Iñigo Erlaiz Cotelo is Partner of Goméz-Acebo & Pombo Spain, Head of Corporate and M&A from February 2016 – specializes in corporate, commercial and M&A transactions, notably involving private equity and restructuring and insolvency-led transactions. He is a member of the Board of Directors of the firm. As to industry sectors he specializes in food, retail, and manufacturing.

TTR: How would you describe the M&A market in Spain year-to-date in 2019?

We are seeing a high amount of

activity. While it’s true that the rate has not been steady, slowing down to a

certain point prior to the election and/or caused by news that has generated

uncertain macro conditions, in general, we are seeing a lot of transactional

activity. This activity has ramped up over H1, driven by abundant liquidity and

low rates that favour access to financing. As this should continue, we expect

H2 to have a similar level of activity.

TTR: As an expert in Retail, Insurance and Pension Funds, how do you expect these sectors to perform? What is your growth forecast for these sectors in Spain in the medium-to-long term?

These are sectors that are going through a

transformation process. In the retail sector, we are seeing movements arising

from the search for new models and the departure of existing models (investment

in companies with a technological base and restructuring of traditional

business). In the insurance sector, there has been a lot of activity stemming

from the reorganisation of bancassurance agreements. Also, there are

cooperation agreements and investments that allow for progress in the

digitalisation of the sector. It is still a fragmented sector, where a

concentration process is pending, which will arrive sooner or later (I think

via an initial concentration phase of mutual insurance companies, by searching

for efficiency and robustness of the balance facing a regulatory environment

that is increasingly demanding with solvency levels).

TTR: How do you see the Spanish private equity market developing?

It is also very dynamic. Funds

have been raised recently which have been larger. Therefore investment has also

grown. There is a lot of competition in the middle of the market (where a large

number of operators compete)and at the high end, but with more limited

investment opportunities. All this, along with a return to lending with

financing structures in which debt-based funds are entering, means a more

favourable context for the seller. I think that the trend will continue for the

rest of the year.

TTR:One of the attractive sectors in Spain for private equity firms is the food industry, in which you also have considerable experience. Why is this sector so attractive for private equity investors in the current economic climate?

It is one of the sectors that has

invested most in technology and process modernisation. There are very

competitive companies, international leaders in their market niches who are

exporters by vocation. At the same time, there is a reconfiguration process in

relationships between suppliers and distributors in which some operators are

looking for access to new markets and clients while others are looking for more

efficiency though vertical integration. Private equity funds can be immensely

useful to support these processes. I think there is a clear flit and that it is

a sector that offers many opportunities to this type of investor profile.

TTR: You also specialize in bankruptcy and restructuring processes. What is the most viable solution for the companies undergoing such processes currently: to access funds from financial institutions or to raise capital through the sale of equity to external investors? What are the advantages of each option?

Traditional financial

institutions avoid these situations. There are special situations funds that

can inject debt in a pre-bankruptcy situation but must be a loan-to-value and a

clear exit scenario. Often, greater legal certainty is offered by structuring

the takeover and restructuring transaction within the bankruptcy, be it with a

proposal of early agreement or via purchasing a production unit. These are

complex transactions, reserved for specialised funds that require a significant

amount of prior risk analysis but whose returns may be substantial in return.

TTR:Cómo describiría la actividad del mercado de M&A español en lo que va de 2019?

Estamos

viendo gran actividad. Es cierto que el ritmo ha sido inconstante, con cierta

ralentización previa al proceso electoral y/o motivada por noticias que han

generado momentos de incertidumbre macro pero, en general, sigue habiendo mucho

movimiento transaccional. Esta actividad se ha acelerado en el final del primer

semestre, impulsada por la abundancia de liquidez y un entorno de tipos bajo

que favorece el acceso a la financiación. Como ese contexto se mantendrá

prevemos una segunda parte del año con un ritmo de actividad similar.

TTR: Más específicamente, como experto en los sectores Retail y Seguros y Fondos de Pensiones, ¿qué balance haría de su actividad transaccional? ¿Qué comportamiento espera en estos sectores en el medio/largo plazo en España?

Son sectores que están viviendo tiempos de transformación y cambio. En el sector retail vemos movimientos provocados por la búsqueda de nuevos modelos y el agotamiento de los existentes (inversiones en compañías con base tecnológica y restructuración de negocios tradicionales). En sector de seguros ha habido mucha actividad derivada de la reorganización de los acuerdos de bancaseguros. También hay inversión y acuerdos de colaboración que permitan avanzar en el proceso de digitalización del sector. Sigue siendo un sector atomizado, donde está pendiente un proceso de concentración que, tarde o temprano, acabará por llegar, yo creo que de la mano de una primera fase de concentración de las mutuas, buscando eficiencia y robustez del balance ante un entorno regulatorio cada vez más exigente con los niveles de solvencia.

TTR: ¿Qué expectativas tiene con el mercado de private equity español?

Está

también muy dinámico. Se han levantado fondos recientemente y, además, de mayor

tamaño, por lo que el ticket de las operaciones ha aumentado también. Hay mucha

competencia en el segmento medio de mercado (donde compite un número elevado de

operadores) y en el alto, con oportunidades de inversión más limitadas.

Todo ello, junto con una vuelta del crédito y con estructuras de financiación

en las que también están entrando los fondos de deuda, se ha traducido en un

contexto más favorable al lado vendedor. Creo que durante el resto del año se

mantendrá la tendencia.

TTR: Uno de los sectores más atractivos para private equity en España es el sector alimentario, en el que también tiene usted experiencia contrastada. ¿Qué ofrece este sector en la actualidad a firmas de private equity?

Es uno

de los sectores que más ha invertido en tecnología y modernización de procesos.

Encontramos compañías muy competitivas, líderes internacionales en sus nichos

de mercado y con vocación exportadora. Al mismo tiempo hay un proceso de

reconfiguración de las relaciones entre proveedores y distribuidores, en el que

algunos operadores buscan acceso a nuevos mercados y clientes y otros más

eficiencia a través de integraciones verticales. Los fondos de private equity

pueden ser de gran utilidad para apoyar estos procesos. Creo que hay un

encaje claro y que es un sector que ofrece grandes oportunidades a este perfil

de inversor.

TTR: Por último, se especializa usted también en insolvencias y restructuraciones. En este tipo de situaciones, ¿es más viable hoy día acudir a financiación de entidades financieras o a inversores que entren en el accionariado de las empresas concursadas? ¿Qué ventajas tiene cada opción?

Las entidades financieras tradicionales evitan

estas situaciones. Hay fondos de situaciones especiales que pueden inyectar

deuda en una situación pre-concursal, pero tiene que haber un loan to value y

un escenario de salida claros. A menudo ofrece mayor seguridad jurídica

instrumentar la operación de toma de control y restructuración dentro del

concurso, ya sea con una propuesta anticipada de convenio o la compra de una

unidad productiva. Son operaciones complejas, reservadas a fondos

especializados, que requieren de mucho análisis previo “a riesgo”, pero que, a

cambio, pueden aportar grandes rentabilidades.

DEALMAKER INSIGHTS

Posted on

Rules and Advantages of using Insurance for

M&A Transactions

Transactions involving purchase and

sale, incorporations and mergers, generically denominated as mergers and

acquisitions transactions (“M&A”),

encompass a variety of different structures that, as a rule, involve the

transfer of a set of rights and obligations between buyers and sellers, where

the risks – despite the sincere efforts of the due diligence teams involved –

are not entirely known by the buyers when the transaction contracts (“Contracts”) are executed.

In fact, given the uncertain nature

of the business activities, it is possible that even the sellers are not aware

of all the factors and events, past and present, which can materially impact

the futures of their companies.

Therefore, in order to become

predictable, these Contracts use representations and warranties (“R&W”) clauses. A useful mechanism

for the sharing of risks inherent to M&A deals, the R&W allocate such

risks to those best prepared to support them. In effect, more than in other

sections of the Contracts, it is in the R&W that value in M&A

transactions can be created or destroyed.

In practice, these kinds of clauses

are structured in the form of statements about the company being acquired (the

“Target”) which are made by seller

and that work as a set of assumptions about the transaction’s economic

conditions. In case of any incorrectness or inaccuracy of such clauses, buyer

will be allowed to seek for the pre-established contractual remedies.

In this stage, the possible

measures/remedies vary as wildly as M&A structures themselves, although the

following are almost always included in the Contracts: (i) indemnity assurances

through which the seller is obligated to reimburse the buyer for damages resulting

from the violation of the R&W in question; and (ii) the contracting of

escrow account administration services, through which part of the funds

necessary for the completion of the transaction are unavailable to the parties

and under the management of an independent banking institution that will either

return them to the buyer – to the extent

the R&W are not complied with – or, if they are fully observed, deliver

them to the seller at the end of the term agreed to in the relevant Contract.

Representations and Warranties Insurance

The main purpose of the Representations

and Warranties insurance (“R&W

Insurance”) – the object of this text – is to ensure compliance with the R&W.

Such policies can be taken out by either the buyer or the seller side. As an

alternative to the remedies above, R&W Insurance presents a series of

advantages, namely:

during

pre-closing, it reduces the distress between buyers and sellers regarding the representations

and warranties to the extent the burdens resulting from their violation are

supported by the insurer, an independent third party;

during

post-closing, if the buyer and seller remain in contact, whether because it was

not a full sale, or because the seller continues to participate in the Target’s

management, distress is avoided as any R&W violations will be dealt with

through the insurer and not between the parties;

speeds

up indemnity payments, mainly because these payments made through insurance are

typically less susceptible to litigation than if they were made directly

between the parties;

buyers

are able to access better financing conditions to the extent that the Target’s

activity is subjected to less unexpected events;

ensures

that R&W violations are indemnified regardless of the seller’s financial

condition;

allows

buyers and sellers to cut ties faster – whether through indemnity agreements or

the establishment of escrow accounts, after closing the seller is typically

prohibited from freely accessing the funds resulting from the transaction; this

situation can be especially inconvenient for investment funds with defined duration

term or to any party wishing to use such funds for other purposes; and

with

the trend of decrease of the interest rates, depending on the seller’s capital

cost, taking on a R&W Insurance policy can be more financially advantageous

(with the resulting improvement of the RoR of other investments) compared to

keeping large sums deposited in an escrow account.

Created in 1997 in the US, R&W

Insurance took a while to gain market, but it has grown significantly in recent

years. In 2017, for example, 34% of the M&A transactions with values

between US$ 25 million and US$ 1 billion counted with R&W Insurance, while

the corresponding figure for 2016 was 20%.

Still in 2017, R&W Insurance policies were taken out in 75% of M&A transactions where private equity funds figured as buyers [1].

In addition to the larger market

penetration, over time, R&W Insurance products have become more flexible.

In principle, insurers offering these products were quite reticent when the

policy holder did not maintain part of the risk, in such a manner that R&W Insurance

would cover only the excess of the

limits of the indemnity agreements executed by seller. However, in the US it is

currently possible to find policies without such limitations, although the

premiums for these products are, of course, higher.

In the US, R&W Insurance premiums vary, on average, between 3% to 8% of the insured capital (which is proportional to the value of the transaction), which can make it less attractive for smaller transactions due to the high subscription costs, especially related to qualitative analyses carried out by insurers on the due diligence processes carried out by buyers [2].

In Brazil

The products available in Brazil normally cover: (i) the

amounts payable to buyers as penalties or indemnities under the terms

of the Contracts entered into with the sellers due to violation of the R&W;

and (ii) the defense costs relating to suits filed by third parties as a result

of R&W violations.

The following are exclusions and events of loss of

rights typical of these kinds of insurance products:

R&W explicitly

identified by the insurer as not being covered or only partially covered (in

the extension of such non-cover);

all R&W violations, or

facts that could reasonably result in R&W violations, over which the buyer

either had knowledge of or should have had knowledge of, when signing or

closing the transaction, as the case may be, and that were not disclosed to the

insurer before such dates;

fines and penalties of a

criminal nature;

non-compliance by the

insured (buyer) of its obligations, as established in the Contract; and

negligence by the insured (buyer)

in immediately communicating to the insurer any R&W violation or fact that

could reasonably result in a R&W violation or any aggravation in the risk

of a R&W violation.

The first product of this kind was only marketed in Brazil in the 2014 year by AIG Seguros Brasil S.A. With a product solely available for the buyer side and with a capped cover of US$ 25 million (per transaction) [3], it is clear that the R&W Insurance market in this country still lacks the diversity and flexibility of the North American market. Even so, according to Marsh Corretora de Seguros Ltda., R&W Insurance demand in Brazil over the first half of the 2018 year grew by 35%, compared to the same period in 2017 [4].

Conclusion

Beyond the long term trends (Brazil has been seeing a

significant increase in the volume of M&A over the past two decades[5]),

the imminent approval of an agenda of legislative reform and the start of a new

cycle of prosperity in the country are setting the expectation for a rapid

increase in the volume of M&A transactions and, consequently, of contracting

of R&W Insurance.

Bearing in mind that the national market for this kind

of insurance remains unexploited, this favorable economic scenario represents a

unique growth opportunity for insurers. Meanwhile, for those involved in

M&A deals (especially lawyers), the handling of this product will represent

an important competitive edge, to the extent it will undoubtedly add

significant value to the transactions they deal with, as already happens in

more mature markets.

As

operações de compra e venda, incorporação, fusão de empresas, dentre outras,

genericamente denominadas fusões e aquisições (mergers and acquisitions – “M&A”),

abrangem uma variedade de estruturas diferentes que, em regra, importam na

transferência de um complexo de direitos e obrigações entre alienantes e

adquirentes, cujos riscos – apesar dos esforços sinceros das equipes de due diligence – não são inteiramente

conhecidos pelos adquirentes no momento da assinatura dos contratosda operação (“Contratos”).

Em

verdade, dada a natureza incerta das atividades empresariais, é possível que

nem mesmo o vendedor tenha ciência dos fatores e eventos, presentes ou

pretéritos, passíveis de impactar materialmente seu negócio no futuro.

Assim,

a fim de se tornarem mais previsíveis, os Contratos se valem das cláusulas de

declarações e garantias (representantions

and warranties – “R&W”).

Mecanismo hábil à repartição dos riscos inerentes às operações de M&A, por

meio das R&W é possível aloca-los àqueles melhor equipados para suportá-los.

Com efeito, mais do que em outras seções dos Contratos, em meio às R&Ws

pode-se criar ou destruir valor nas operações de M&A.

Na

prática, as cláusulas desse tipo são estruturadas na forma de assertivas sobre

a empresa a ser adquirira (“Target”)

feitas pelo vendedor e funcionam como um conjunto de premissas das condições

econômicas da transação, cuja eventual falsidade franqueia ao comprador acionar

os remédios contratuais preestabelecidos.

Nesse

passo, as medidas/remédios possíveis são tão variados quanto as estruturas de

M&A, dentre as quais, no entanto, destacam-se pela quase onipresença: (i) os

acordos de indenidade firmados nos Contratos, por meio dos quais o vendedor se

obriga a ressarcir o comprador dos prejuízos decorrentes da violação de

determinada R&W; e (ii) a contratação de serviços de administração de conta

vinculada (escrow account), por meio

dos quais parte dos recursos necessários à concretização da operação ficam

indisponíveis às partes e sob a gestão de instituição bancária independente, que

os devolverá ao comprador na medida em que as R&W venham a ser descumpridas,

ou os entregará ao vendedor após o decurso de prazo contratualmente determinado

dede que não haja violação das mesmas.

Seguro de Representantions and Warranties

O

seguro de declarações e garantias (“Seguro

de R&W”) – objeto deste texto – tem por finalidade principal garantir o

cumprimento das R&W, podendo ser contratado tanto pelo comprador (buyer side), quanto pelo vendedor (seller side). Como alternativa aos

remédios acima, o Seguro de R&W apresenta uma série de vantagens:

no pré-closing, reduz o desgaste negocial entre

comprador e vendedor acerca das declarações e garantias, na medida em que os

ônus decorrentes de sua violação serão arcados por seguradora, terceira à

relação;

no pós-closing,

caso o vendedor e o comprador mantenham relações, seja porque a venda não foi

integral, seja porque o vendedor compõe a administração da Target, evita o

desgaste, na medida em que quaisquer violações às R&W serão tratadas com a

seguradora, e não entre as partes;

agiliza o pagamento das indenizações, em grande

medida porque o pagamento das indenizações por meio de seguro tem menor

litigiosidade do que por meio de cobrança direta entre as partes;

viabiliza melhores condições de financiamento

pelo comprador, na medida em que a atividade da Target fica sujeita a menos imprevistos;

assegura que eventuais violações das R&W

sejam indenizadas a despeito da situação financeira do vendedor;

permite que comprador e vendedor se desvinculem

mais rapidamente: seja por meio de acordos de indenidade, ou do estabelecimento

de contas vinculadas, a vendedora, após o closing,

não pode/deve livremente dispor dos recursos decorrentes da venda, o que pode

ser especialmente inconveniente para fundos de investimento com prazo

determinado de duração ou qualquer um que deseje destinar os recursos para

outra finalidade; e

com a tendência de queda dos juros (taxa

básica), a depender do custo de capital do vendedor, a contratação de Seguro de

R&W pode vir a ser financeiramente mais vantajosa (com a consequente

melhora na taxa interna de retorno do investimento) do que a manutenção de

vultuosas quantias em conta vinculada.

Criado

em 1997 nos Estados Unidos, o Seguro de R&W demorou a se difundir, mas, nos

últimos anos, tem se expandido rapidamente. Vinte anos depois, em 2017, dentre

as operações de M&A ocorridas nos Estados Unidos com valor compreendido

entre US$ 25 milhões e US$ 1bilhão, 34% contaram com a contratação de Seguro de

R&W, contra somente 20% em 2016.

Ainda

em 2017, houve contratação de Seguro de R&W em 75% dos M&A’s nos quais

fundos de private equity atuaram como

compradores[1].

Além

da maior penetração no mercado, com o passar do tempo os produtos de Seguros de

R&W têm se tornado mais flexíveis. Em princípio, as seguradoras que

operavam esse tipo de produto eram muito reticentes em segurar as R&W em

operações nas quais o segurado não retivesse parte do risco; as coberturas de

R&W eram feitas somente em excesso aos limites dos compromissos de

indenidade assumidos pelo vendedor. Hoje, nos Estados Unidos, entretanto, já é

possível contratar coberturas desse tipo mediante proporcional majoração no

valor do prêmio a ser pago, é claro.

No mercado

norte-americano, os prêmios dos Seguros de R&W variam, em média, entre 3% a

8% do capital segurado (que é proporcional ao valor da operação), o que pode

torná-lo pouco vantajoso para operações menores devido aos elevados custos de

subscrição, mormente relacionados às analises qualitativas conduzidas pelas

seguradoras com relação aos processos de due

diligence realizados pelos compradores[2].

No Brasil

Os produtos

disponíveis no mercado brasileiro, normalmente, cobrem: (i) os valores a que os

compradores façam jus a título de multa ou indenização, nos termos dos Contratos

firmados com o vendedor, em virtude da violação às R&W; e (ii) os custos de

defesa relacionados a ações ajuizadas por terceiros em decorrência da violação

das R&W.

Em tempo, são

exclusões e hipóteses de perda de direito típicas de produtos de seguro desse

tipo:

as R&W expressamente identificadas pela seguradora

como não cobertas ou como parcialmente cobertas (na extensão de sua não

cobertura);

todas as violações de R&W, ou fatos que possam

razoavelmente resultar em violações de R&W, sobre as quais o comprador

tinha conhecimento ou deveria ter conhecimento no momento do signing ou closing, conforme o caso, e que não tenham sido informadas à

seguradora antes dessas datas;

multas e penalidades de natureza criminal;

descumprimento pelo segurado (comprador) de suas

obrigações, conforme estabelecidas nos Contratos; e

desídia pelo segurado (comprador) em comunicar à

seguradora imediatamente acerca de qualquer violação das R&W ou fato que

razoavelmente possa acarretar uma violação das R&W ou agravamento desse

risco.

O primeiro

produto do tipo somente veio a ser lançado no país em 2014 pela AIG Seguros

Brasil S.A. Sendo comercializado somente na modalidade buyer side e com valor máximo de coberturas de 25 milhões de

dólares (por operação)[3],

o mercado brasileiro de Seguro de R&W ainda não possui a diversidade e

flexibilidade do norte-americano. Apesar disso, segundo a Marsh Corretora de

Seguros Ltda., entre os meses de janeiro a junho de 2018, a demanda pelo Seguro

de R&W no Brasil cresceu 35%, em comparação com o mesmo período de 2017[4].

Conclusão

Para além das

tendências de longo prazo (o Brasil vem experimentando um aumento significativo

no volume de M&As nas últimas duas décadas[5]),

na iminência da aprovação de uma agenda legislativa reformista e do início de

um novo ciclo de prosperidade no país, a expectativa é que haja um rápido

aumento no volume de operações de M&A e, consequentemente, de contratações

de Seguro de R&W.

Em vista do quão

inexplorado é o mercado nacional de seguros desse tipo, essa conjuntura

econômica favorável representa uma oportunidade única de expansão das carteiras

das seguradoras. Já para os operadores de M&A (especialmente os advogados),

o manuseio desse produto representará relevante diferencial competitivo, na

medida em que certamente agregará imenso valor às operações por eles

conduzidas, tal como já ocorre em mercados mais maduros.

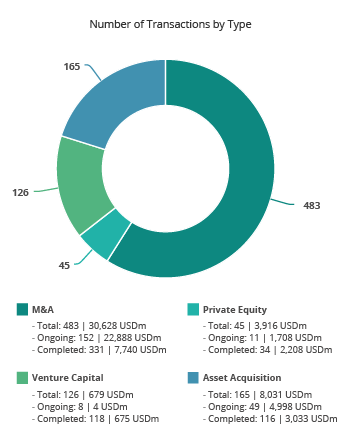

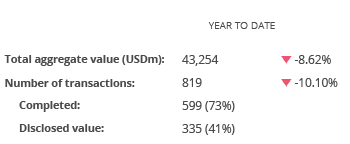

Capital movilizado en el mercado M&A de América Latina registra USD 43.254m hasta mayo de 2019

129 operaciones registradas en el mes alcanzan un importe de USD 5.655,53m

Chile y Colombia son los países que registran los mejores resultados de 2019

El mercado transaccional de América Latina ha registrado, en los cinco primeros meses del año, un total de 819 transacciones, de las cuales 335 registran un importe conjunto de USD 43.254m, lo que implica decrementos del 8,62% en el número de operaciones y una disminución del 10,10% en el importe de estas, con respecto al mismo periodo del año pasado, según el más reciente informe de Transactional Track Record.

Por su parte, en el mes de mayo se han contabilizado un total de 129 operaciones, de las cuales 52 tienen un importe no confidencial que suman aproximadamente USD 5.655,53.

Estas cifras implican un aumento del 4,03% en el número de operaciones, así como un descenso del 24,95% en el importe de las mismas, con respecto a mayo de 2018.

Ranking de Operaciones por Países

Según datos registrados hasta el mes de mayo, por número de operaciones, Brasil lidera el ranking de países más activos de la región con 453 operaciones (pese al descenso del 8%), con un descenso del 6% en el capital movilizado en términos interanuales (USD 25.628m). Le sigue en el listado México, con 112 operaciones (un descenso del 30%), y con una baja del 2% de su importe con respecto al mismo periodo de 2018 (USD 9.413m).

Por su parte, Chile sube una posición en el ranking y se posiciona como uno de los países con resultados positivos en la región, con 90 operaciones (un aumento del 6%), y con un aumento del 69% en el capital movilizado (USD 4.112m). Colombia, otro de los países que registra resultados positivos en la región, contabiliza 83 operaciones (un aumento del 17%), y un alza del 62% en el capital movilizado (USD 2.250m).

Entre tanto, Perú aumenta una posición y registra 55 operaciones (una baja del 19%), con una disminución del 56% en su importe respecto al mismo periodo del año pasado (USD 1.920m). Por su parte, Argentina se ubica en el último lugar por número de operaciones, con 54 operaciones (caída del 44%) y con un descenso del 51% en su capital movilizado (USD 2.019m).

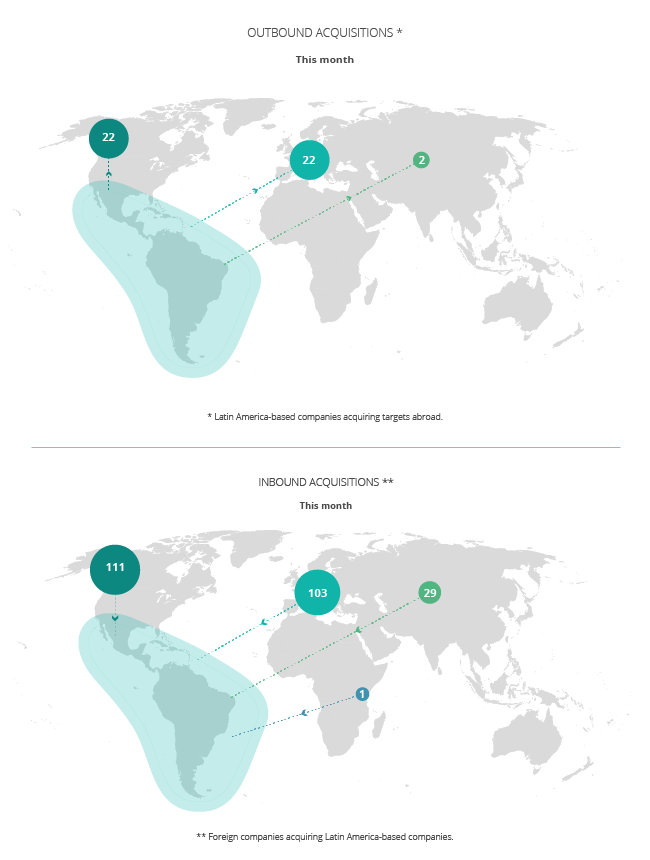

Ámbito Cross-Border

En el ámbito cross-border se destaca en mayo el apetito inversor de las compañías latinoamericanas en el exterior, especialmente en Europa y Norteamérica, donde se han llevado a cabo 22 operaciones en cada región. Por su parte, las compañías que más han realizado operaciones estratégicas en América Latina proceden de Norteamérica y Europa, con 111 y 103 operaciones respectivamente.

PrivateEquity y Venture Capital

Hasta mayo se han contabilizado un total de 45 operaciones de Private Equity, de las cuales 20 han registrado un importe de USD 3.916m, lo cual supone una disminución del 27,42% en el número de operaciones y un descenso del 13,15% en el importe de las mismas, con respecto al mismo periodo de 2018.

Por su parte, en el mercado de Venture Capital se han llevado a cabo 126 transacciones, de las cuales 81 registran un importe agregado de USD 679m, lo que corresponde a un descenso del 12,50% en el número de operaciones y una baja del 45,21% en el importe de las mismas, con respecto a mayo del año pasado.

La operación, que ha registrado un importe de USD 156m, ha estado asesorada por Garrigues Perú; Clifford Chance US; DLA Piper Pizarro Botto Escobar; Estudio Echecopar; y Rebaza, Alcázar & De Las Casas. Por la parte financiera, la operación ha estado asesorada por Macroinvest – Grupo Macro.

DealMaker Q&A

Posted on

TTR DealMaker Q&A with UNE Asesores Financieros Partner Eduardo Peláez

Eduardo Peláez

Eduardo Peláez is Partner of UNE Asesores Financieros, an M&A advisory boutique focused in Latin America Small/Mid-Market. Eduardo Peláez has conducted many transactions in diverse sectors including tourism, chemicals, real estate and agriculture. Previously Eduardo was associate of Miranda & Amado Abogados and Hernández & Cía. Abogados. Also, worked in Lindley.

He is Lawyer from Pontificia Universidad Católica del Perú and holds a MSc Management from Alliance Manchester Business School.

TTR: What’s your general outlook for the M&A market in Latin American this year, and specifically, in Peru?

EP: We believe the Latin American M&A market is experiencing a quite dynamic phase. Notwithstanding, the particular circumstances of each country in terms of macroeconomic conditions and political environment lead to diverse possibilities and projections.

In the region there are markets like Venezuela, a country with enormous potential but absolutely isolated, but also the case of Chile, a nation with very stable economy and government, but with less opportunities for high returns. Also, there are some up-and-coming countries like Paraguay that has established favorable market conditions through a pro-investment regulatory and tax set of rules.

The case of Peru is very particular. Despite of the political turbulence and the scandals of corruption, the economy is stable and the National Central Bank maintains its growth´s projections around 4%. The last two years have been marked by iconic transactions led by strategic investors pursuing market consolidation, such as the acquisition of the pharmacy chain MiFarma by Intercorp and the recent acquisition of Intradevco by Alicorp.

TTR: What are the primary factors influencing M&A decisions in the current economic climate? How do these economic fluctuations affect investment priorities?

EP: In the last decade, Peru has grown consistently. Even though the pace slowed since 2014, the Peruvian market maintains healthy indexes and presents opportunities for high returns, making it one of the most attractive markets in Latin America.

Likewise, the Private Equity industry is taking more prominence in Peru, generating more dynamism in M&A activity. Global funds like Advent and Carlyle are already active investors in the Peruvian market. Also, there are other relevant players specialized in the mid-market such as HIG, L Catterton, Southern Cross and Victoria Capital Partners, that are exploring opportunities in Peru.

From the sell-side standpoint, the political instability could make some businesses owners’ deciding to sell. Also, the new M&A regulation that will go into effect next year could accelerate the velocity of transactions and increase the volume of deals in the following months.

TTR: What is the state of the capital market in Perú? How has the country evolved in this respect in recent years? What is your forecast for the near-term?

EP: Peruvian capital market is still in an embryonic stage, characterized by low activity and hardly influenced by a few institutional investors. The exclusion of Credicorp from the FTSE Emerging Markets index is symptomatic.

There are some significant efforts of developing the MAV (capital market for mid-size companies with less than S/. 350MM of annual revenue), but the results are modest, with just 13 listed companies since its inception in 2013.

In this context, the recent creation of FIRBIs and FIBRAs, vehicles that have similarities with the American REITs, could represent a great opportunity to attract retail investors and increase the activity and liquidity of the capital market.

TTR: How difficult is it for corporates to access financing from local financial institutions in the current environment? What are the main barriers? How is financing structured?

EP: We have experienced a significant evolution in the volume of Peruvian companies accessing to the banking system in the past few years, going from 25% in 2014 to 40% in 2018, according to ASBANC.

The big challenge is the inclusion of the majority of small and medium enterprises that currently have very few options. The fintech market represents a very interesting alternative for this type of businesses, particularly in the way of factoring platforms.

Also, the increasing presence of foreign debt funds, especially Chilean, are becoming key participants, even in the small-and-mid size market. For example, recently we helped our client Llaxta Inmobiliaria y Constructora to obtain a US$ 10.5MM loan from Volcom Capital Chile for a real estate project in Piura, part of the social program “Techo Propio”.

TTR: Finally, we would like you to share with us your opinions and forecasts about the opening of the Peruvian market with other countries

EP: The Peru market presents many opportunities for all types of international investors, from strategic regional players to family offices and private equity and debt funds.

Beyond the usual M&A activity in the mining sector, we see interesting opportunities of consolidation in the agricultural business. For example, there is the case of Hortifrut that became the leading berry producer in the world after the acquisition of El Rocío. Likewise, last year we had the opportunity to advise the British trader Wealmoor and Limones Piuranos in the acquisition of the mango and avocado´s exporter Sunshine. Also, recently we led the sale of the mango´s exporter Dominus to the Peruvian-Danish joint venture Danper.

On the other hand, the real estate market still presents superiors return rates compared with other countries in Latin America, attracting global and regional real estate funds.

Finally, considering the current development of modern retail, we believe Peru represents an interesting possibility for regional companies dedicated to services related with cold chain and specialized storage.

Informe México – Mayo 2019

Posted on

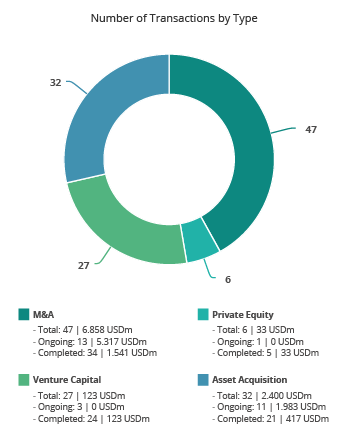

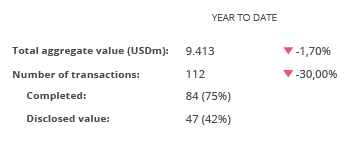

Fusiones y adquisiciones en México registran 112 operaciones hasta mayo de 2019

En el mes se han registrado 19 transacciones en el país por USD 810,14m

A lo largo de 2019 se han registrado 112 transacciones y un importe de USD 9.413m

Sector Tecnología, el más destacado del año, con 20 operaciones

El mercado de M&A en México ha contabilizado en los cinco primeros meses del año un total de 112 transacciones, de las cuales 47 registran un importe conjunto de USD 9.413m, de acuerdo con el informe mensual de Transactional Track Record. Estos datos reflejan un descenso del 30 % en el número de operaciones y del 1,70% en el importe de estas, con respecto al mismo período de 2018.

De las 47 operaciones contabilizadas en 2019 con importe revelado, el 3,58% hace parte de operaciones menores a USD 1m; el 9,12% pertenece a operaciones entre USD 1m y USD 10m; el 16,94% hace parte a operaciones entre USD 10m y USD 50m; el 7,17% pertenece a operaciones entre USD 50m y USD 100m; el 8,79% hace parte de operaciones entre USD 100m y USD 500m; y el 6,51% pertenece a operaciones mayores a USD 500m.

En términos sectoriales, el sector de Tecnología es el que más transacciones ha contabilizado a lo largo del año, con un total de 20, seguido por el sector Internet, con 16 registros.

Ámbito Cross-Border

Por lo que respecta al mercado cross-border, a lo largo del año las empresas mexicanas han apostado principalmente por invertir en España, con 8 operaciones, seguido de Estados Unidos con 7 transacciones, además de Colombia y Perú, con 3 negocios registrados en cada país. Por importe destaca Brasil, con USD 912,13m.

Por otro lado, Estados Unidos, es el país que más ha apostado por realizar adquisiciones en México, con 12 operaciones, seguido de Reino Unido, con 5 transacciones, y España y Japón, con 4 operaciones en cada país. Por importe, se destaca en este periodo España, con USD 2.947,22m.

Private Equity y Venture Capital

En lo que va de año se han producido un total de 6 transacciones de Private Equity valoradas en USD 33m, con una tendencia bajista de 64,71% en el número de operaciones y del 98,13% en el capital movilizado con respecto a mayo de 2018.

Por su parte, en 2019 se han contabilizado 27 operaciones de Venture Capital, con un descenso del 12,90%, y un capital movilizado de USD 123m en 14 transacciones divulgadas, lo cual representa un descenso del 55,30% con respecto al mismo periodo del año anterior.

Transacción Destacada

Para mayo de 2019, Transactional Track Record ha seleccionado como operación destacada la relacionada con el Grupo Industrial Saltillo (GIS), el cual ha completado la venta del negocio de calentadores a Ariston Ther.

La operación, que ha registrado un importe de USD 144,22m, ha estado asesorada por la parte legal por Santamarina y Steta Abogados; Galicia Abogados; Ariston Thermo Group y Grupo Industrial Saltillo (GIS).

En la parte financiera, la transacción ha sido asesorada por HSBC México.

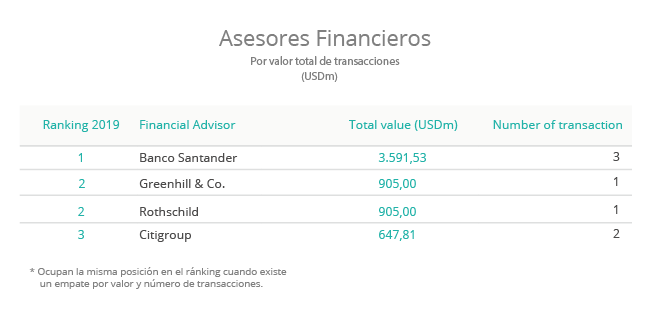

Ranking de Asesores Legales y Financieros

En el ranking TTR de asesores financieros, por número de operaciones, lidera en los cinco primeros meses de 2019 RIóN M&A – Global M&A México, con 4 operaciones. Por importe, se destaca hasta el mes de mayo Banco Santander, con USD 3.591,53m.

En cuanto al ranking de asesores jurídicos, por importe, lidera la firma Todd & Asociados con USD 1.005,90m y, por número de transacciones, el ranking es liderado por Galicia Abogados con 5 operaciones asesoradas.

Subscribe to our free newsletter:

This website uses cookies. By continuing to browse the site, you are agreeing to our use of cookies