Mercado transaccional en México cae un 25% hasta mayo de 2020

En mayo se han registrado 11 transacciones en el país por USD 145,65m

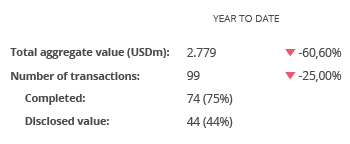

A lo largo de 2020 se han registrado 99 transacciones

Adquisiciones extranjeras en Tecnología e Internet han disminuido un 50% en 2020

Sector Financiero y de Seguros, el más destacado del año con 16 operaciones

El mercado de M&A en México ha contabilizado en mayo de 2020 un total de 11 fusiones y adquisiciones, entre anunciadas y cerradas, por un importe agregado de USD 145,65m, de acuerdo con el informe mensual de Transactional Track Record.

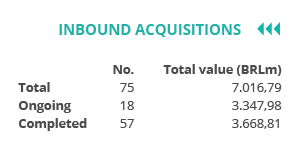

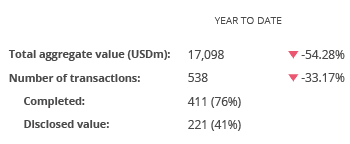

Por su parte, en los cinco primeros meses del año se han producido un total de 99 transacciones, de las cuales 44 registran un importe conjunto de USD 2.779m, lo que implica un descenso del 25% en el número de operaciones y una disminución del 60,60% en el importe de estas, con respecto al mismo período de 2019.

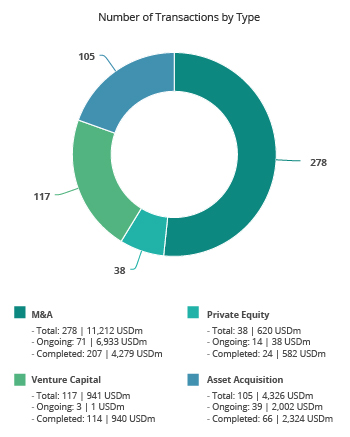

En términos sectoriales, el Financiero y de Seguros ha sido el más activo del año, con un total de 16 transacciones, seguido por el de Internet, con 15.

Ámbito Cross-Border

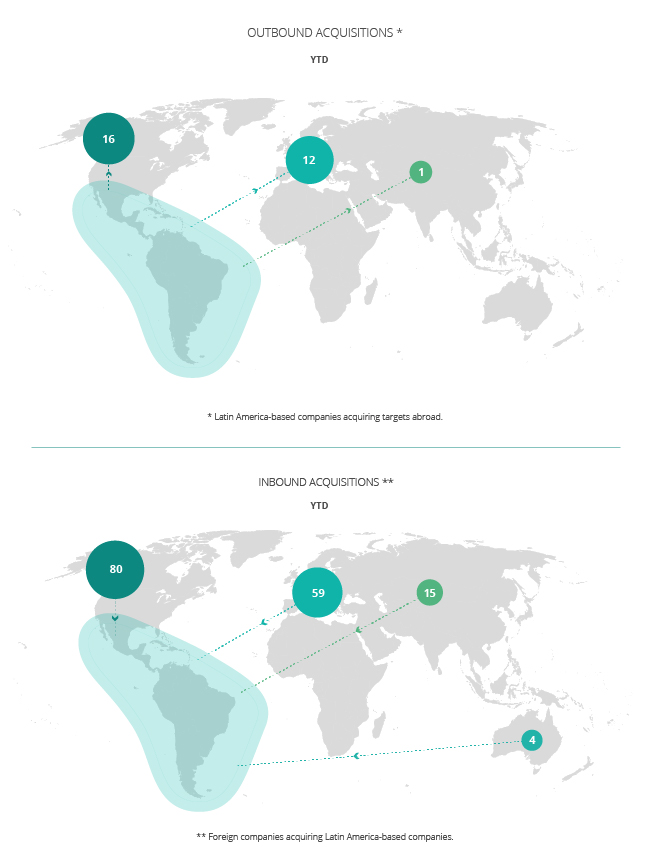

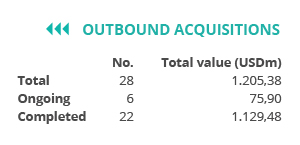

Por lo que respecta al mercado cross-border, a lo largo de 2020 las empresas mexicanas han apostado principalmente por invertir en Estados Unidos, con 11 operaciones, seguido de España, con 5 transacciones. Por importe destaca Estados Unidos, con USD 910,95m.

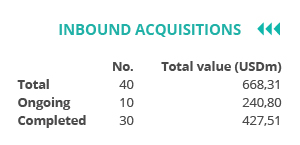

Por otro lado, Estados Unidos, es el país que más ha apostado por realizar adquisiciones en México, con 19 operaciones, seguido de Chile y Canadá, con 5 transacciones en cada país. Por importe, se destaca Estados Unidos, con USD 198,32m.

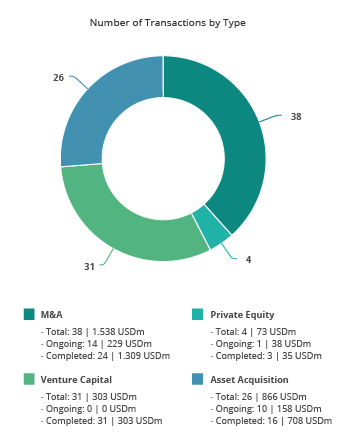

Private Equity, Venture Capital y Asset Acquisitions

Hasta mayo de 2020 se han contabilizado un total de 4 operaciones de Private Equity por USD 73m, lo cual supone un descenso del 55,56% en el número de operaciones y un aumento del 7,98% en el importe de éstas, con respecto al mismo periodo del año anterior.

Por su parte, en el segmento de Venture Capital se han contabilizado hasta mayo un total de 31 operaciones con un importe agregado de USD 303m, lo que implica un descenso del 13,89% en el número de operaciones y un alza del 132,09% en el importe de las mismas en términos interanuales.

En el segmento de Asset Acquisitions, hasta el mes de mayo se han registrado 26 operaciones, por un valor de USD 866m, lo cual representa una disminución del 23,53% en el número de operaciones, y un descenso del 62,83% en el importe de estas, con respecto a mayo de 2019.

Transacción Destacada

Para mayo de 2020, Transactional Track Record ha seleccionado como operación destacada la inversión de Aztecavo, por parte de HMC, por un valor de USD 145m.

La operación ha estado asesorada por Nader Hayaux & Goebel Abogados.

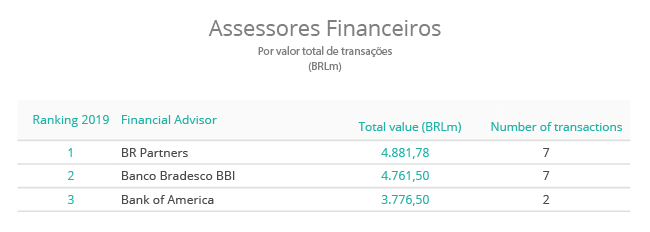

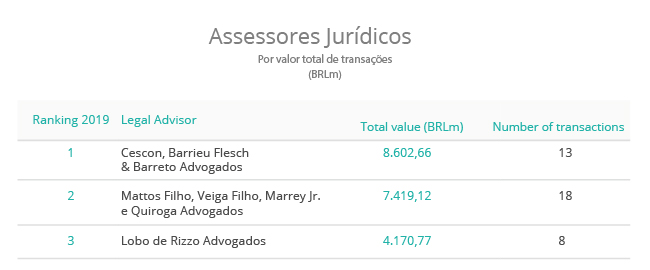

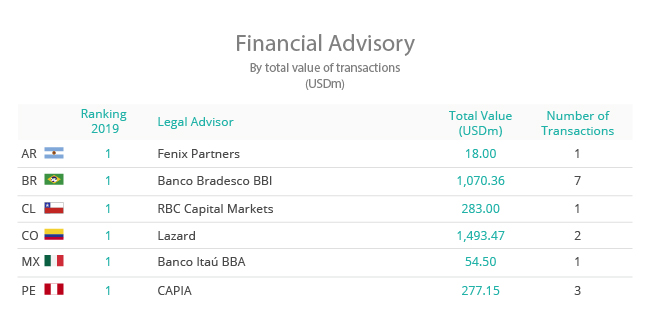

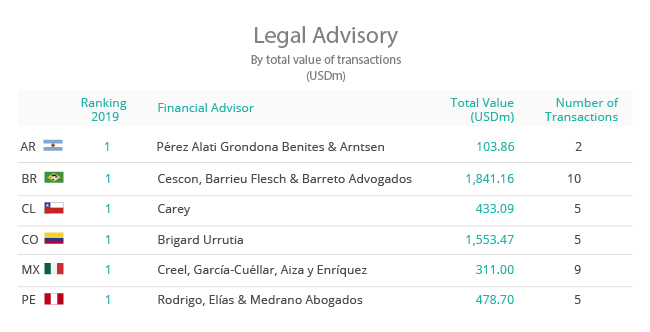

Ranking de Asesores Financieros y Legales