Mercado M&A peruano registra disminución del 16% en 2022

- En 2022 se han registrado 109 transacciones por USD 2.572m

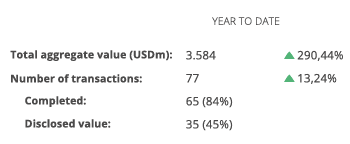

El mercado transaccional peruano ha registrado en 2022 un total de 109 fusiones y adquisiciones, entre anunciadas y cerradas, por un importe agregado de USD 2.572m, según el informe anual de TTR Data. Estas cifras suponen un descenso del 16% en el número de transacciones y un descenso del 25% en su importe, con respecto a 2021.

En términos sectoriales, el sector de Banca e Inversión es el más activo del año, con un total de 17 transacciones, junto con el sector de Servicios Profesionales, con 16 transacciones y un crecimiento del 183% y 60%, respectivamente, con respecto al año pasado.

Ámbito Cross-Border

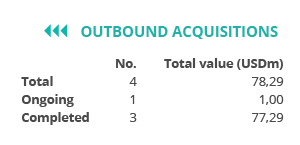

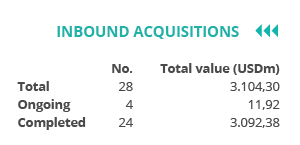

En lo que respecta al mercado Cross-Border, en 2022 las empresas peruanas han apostado principalmente por invertir en Colombia, con seis transacciones en cada país. Por otro lado, Estados Unidos es el país que más ha realizado adquisiciones en Perú, con 22 transacciones y un importe de USD 1.151m.

Venture Capital

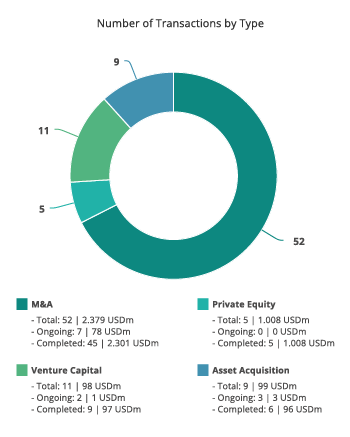

En 2022, se han contabilizado un total de 20 transacciones de Venture Capital, de las cuales 16 tienen un importe no confidencial agregado de USD 75m. Esto supone un aumento del 5% en el número de transacciones y un descenso del 44% en su importe, con respecto al año anterior.

Asset Acquisitions

En el mercado de adquisición de activos, se han cerrado en 2022 un total de nueve transacciones por USD 1.028m, lo cual implica un descenso del 31% en el número de transacciones y un alza del 538% en su importe, con respecto a 2021.

Transacción Destacada

Para 2022, TTR Data ha seleccionado como deal del año el relacionado con Newmont Mining, la cual ha adquirido una participación adicional del 43,65% en Yanacocha a Minas Buenaventura. El importe de la transacción ha sido USD 300m.

La transacción ha cotado con el asesoramiento jurídico de Estudio Rubio Leguía Normand y García Sayán Abogados. Por la parte financiera, la transacción ha sido asesorada por Scotiabank.

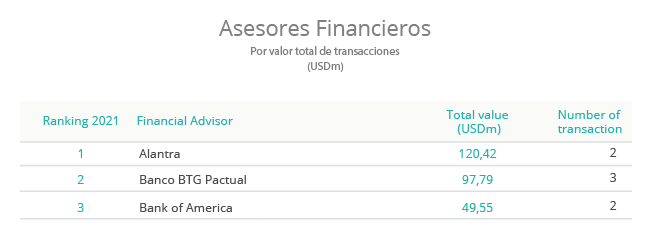

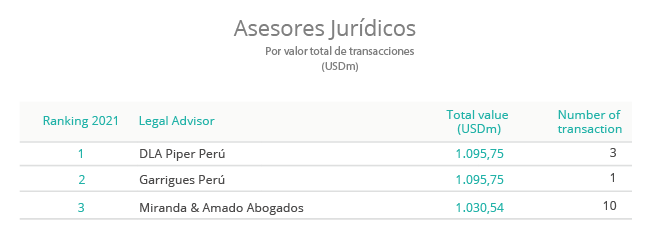

Ranking de Asesores Jurídicos y Financieros

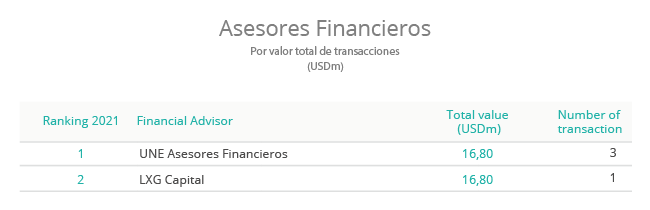

En el ranking TTR Data de asesores financieros, por importe, lideran en 2022 Bank of America y Citigroup, con USD 736m. Por número de transacciones, lidera UNE Asesores Financieros, con cuatro transacciones.

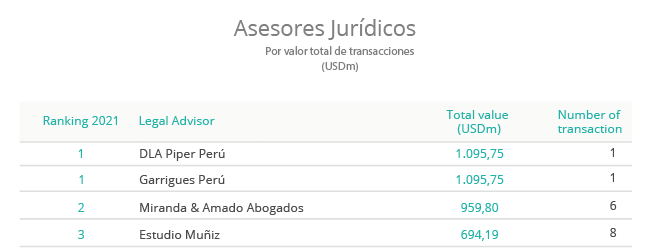

En cuanto al ranking de asesores jurídicos, por importe, lidera en 2022 Rodrigo, Elías & Medrano Abogados, con USD 977m y, por número de transacciones, lidera Estudio Muñiz, con 14 transacciones asesoradas.