo semestre de 2021, TTR convocó al webinar, ‘Transacciones Corporativas en el Sector Salud’, en alianza con DLA Piper Martínez Beltrán, para destacar los cambios, desafíos y oportunidades que se presentan en este segmento clave del mercado colombiano.

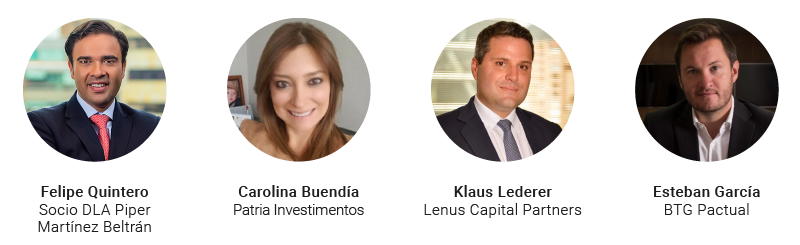

El informe especialTransacciones Corporativas en el Sector Salud’ presenta a algunos de los negociadores más destacados del país, incluidos la Operating Partner para el sector salud en Patria Investimentos y CEO del Grupo Avidanti – Grupo de Hospitales y clínicas en Colombia y Althea Colombia, Carolina Buendía; el Confundador y CEO de Lenus Capital Partners, Klaus Lederer; el s socio del banco de inversión de BTG Pactual, Esteban García, y el socio de DLA Piper Martínez Beltrán, Felipe Quintero, quienes han brindado una evaluación clave en el mercado de Fusiones y Adquisiciones en el sector salud, así como las oportunidades que puedan estar involucradas en el corto y mediano plazo en el sector salud colombiano.

El Informe especial tiene diversas secciones sobre la evolución del mercado transaccional colombiano en el sector salud en los últimos 48 meses, así como en el periodo de pandemia generada por la crisis sanitaria del Covid – 19. También incluye un resumen de las perspectivas de los invitados al webinar, así como el ranking legal de las firmas más destacadas en el mercado transaccional colombiano durante el periodo de la emergencia sanitaria generada en 2020 y 2021.

TTR’s Transactional Impact Monitor (TIM) is a Special Report combining local knowledge and market visibility from top dealmakers developed to address extraordinary situations affecting the macroeconomic stability and M&A outlook in core markets

INDEX

– M&A Outlook – Private Equity – Capital Markets – Handling the Crisis – Dealmaker Profiles

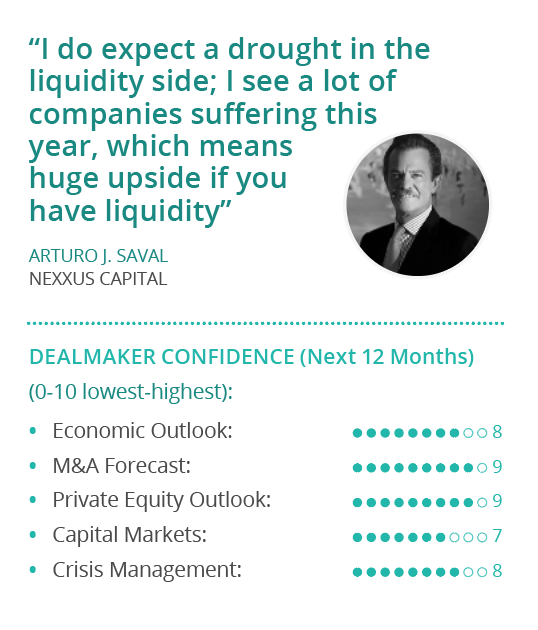

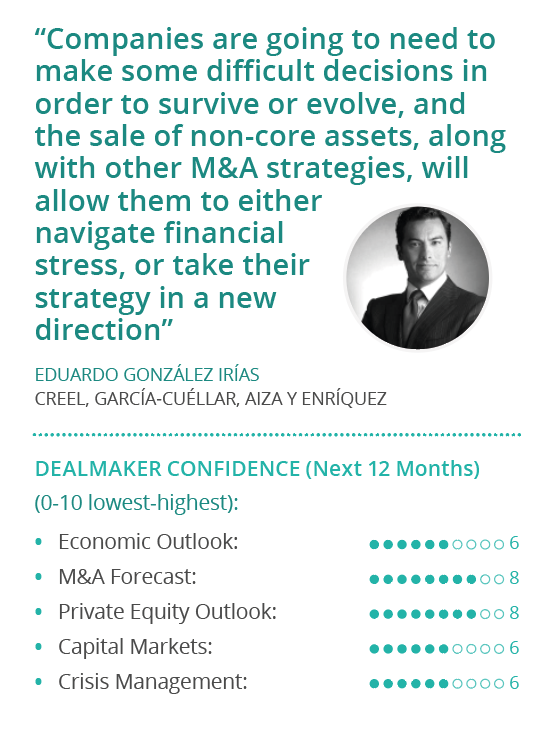

There is no doubt that 2020 has been one of the most challenging years in Mexico for decades, made all the more difficult by the slow reaction and absence of mitigating measures provided by the government, in contrast to most other nations.

“Mexico has endured a deeper recession because we haven’t had the government support,” said Nexxus Capital Founder and Chairman of the Board Arturo Saval. “I’ve never lived through anything like this.” Several sectors have been put under enormous stress, he noted, none more so than the country’s normally booming hospitality industry.

If there’s any optimism in Mexico’s business community as 2020 draws to a close, it’s relative to the dire pessimism that pervaded at the close of the first quarter, said Creel, García-Cuéllar, Aiza y Enríquez Partner Eduardo González.

There was great uncertainty over how the markets would react, González recalled, and many transactions that were on the cusp of closing were suspended as a result, some led by financial sponsors that relied on credit lines with local banks, others that depended on international financing. International lenders froze loan processing for several months, putting deals that relied on debt on ice, González said.

Mexico’s private sector has been damaged, and the health of the country’s financial system remains precarious, said Saval. Of Mexico’s 51 banks, 25 will have a very hard time, and some will shut down for good, Saval predicted, which will put extra pressure on the large ones that remain, many of which are based overseas and are facing stress in their home markets as well. “There will be a lot of stress in the banking industry globally, which will make them reluctant to increase their exposure in Mexico,” he said.

The downturn has affected deals in a range of sectors, from construction to chemicals and consumer products, with some proving far more vulnerable than others, González said. “We saw up close people trying to get out of signed deals, invoking force majeure events or breach of contract,” he noted.

The uncertainty clouded financial projections, with no assurance that companies would be able to maintain their revenue and EBITDA margins in an unknown economic climate, he added. “Nobody thought they’d be able to maintain their sales volumes; nobody knew how the world economy would work with everybody being asked to stay at home.”

There are sectors that have been severely affected, but many continue operating and the fall in sales and profitability hasn’t been as devastating as anticipated, which has resulted in cautious optimism, González said.

Some industries have indeed been flourishing, Saval noted, with the surge in e-commerce bolstered by Mexico’s lag in this area pre-crisis. The country is underleveraged compared to many of its peers in Latin America and state finances are in good shape, with the exception of the country’s national oil company Pemex, “mostly because of the position the government has taken”, Saval added.

Investment in Mexico’s energy sector has been impacted by the policy position of the Andrés Manuel López Obrador (AMLO) administration, which eroded investor confidence in the renewable energy market and put a damper on reforms passed by his predecessor, González explained.

Nonetheless, there are still investors out there for good assets, he said, and many, like China’s State Power Investment, which bought wind farm operator Zuma Energía in November, are accustomed to regulatory and political risks. The policy position of Mexico’s current government has made the energy sector less attractive, but renewable deals still command interest, he said. Similarly, appetite for Mexico’s road infrastructure among Canadian pension funds has also held up, González said, as evidenced by the recent sale of IDEAL.

Investment in conventional energy, on the other hand, faces tremendous hurdles, González said. “It’s difficult to understand the intentions of the government in areas that they themselves have politicized,” he said. “AMLO has consistently tried to make the petroleum industry a sacred cow for the people of Mexico for many years, and decisions governing the sector won’t likely be made based on any market intelligence, nor geopolitics, but rather for his own political benefit,” he added.

Transactional Impact Monitor: Spain & Portugal – Vol. 5

Posted on

Transactional Impact Monitor: Spain & Portugal – Vol. 5

1 December 2020

TTR’s Transactional Impact Monitor (TIM) is a Special Report combining local knowledge and market visibility from top dealmakers developed to address extraordinary situations affecting the macroeconomic stability and M&A outlook in core markets

INDEX

SPAIN – M&A Outlook – Private Equity – Capital Markets – Handling the Crisis

PORTUGAL – M&A Outlook – Private Equity – Capital Markets – Handling the Crisis

– Dealmaker Profiles

SPAIN

The Spanish economy will be among the most severely affected by the global crisis that upended life across the world in 2020. Despite a moderate rebound in 3Q20, Spain’s GDP was down 8.7% compared to the same nine-month period ending a year prior, according to the International Monetary Fund (IMF). IMF economists project a 12.8% slide by year-end as federal and regional governments impose new restrictions on movement and business activities.

Spanish companies have contracted government guaranteed debt amounting to 7% of GDP to shore-up their finances, but the country’s small and medium-size enterprises (SMEs), which account for 70% of overall economic activity, remain highly vulnerable and dependent on fiscal measures to remain solvent. About 37% of the debt contracted by Spanish companies is estimated to be at risk, according to the IMF, foreshadowing impending insolvencies for many in 2021.

“The wave of restructurings is coming,” said DLA Piper Spain Senior Partner Iñigo Gomez-Jordana. More troubling than the imminent onslaught of insolvencies, is the persistent lack of clarity where mitigation measures and their duration are concerned, however, Gomez-Jordana said.

New restrictions should be accompanied by guidance on how long they will last so that everybody can set their expectations, he said, noting there was a broad divergence among countries of the EU on approach, with poor coordination between them. “All this just serves to foment uncertainty,” he said.

“There’s a more pessimistic climate in Spain than in neighboring markets, which is affecting the macro situation,” said Norgestión Managing Partner Igor Gorostiaga. The lack of coordination was understandable in March, but the fact that this continues almost nine months later is confounding, Gorostiaga said.

Large companies and banks raised a lot of debt immediately after the lockdown to be solidly positioned in the face of uncertainty. The volume of senior and high yield issuances was very high, and there were plenty of investors ready to buy, Gomez-Jordana noted. Convertible debt issuances were down to a trickle, however, with few companies willing to risk equity at discounted rates amid the volatility, he said.

“I think there’s a general conviction that this situation is transitory,” said Gomez-Jordana. Of course, it’s important that the large companies that employ thousands don’t run into problems, and they need to maintain their cash reserves in an uncertain market, he added.

“Where the macro outlook is concerned, I tend to be an optimist,” said Portobello Capital Founding Partner Juan Luis Ramírez. “This crisis is better than the last, in that once it’s resolved, we’re going to return to normal more rapidly, as we have a healthy financial system,” he noted. Governments have injected historic sums into the economy, which should ultimately result in inflation to the benefit of debtors, he added.

Traditional retail, on the other hand, which was already suffering as e-commerce took at growing piece of the market, has been dealt a severe blow, Hernández noted. An acceleration of the migration online and away from brick and mortar among major retailers is a clear outcome of the current crisis, he said.

The Portuguese economy is projected to contract by 10% in 2020, according to the IMF, with unemployment pushing 14%. A moderate recovery with 5% GDP growth is projected in 2021, with a drop in unemployment to 8.7%. The Portuguese government’s stimulus measures aimed at supporting income, preserving employment and ensuring liquidity will amount to nearly 3% of GPD in 2020, according to Banco de Portugal’s October Bulletin, not enough to stave off its economic contraction, which outpaced most other markets of the Eurozone in 1H20.

“Currently the economic outlook is negative, but the full extent of the contraction will depend on the severity of the second wave and the measures that might be needed to control it,” said Deloitte Partner João Diogo Pinto. “If we don’t have full lockdown, we’ll be living under constrained economic conditions for the foreseeable future, and we may be heading for a third wave in 2021 as well,” Pinto said. The leisure, hospitality and retail industries have been decimated, he noted, with weak prospects for recovery in the near term.

Restaurants are open again, but new government measures in force since mid-October limit the number of people that can congregate to five, and with many working remotely or in rotation at the office, half the customers are completely missing, noted SRS Advogados Partner Paulo Bandeira. The Portuguese government’s 2021 budget being resolved in parliament has offered a value-added tax voucher, which will allow patrons to claim back a portion of what they spend in restaurants in 1Q21 the following quarter to encourage consumption and support the sector. Restaurants are happy with the measure, but the effective benefits will only accrue to consumers from April onwards, Bandeira noted. Meanwhile, the government upped its state of alarm and mandated mask wearing in public through the end of 2020 in a new law passed in late October.

Transactional Impact Monitor: Andean Region – Vol. 3

Posted on

Transactional Impact Monitor: Andean Region – Vol. 3

15 October 2020

TTR’s Transactional Impact Monitor (TIM) is a Special Report combining local knowledge and market visibility from top dealmakers developed to address extraordinary situations affecting the macroeconomic stability and M&A outlook in core markets

INDEX

CHILE – M&A Outlook – Handling the Crisis

COLOMBIA – M&A Outlook – Handling the Crisis

PERU – M&A Outlook – Handling the Crisis

– Dealmaker Profiles

CHILE

The mood among investors in Chile, and those looking on from abroad at what has long been considered the darling of Latin America for its political stability and liberal trade policies, is tenuous. The plebiscite on constitutional reform, originally scheduled for April, will be held on 25 October, a year after protesters filled the streets of Santiago following a public transit hike to voice their discontent on a range of matters. Among the grievances that led to widespread unrest were human rights abuses, the exclusion of a large swath of the population from the economic gains the country has enjoyed over the last three decades, and a generalized disenchantment with Chile’s form of pro-business, neoliberal democracy.

The economic crisis that gripped the world in 1Q20 caught Chile, and much of Latin America, mid-downward cycle, noted Banmerchant Deputy Manager of Corporate Finance Ignacio Rodríguez. Like other investment banks across the region, Banmerchant had several sale processes underway that were put on hold, Rodríguez said, noting that as the M&A work began to decline, restructuring became the firm’s core business.

“Many companies stopped generating revenues, but their liabilities still needed to be serviced,” he said. Chile’s banks stepped up to support the private sector, funneling low-interest loans with extended grace periods before borrowers had to begin repaying. In September, those grace periods began to expire, Rodríguez said, and if corporate revenues don’t normalize in October and November, a wave of insolvencies will hit Chilean shores.

The uncertainty surrounding the economic recovery is complicated by the October plebiscite, which has investors, and Chileans in general, anxious. “Everybody wants to restructure their liabilities long-term, but many won’t be able to,” Rodríguez said. “They will either go under or seek fresh capital. That’s where M&A will reactivate, representing an opportunity for foreign investors to enter Chile at very low valuations.”

Restrictions governing economic activity in Colombia are easing with all businesses except bars, nightclubs and gyms permitted to open daily as of 22 September, though opening hours continue to be limited for specific sectors. Business confidence has accordingly turned slightly positive for the first time since March, according to the local press.

“We can now turn the page,” said César Gutiérrez, Managing Director of boutique investment bank Bastion Capital Advisors. After six months of near paralysis, the private sector is ready to get back to business, he said. Many Colombian companies in certain industries are entering restructuring processes, refinancing their debt, looking for capital or exploring sale options after six months of little-to-no business activity, however, he noted.

Tourism and hospitality and related industries like aviation and catering, have been decimated, said Gutiérrez, and automotive sales are also down sharply. Bastion was recently approached by a company serving the aviation industry that could not continue to finance its overhead when revenue fell flat, Gutiérrez said. Though Colombia’s international airports reopened on 1 September, traffic remains lackluster as the fear of contracting COVID-19 while flying persists, and many corporate entities maintain work-from-home policies, limiting the company’s prospects for a rebound, he noted.

There is no way to maintain fixed costs for five or six months when revenue evaporates overnight, Gutiérrez said, especially for companies that have relied on debt financing. Colombia’s banks have classified virtually every business segment as high-risk, meanwhile, making it difficult for companies to access bridge financing, Gutiérrez said.

This looks to be the start of a wave of consolidation, where private equity funds with firepower can buy on the cheap, he noted, whether diversified domestic fund managers that have longstanding interests in Colombia, or those that have always had an interest in investing in the country. A long-awaited opportunity for private debt could finally find fertile ground in Colombia, Gutiérrez noted.

Despite the uncertainty about the timing and speed of the recovery, there will always be appetite for good assets, Gutiérrez said. “When some cry, others make handkerchiefs,” he noted, citing a popular saying. This is the moment for opportunistic investors, both strategic and financial, he added. “I’m very optimistic. This has been a moment to reflect, to analyze where industries are headed, and understand the new opportunities; companies need to get ready for what comes next.”

Following months of strict isolation, the Peruvian government announced it would permit air traffic between Peru and seven countries, namely Bolivia, Chile, Colombia, Ecuador, Panama, Paraguay and Uruguay, beginning the first week in October. The reopening of the country’s airspace comes despite an official death toll attributed to SARS-CoV-2 that puts Peru at the top of the list of nations globally by a significant margin, at over 1,000 per million inhabitants. Despite the health crisis, Peruvian companies are beginning to get back to business, and stalled transactions are getting back on track, according to Hernández & Cía. Abogados Partner Diego Carrión.

Peru was awash with M&A deals in 2015, when Carrión was appointed partner. That wave of transactions hit a bump when the “Lava Jato” scandal in Brazil spilled over into Peru, where Odebrecht and other large Brazilian and Spanish construction firms had large contracts underway in partnership with local entities, many of them, it turned out, won by corrupt means.

The construction sector was paralyzed as a result of this, with project finance transactions arrested midstream. This was followed by some opportunistic M&A when Odebrecht and other large international construction firms needed to exit some projects, Carrión recalled, while M&A activity in other sectors of the economy continued at a good pace.

Hernández & Cía. Abogados was never involved with Odebrecht, which gave it a great upside, as many clients began to search the firm out for its clean record, said Carrión. Among the important new clients garnered as a result was Graña y Montero, Carrión noted. In 2017, the firm was retained by the company’s new board to guide it through a reorganization, and it has continued to work hand-in-hand with the board and the new management ever since to overcome one of the most dire corporate crises in the country’s history. “They sought us out for the strength of our team, and because we had no conflict of interest,” Carrión said, noting Hernández was part of the “big change” in the company.

The firm’s deal flow isn’t dependent on the construction industry, however, and it has worked on a slew of M&A deals in other sectors in recent years, including several led by private equity investors. Real estate is one sector in which it has invested heavily of late to enhance its expertise. In the midst of the crisis in mid-2020, it poached an entire real estate practice from another law firm to bolster its capabilities in this growing field.

“This gives us an edge amid strong growth in what has become an increasingly sophisticated real estate market,” Carrión said. Real estate lawyers need to speak the language of the engineers and regulators, and Hernández was losing some business without a clear leader in the space, he said. The runway in the real estate market is tremendous, with construction projects that were shut down in 2Q20 now getting underway again and a pipeline of deals spanning the economy, from the development of agricultural lands to malls. “We now have the capacity to ride this wave,” Carrión said, noting the firm took advantage of its strong balance sheet and the lull in the market to make a strategic move that will position it with the right team.

While construction projects in the private sector are underway again, the large infrastructure projects tendered by the Peruvian government, including Line 2 of Lima’s metro and the expansion of Jorge Chávez Airport, are progressing at a snail’s pace, Carrión said, amid bureaucracy that’s worse than ever, inducing skepticism, fear and a lack of confidence among participants and onlookers alike.

Transactional Impact Monitor: Spain & Portugal – Vol. 4

Posted on

Transactional Impact Monitor: Spain & Portugal – Vol. 4

31 July 2020

TTR’s Transactional Impact Monitor (TIM) is a Special Report combining local knowledge and market visibility from top dealmakers developed to address extraordinary situations affecting the macroeconomic stability and M&A outlook in core markets

Sponsored by:

INDEX

SPAIN – M&A Outlook – Capital Markets – Private Equity – Handling the Crisis

PORTUGAL – M&A Outlook – Private Equity – Handling the Crisis

– Dealmaker Profiles

SPAIN

On the cusp of Spain’s summer holiday season, the country confronts the reality that its fight against SARS-CoV-19 may be far from over. The streets of Madrid are once again full of pedestrians, who are now required to wear masks in public, as reported cases surge to levels not seen since the beginning of May. New infections are being reported mainly among younger Spaniards, however, and haven’t resulted in the same level of hospitalizations, according to the local press.

The official death toll attributed to the novel corona virus stands just shy of 45,000, while in any given year, there are nearly 500,000 deaths overall in the country. Spain’s death rate has trended upwards over the past 10 years as the country’s population ages, with both cancer and circulatory system diseases each blamed for more than 100,000 deaths annually.

Nearly half of Spain’s autonomous communities are some semblance of normal, while the other half are considered high- or medium-risk by the authorities. Those who can work remotely, continue to do so across much of the country.

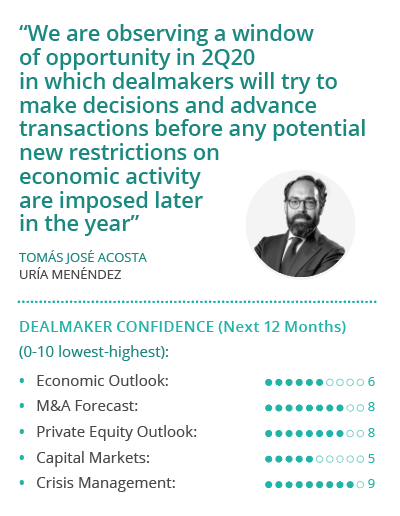

Dealmakers in the transactional market have remained incredibly busy, and the pipeline is looking robust for 2H20, sources told TTR. The workload for legal advisor Uría Menéndez has been surprisingly heavy, given the low expectations earlier in the year, despite the poor visibility about what will happen in the coming months, Partner Tomás Acosta told TTR.

Projections by the International Monetary Fund indicate a fall in global GDP of between 3% and 5%, while the Bank of Spain projects a 15% contraction in Spain, Acosta noted, but these figures too are in flux, making it difficult to predict what will happen by the close of the year.

“What I do see, and this will be key, is the need for government authorities to react decisively to avoid any major resurgence,” Acosta said, noting the new outbreaks seemed to be under control, even as reported cases escalate once again.

“We are observing a window of opportunity in 2H20 in which dealmakers will try to make decisions and advance transactions before any potential new restrictions on economic activity are imposed later in the year,” Acosta added.

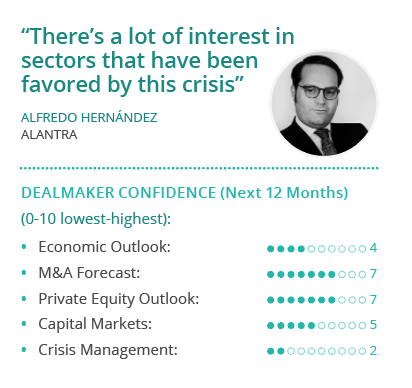

It won’t be until September or October that reality will set in, said Alantra Partner Alfredo Hernández, when companies will have three quarters of results to analyze. There will be a window between October and November to close deals, but the real boom will be in 1Q21, said Hernández. Alantra’s deal pipeline is stronger than it was at this point in 2019, Hernández said, but the type of deals has changed from overwhelmingly M&A-related to roughly half M&A and half financing transactions, he said.

When speaking with CEOs and CFOs, they are primarily concerned about their 2020 results, Hernández said. “The reality is that they still don’t know what the impact will be, though for those in the transportation and hospitality industries, the repercussions have been profound, and the impact is exceedingly clear,” he said.

There are already clear winners too, Hernández noted, citing the healthcare industry, certain consumer product segments and food production and distribution, which haven’t merely been resilient, they’ve growth by 20% to 30%. “All this has been made possible thanks to technology and communications, which have helped accelerate the existing trend of digitalization. “

Traditional retail, on the other hand, which was already suffering as e-commerce took at growing piece of the market, has been dealt a severe blow, Hernández noted. An acceleration of the migration online and away from brick and mortar among major retailers is a clear outcome of the current crisis, he said.

Portugal has registered a much lower toll from SARS-CoV-19 than its Iberian neighbor, with some 50,613 confirmed cases and 1,725 deaths attributed to the novel coronavirus. This hasn’t allowed the country to escape the devastating economic impacts associated with the pandemic threat, however, and the prospects for the economy are grim as the country enters peak summer holiday season, dealmakers told TTR.

“I am pessimistic about the economic outlook for Portugal,” said SLCM Managing Partner Luís Miguel Cortes Martins. “We are already seeing empty hotels; high-end restaurants also with very few clients. Many of them in fact reopened and then had to close again; that will generate a lot of unemployment and it will have a sharp impact on demand.”

The estimates for the Portuguese economy are not at all positive, Cortes Martins noted, and that will, in turn, drive away foreign investment. “I don’t see a V-shape recovery for the Portuguese economy,” he said.

“If Spain has a quick recovery, Portugal will be better off, since they are our main commercial partner,” he noted, and Portugal is also subject to the form the recovery will take across Europe, generally, especially in Germany. “Tourism is a main driver in our economy, and no one really knows when that will recover,” he said.

“I am somewhat pessimistic with regard to the economic outlook for 2021,” agreed EY Partner, Strategy and Transactions Miguel Farinha. “The pandemic’s economic impact will be greater than what most institutions, such as the IMF and the Bank of Portugal, are forecasting,” he cautioned. “Portugal will take a heavy blow, one which I think most people are not yet estimating correctly,” he said.

Portugal’s economy grew substantially in recent years, mostly thanks to its booming tourism sector, Farinha pointed out. Tourism typically represents about 15% of GDP in direct contributions and well over 20% including indirect contributions. The sudden flat line will bring severe economic hardship, he said.

Until a vaccine or some kind of treatment is made available, the downturn will persist, Farinha added. Notwithstanding his gloomy macroeconomic forecast, Farinha said the transactional market will be very strong, with a lot of very good acquisitions.