Queda de 23,9% nas operações de Fusões e Aquisições em fevereiro

- Mês fecha com 54 transações

- Fevereiro tem o pior resultado dos últimos dois anos

- Investimentos de Venture Capital em alta de 23% no ano

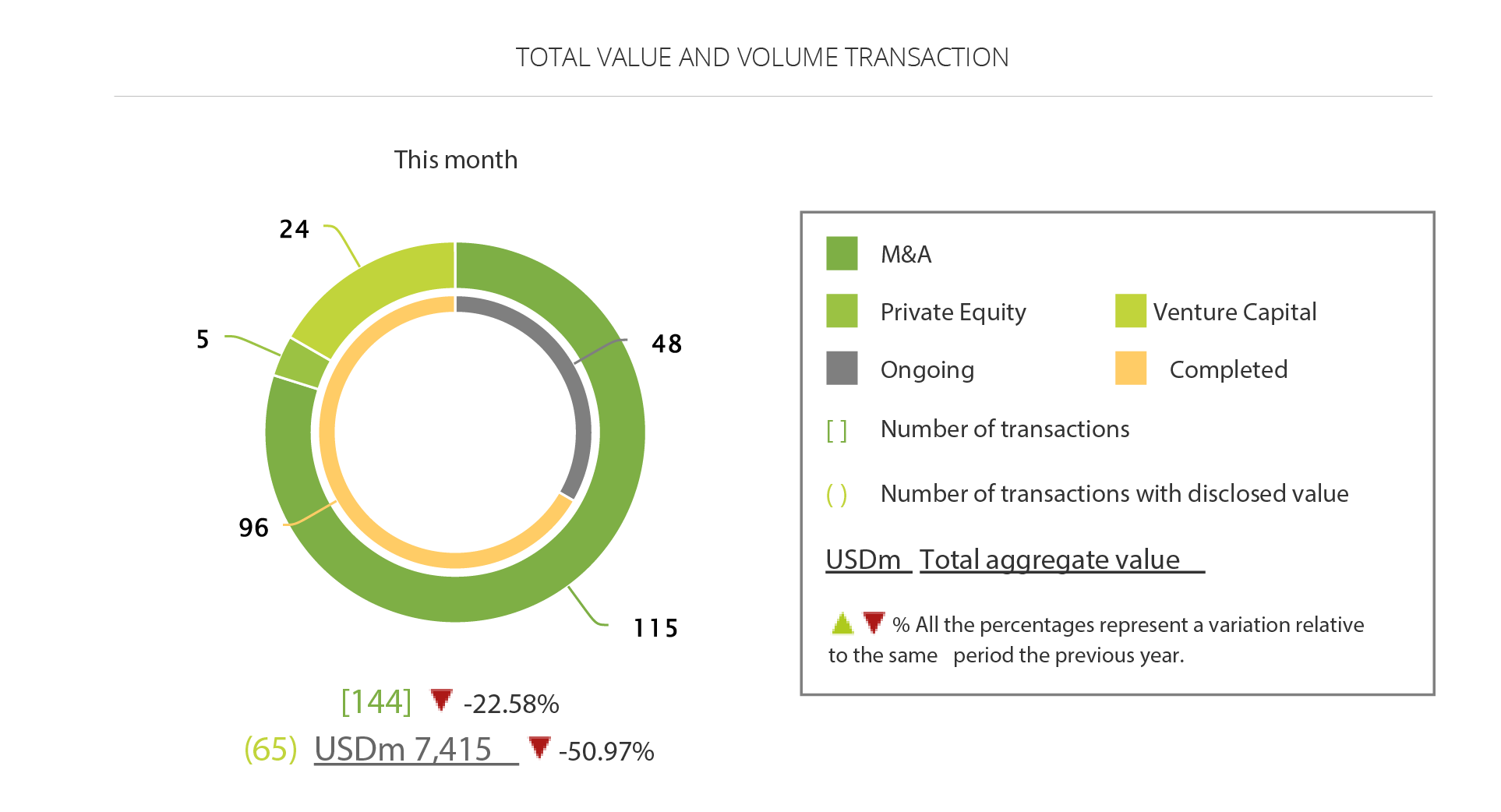

O mês de fevereiro registrou 54 transações de fusões e aquisições de empresas no mercado brasileiro, o que equivale a uma queda de 23,9% em relação ao mesmo mês no ano anterior, quando foram anunciadas 71 operações. De acordo com os dados publicados no Relatório Mensal da Transactional Track Record, em parceria com a LexisNexis e TozziniFreire Advogados, em volume financeiro, essas transações movimentaram, entre as 16 que tiveram seus valores revelados, R$ 4,6 bilhões, baixa de 75,9% em relação ao montante de R$ 19,1 milhões somados em fevereiro de 2016.

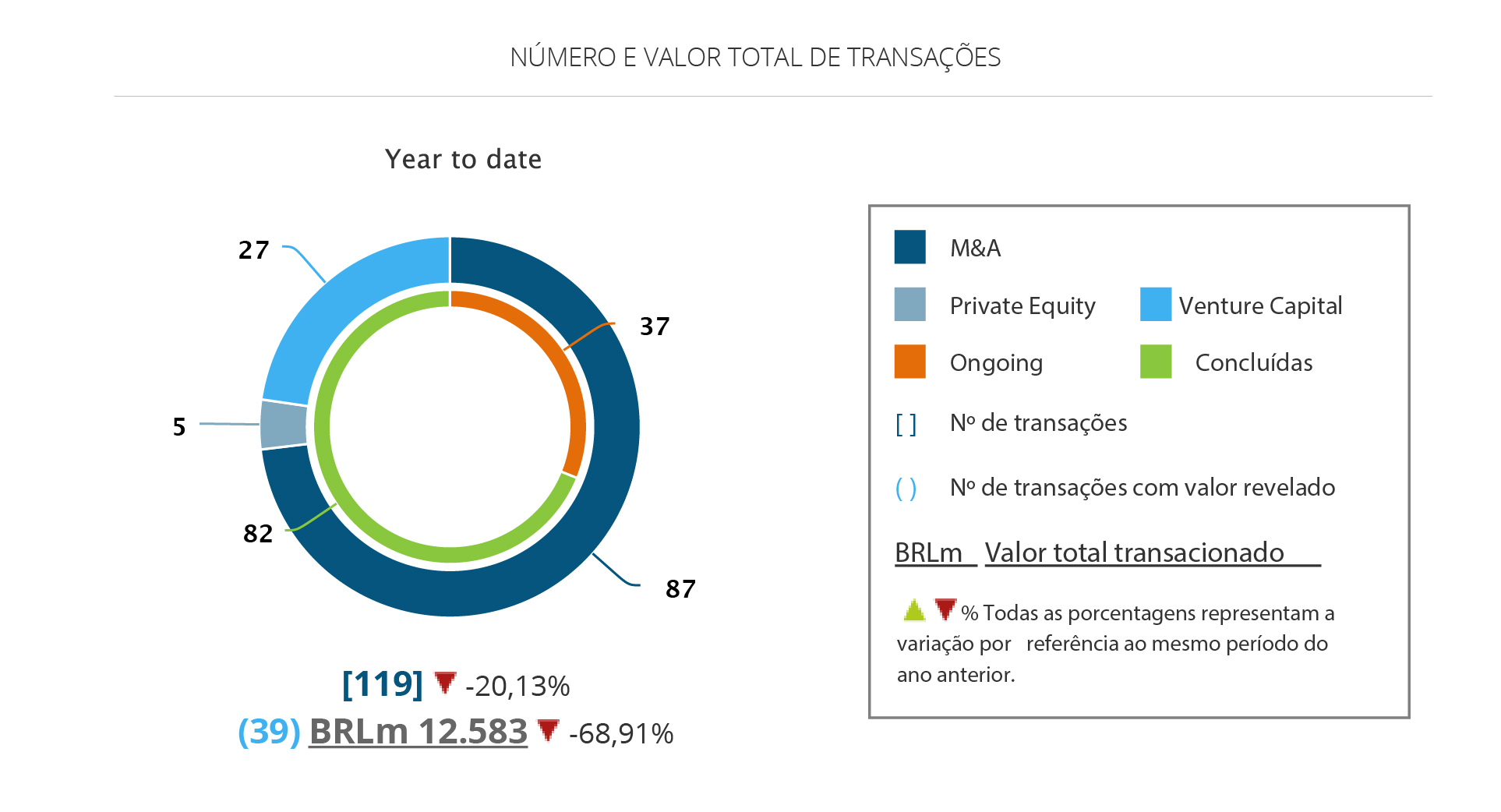

No primeiro bimestre do ano, foram realizados 119 anúncios de operações de compra e venda de participação envolvendo empresas brasileiras. Número inferior ao registrado em 2017 e 2016, 149 e 139, respectivamente. Das operações de 2018, 39 tiveram seus valores revelados, somando R$ 12,5 bilhões, total 38,9% inferior ao mesmo período do ano anterior.

O segmento Tecnologia foi o que mais atraiu investimentos no mês, foram 14 transações, repetindo resultado de janeiro. No bimestre, um salto de 56% nos movimentos em relação ao mesmo intervalo do ano anterior. O crescimento dos investimentos no setor acompanha a alta de 28,5% das aquisições estrangeiras nos segmentos de Tecnologia e Internet.

No apanhado do ano, Financeiro e Seguros aparece na segunda colocação, com 13 operações, declínio de 7%, seguido por Saúde, Higiene e Estética e Distribuição e Retail, 11 operações cada e queda de 45% e 48%, respectivamente.

Operações cross-border

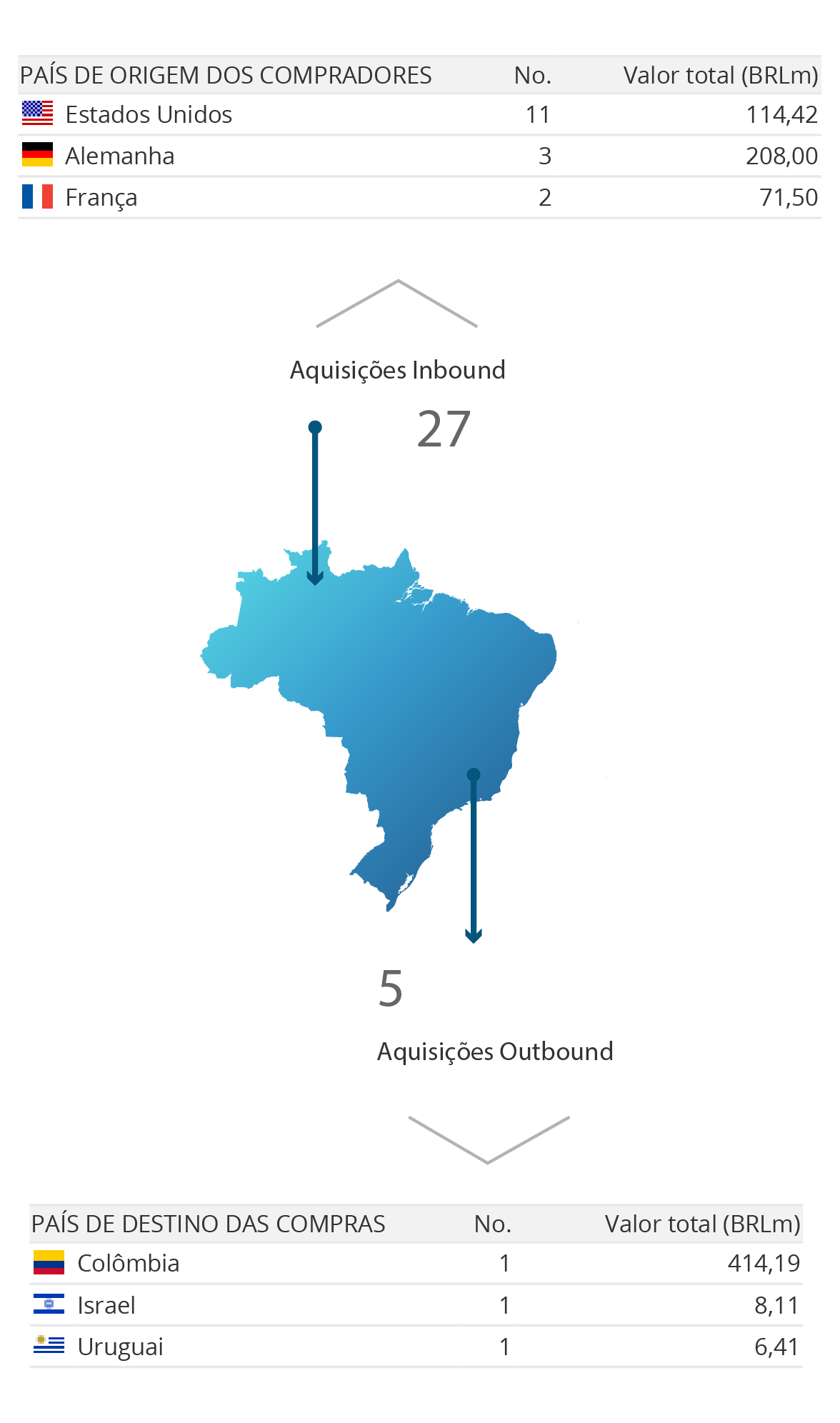

No âmbito inbound, foram contabilizadas 27 operações de compra de empresas brasileiras no bimestre. Apesar de seguir como o país com o maior número de aquisições no mercado brasileiro, as 11 operações dos Estados Unidos, que juntas somam R$ 114 milhões no ano, não foram suficientes para ultrapassar os valores investidos por empresas chinesas e alemãs. O único investimento chinês registrado no ano, 99 taxis pela chinesa Didi Chuxing, chegou a aproximadamente R$ 1,9 bilhões, enquanto as três operações envolvendo investimentos de empresas de origem alemã totalizaram R$ 208 milhões.

No âmbito inbound, foram contabilizadas 27 operações de compra de empresas brasileiras no bimestre. Apesar de seguir como o país com o maior número de aquisições no mercado brasileiro, as 11 operações dos Estados Unidos, que juntas somam R$ 114 milhões no ano, não foram suficientes para ultrapassar os valores investidos por empresas chinesas e alemãs. O único investimento chinês registrado no ano, 99 taxis pela chinesa Didi Chuxing, chegou a aproximadamente R$ 1,9 bilhões, enquanto as três operações envolvendo investimentos de empresas de origem alemã totalizaram R$ 208 milhões.

O setor de Internet foi aquele que mais recebeu aporte de empresas estrangeiras em 2018. Destaque também para os setores de Transportes, Aviação e Logística, Tecnologia e Financeiro e Seguros.

As compras brasileiras no exterior tiveram como alvo prioritário no ano a América Latina, com aquisições realizadas na Colômbia, no Uruguai, e, em fevereiro, no Paraguai, compra do controle da Estrella Del Paraguay pela fabricante de brinquedos Estrela, e no Chile, na aquisição da rede O2 Fit pela brasileira Smart Fit. O investimento de U$ 2,5 milhões da Klabin na start-up israelense Melodea Bio Base Solutions foi o primeiro de uma empresa brasileira fora da América Latina no ano.

Private Equity e Venture Capital

Nos cenários de private equity e venture capital, o mercado continua com um panorama positivo, reflexo também da retomada dos investimentos dos fundos estrangeiros em empresas brasileiras, com alta de 66,67% nos aportes.

Entretanto, fevereiro não trouxe resultados favoráveis no segmento de private equity. O volume financeiro das operações da modalidade sofreu queda de 40% no número de deals – apenas três registrados. Porém, em volume financeiro, o ano já registrou alta de 83% no total aportado em comparação a 2017, alcançando R$ 2,2 bilhões em investimentos.

Nos investimentos de venture capital, o panorama é outro. Das 27 transações assinaladas no TTR desde o inicio do ano, 23% acima do que foi anunciado no mesmo período do ano anterior, 13 revelaram valores que somam R$ 576,31 milhões, alta de 18% em comparação ao período homólogo de 2017. Porém, em fevereiro, 13 operações movimentaram R$ 96,5 milhões, 20% de retração. O setor de maior crescimento no acumulado dos dois primeiros meses do ano foi Tecnologia – 22% – e também o que apresentou mais transações, 11.

Transação TTR do Mês

A conclusão da aquisição de 90% da TCP, empresa que opera o Terminal de Contêineres de Paranaguá, no Paraná, pelo grupo chinês China Merchants Port, por meio da sua subsidiária Kong Rise Development, por R$ 2,9 bilhões.

A conclusão da aquisição de 90% da TCP, empresa que opera o Terminal de Contêineres de Paranaguá, no Paraná, pelo grupo chinês China Merchants Port, por meio da sua subsidiária Kong Rise Development, por R$ 2,9 bilhões.

O terminal tem capacidade de movimentação anual para 1,5 milhão de TEUs, com previsão de aumento para quase 2,5 milhões de Teus até 2019. O CADE já aprovou a transação.

O TCP foi assessorado na transação pelo Banco BTG Pactual e pelo Mattos Filho, Veiga Filho, Marrey Jr e Quiroga Advogados, que também prestou assessoria para uma das partes vendedoras, a Advent International. A APM Terminals, que também vendeu sua participação, recebeu assessoria jurídica do escritório Lobo de Rizzo Advogados.

Por sua vez, a Kong Rise Development teve como assessores o Pinheiro Neto Advogados, e os escritórios chinês e norte-americano da Linklaters.

Leia mais sobre a Transação do Mês

Rankings Financeiros e Jurídicos

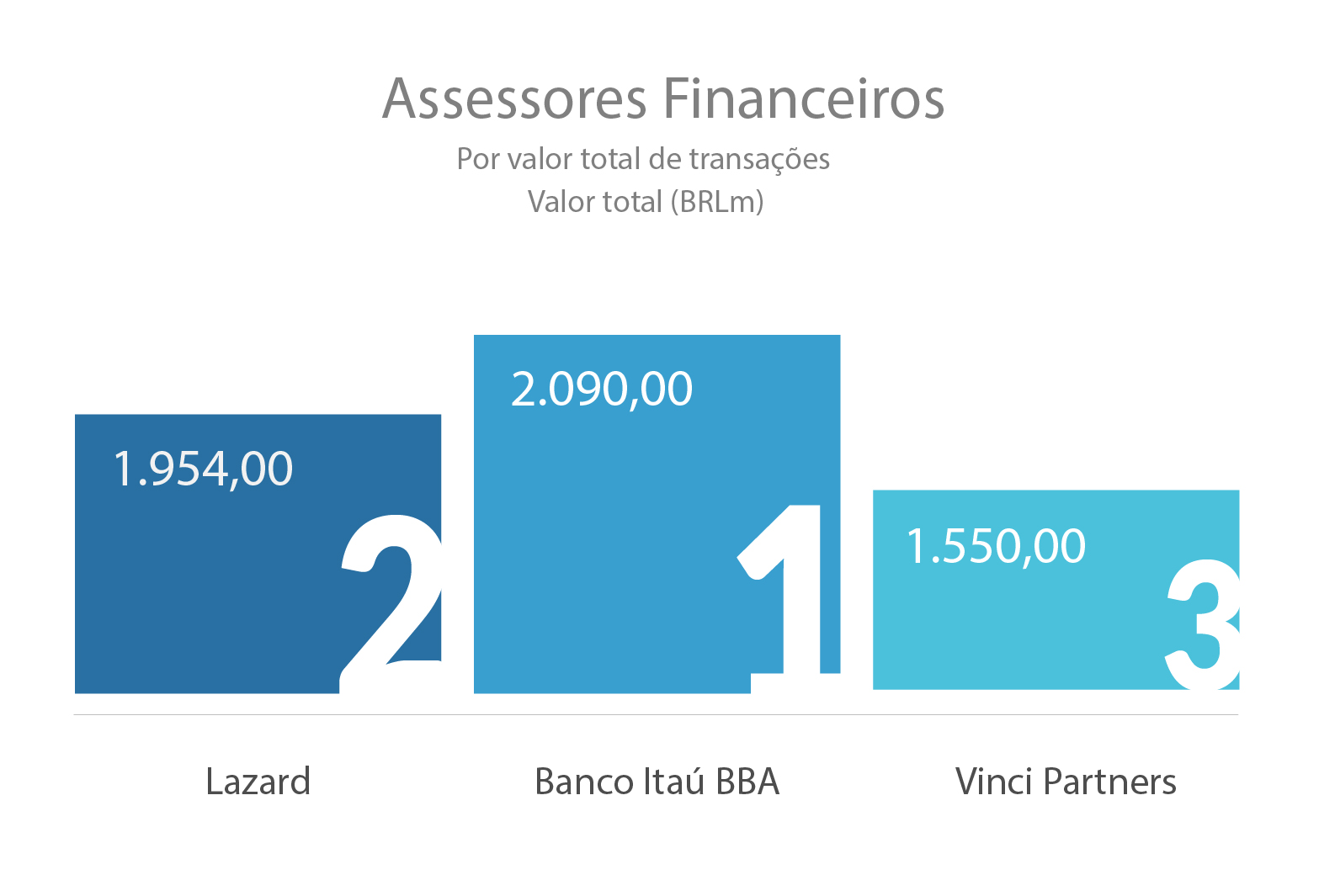

O pódio do ranking TTR de assessores financeiros por valores das transações e número de transações é liderado em fevereiro pelo Banco Itaú BBA, com acumulado de R$ 2 bilhões nos primeiros dois meses do ano. Seguido por Lazard, com R$ 1,9 bilhão, e Vinci Partners, com R$ 1,5 bilhão.

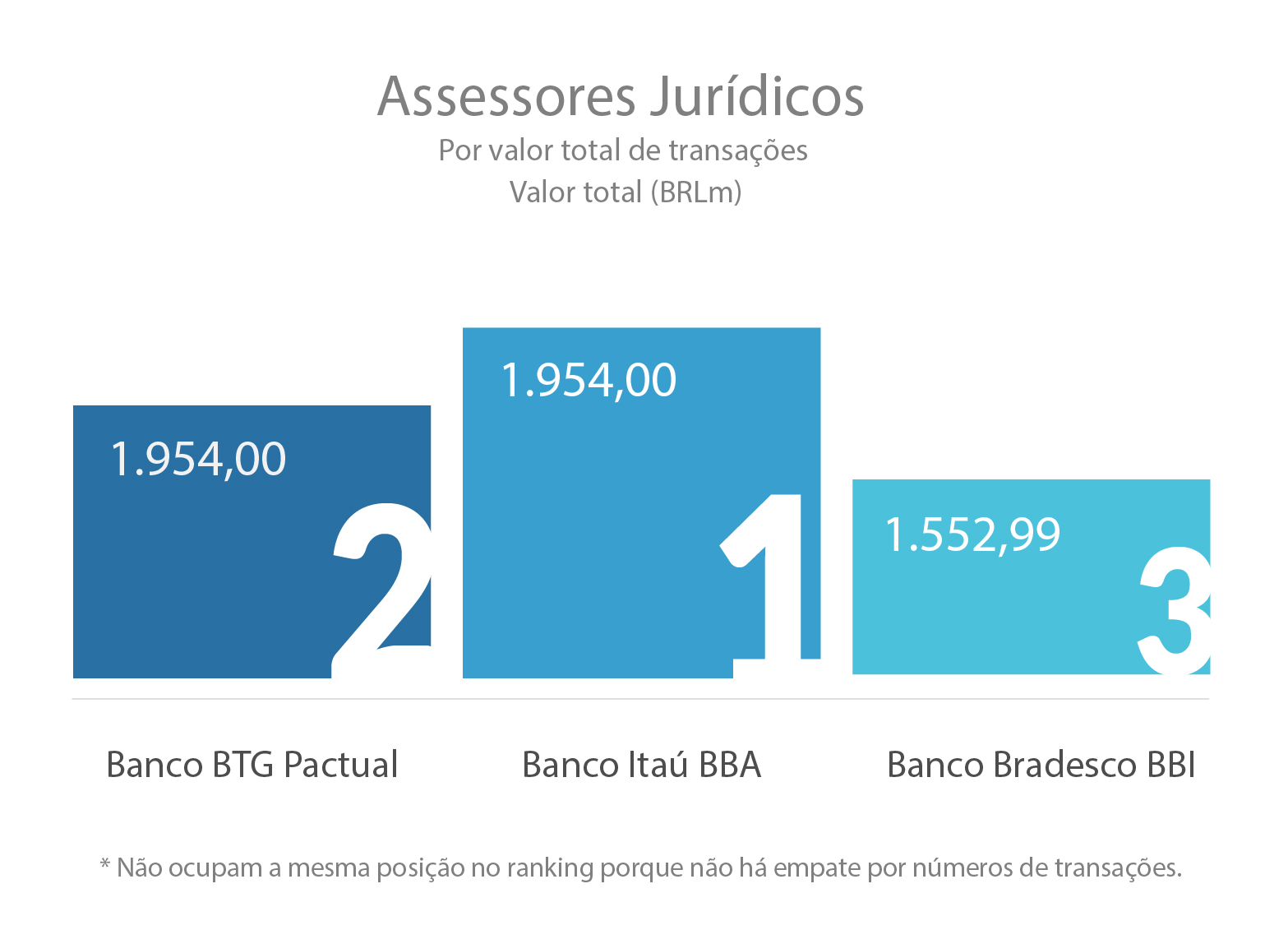

O ranking de assessores jurídicos por valor é liderado por e Barbosa, Müssnich, Aragão, com R$ 1,9 bilhão, seguido por Ulhôa Canto, Rezende e Guerra – Advogados, que alcançou o mesmo valor, mas perde no número de operações. TozziniFreire Advogados, R$ 1,5 bilhão, fica com a terceira posição. Por número de transações o ranking é liderado por Mattos Filho, Veiga Filho, Marrey Jr. e Quiroga Advogados (5), com Demarest Advogados na segunda colocação, e Felsberg Advogados na sequência.

Para o ranking completo, clique aqui.