Las operaciones de M&A en Perú disminuyen un 43% en el tercer trimestre de 2020

En los nueve primeros meses de 2020 se han registrado 63 transacciones por USD 859m

El sector Inmobiliario es el más destacado del año, con 11 operaciones

Patrocinado por:

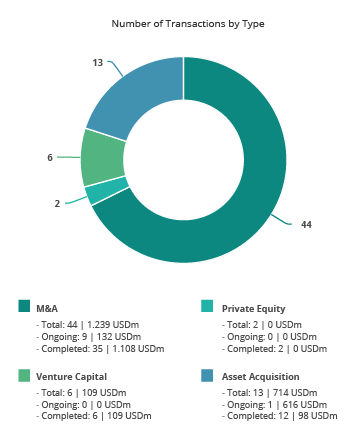

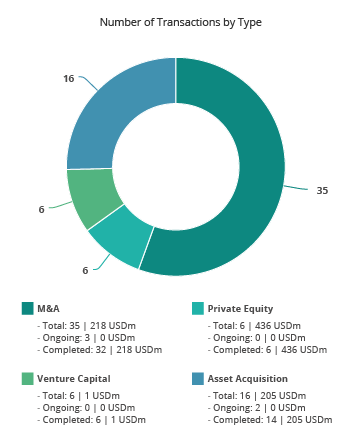

El mercado transaccional peruano ha registrado en los nueve primeros meses del año un total de 63 fusiones y adquisiciones, entre anunciadas y cerradas, por un importe agregado de USD 859m, según el informe trimestral de Transactional Track Record con la colaboración de Intralinks. Estas cifras suponen una disminución del 42,73% en el número de operaciones y un descenso del 88,55% en el importe de las mismas, con respecto al mismo periodo de 2019.

Por su parte, en el tercer trimestre de 2020 se han contabilizado un total de 22 operaciones con un importe agregado de USD 268,30m.

En términos sectoriales, el Inmobiliario es el más activo del año, con un total de 11 transacciones, seguido por el sector de Financiero y de Seguros, con 9 deals.

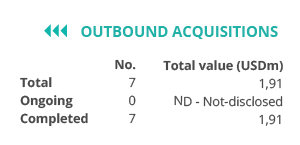

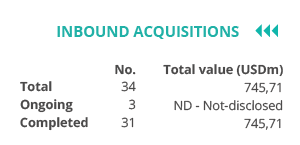

Ámbito Cross-Border

Por lo que respecta al mercado Cross-Border, en lo que va de año las empresas peruanas han apostado principalmente por invertir en Chile, con 2 transacciones y USD 1,50m.

Por otro lado, Estados Unidos y Chile son los países que más han apostado por realizar adquisiciones en Perú, con 11 y 6 operaciones, respectivamente. Por importe, destaca Reino Unido, con USD 277,15m

Private Equity y Venture Capital

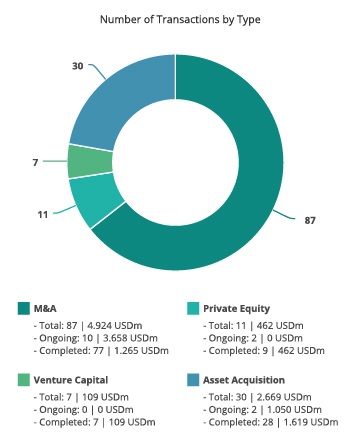

Hasta el tercer trimestre de 2020 se han producido un total de 6 transacciones de Private Equity, lo cual representa una disminución del 33% en el número de operaciones con respecto al tercer trimestre de 2019.

Por su parte, en los nueve primeros meses de 2020, Perú ha registrado 6 operaciones de Venture Capital lo que representa una disminución del 14,29% en el número de operaciones con respecto al mismo periodo del año pasado.

Asset Acquisitions

En el mercado de adquisición de activos, se han cerrado en el tercer semestre del año 16 transacciones con un importe de USD 205m, lo cual implica un descenso del 38,46% en el número de operaciones y un descenso del 89,15% en su importe con respecto al mismo periodo de 2019.

Transacción Destacada

Para el tercer trimestre de 2020, Transactional Track Record ha seleccionado como operación destacada la adquisición de Orazul Energy Perú por parte de ISA.

La operación, valorada en USD 158,50m, ha estado asesorada por la parte legal por Estudio Echecopar, Baker McKenzie US, Rodrigo, Elías & Medrano Abogados y White & Case US. Por la parte financiera, la operación ha sido asesorada por Scotiabank Perú.

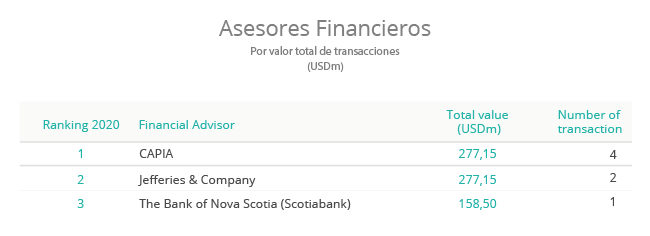

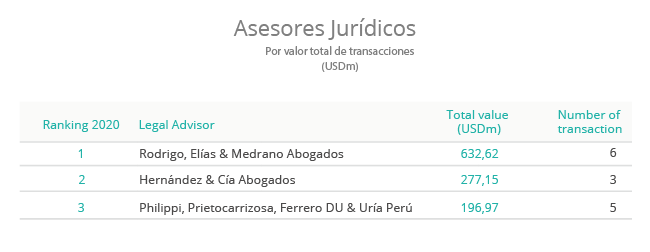

Ranking de Asesores Legales y Financieros