Matias focuses his practice on corporate and securities law, mainly corporate governance, mergers and acquisitions, capital markets, project finance and venture capital matters. Matias has previous experience at other firms in the US and in Chile.

TTR – How would you describe the current situation of M&A market in Latin America, now we are over the worst part in terms of paralysis of economic activity?

M. Z. – Improving. Obviously was impacted by Covid-19, in the sense that a significant number of deals were in a stand-by mode in March-April with only the deals that were in a later stage moving forward. However, since then the activity and interest has grown up, mainly because targets are cheaper now creating an increased pool of opportunities and also because companies, after the initial shock have restarted their “normal” operations.

TTR – How would you describe the measures taken by the Chilean Government and, in general, in Latin America, for the situation of business instability caused by the health crisis? Do you think additional measures are necessary?

M. Z. – As a trial/error effort. I think that nobody was able to predict this pandemic and its effects in any country or region. There have been efforts more focalized in health aspects and others in the economic aspects and to be able to balance both have proved to be challenging to say the least. In the case of Chile, I believe that most of these efforts have been positive not necessarily to counterbalance the negative effects but to avoid deepening such negative effects.

TTR – In terms of company restructurings, what is the current situation and what are the prospects for the following months in Chile and the region?

M. Z. – There have been several cases of large companies entering into reorganization proceedings within the insolvency framework, either locally or abroad, such as in the cases of Latam Airlines (Chapter 11) or Enjoy and others taking the opportunity to restructure its liabilities because of better financial conditions. We believe that, depending on for how long this pandemic remains, more companies will start restructuring proceedings although a significant number have taken the appropriate measures during H1 of this year,

TTR – What type of companies has been more affected by COVID-19 in Chile and LatAm?

M. Z. – Those heavily reliant in their cash Flow to operate instead of having a strong balance sheet and those in industries more cyclical such as hospitality, airlines, tourism in general. In other industries the results have been mixed with some having really good results.

TTR – Regarding DLA Piper Chile’s advice on the acquisition of Cornershop in Latin America by Uber, how will you assess the evolution of Venture Capital transactions, both in Chile and Latin America despite the current uncertain environment?

M. Z. – Growing. The tech sector in general has been a highlight during the pandemic, as a significant number of them have seen an extraordinary demand for their products and services in multiple verticals, gaining traction and therefore having higher valuations and attracting investment not only from VC firms but also from CVC and family offices. In fact, many of them have taken the opportunity to raise money to be sure that have enough runway to keep growing in these trouble waters.

TTR – Regarding the M&A sector, do you think the health crisis has generated business opportunities? Which sectors do you think are more interesting for financially strong investors?

M. Z. – Absolutely yes. There are more companies that are for sale as the effects of the pandemic remains and will remain for a while, specially if such transaction creates a cash-out opportunity in the case of family-controlled companies. Has also created opportunities in case of multinational companies that are becoming more focused in their core business. Investors that have more appetite for risk are looking for opportunities in the sectors more heavily affected by the crisis, like Hospitality and transportation.

Mauricio Borrero – Dentos Cardenas & Cardenas: Co-head of M&A and Corporate groups, and is the head of the Latin American and Caribbean region Corporate practice group.

—————————————–

The M&A activity in 2020 is severely affected by the COVID-19 health crisis. How would you describe the situation of the M&A players in Colombia and LatAm at this time?

After coming nearly to a halt as a result of the Coronavirus, the M&A market is starting to recuperate.In general terms, traditional M&A players such as strategic buyers and private equity funds, are currently focusing on protecting the value of their own companies and assets rather than entering into new transactions. Nonetheless, those strategic buyers and funds that have available cash, are now starting to actively look for potential targets to acquire. This stems from the fact that the crisis has created a buyer’s market for M&A, with bargain prices and multiple investment opportunities.This is particularly evident for strong LatAm companies investing in other countries of the region, as well as acquisitions of companies with a strong reputation and global presence.With an increase in the negative financial effects of the crisis in local companies, especially in the leisure, transport, hospitality, and real estate sectors, it is likely that we will have a surge in distressed M&A transactions during the second semester of 2020 and Q1 and Q2 of 2021.

Which sectors would you say are more affected by this situation? Which ones do you think are most likely to recover more quickly?

Although this crisis has affected the entire economy, the most affected sectors are leisure, transportation, hospitality, and real estate. The oil and gas sector has also been affected by both COVID-19 and a reduction of the international prices of crude oil. We consider that the sectors that are more likely to recover quickly will be pharmaceutical, manufacturing, and technology.

What regulatory measures do you think could be deployed to unblock the current situation?

The most critical point is to re-open the economy, with a controlled opening of air travel. The Colombian government needs to increase the available funds for the different financial stimulus packages (i.e. Colombia Responde, Colombia Responde para Todos, etc.), to provide liquidity to local companies. The payment ecosystem needs to be enhanced by enabling new players and different options for the circulation of money and payment mechanisms different than traditional means such as cash. This will also serve to give access to credit and some level of formalization to more individuals and businesses. Defining what economic sectors are key in the “new dynamic” and promote them with subsidized funding and/or tax incentives.

What is the situation of the M&A market in Colombia compared to other nearby countries? Is this stagnation being lived in the same way in other countries in LatAm?

The current situation of the Colombian M&A Market is fairly similar to our peers in LatAm. We have been monitoring the situation with our M&A partners of the region and we have seen that they have all experienced a slowdown in the number and size of M&A deals. We have also evidenced that through the LatAm region there is an increased interest from strategic buyers and private equity sponsors to acquire companies and/or assets at a bargain price. Currently, Dentons Latin America and the Caribbean is participating in several intra-region transactions and international M&A deals involving more than three countries of the region.

What should we expect in the following months? Do you believe it is still possible to get back to normal in 2020?

We consider that the M&A market in Colombia will continue to grow during the following months, but it will not reach the number and size of deals of the previous years. These transactions will be more difficult and the entire process may take longer. All participants of the M&A market will face difficult times ahead when determining the fair market value of the asset/company being acquired, and securing financing at reasonable rates. Moreover, the social distancing rules will affect the negotiation process, as “all hands on deck” negotiations will be difficult to achieve. The time for performing a due diligence process will also be affected, as the collection of documents will become more difficult for the target company, given the limitations for their personnel to be physically present at their offices. We also consider that governmental approvals when required will take longer to be issued. An increase in distressed M&A deals is evident, and will probably be one of the drivers of the M&A market during the following 18 to 24 months. I believe we will only get back to normal during 2023.

———————————————

Versión en español

La actividad transaccional en 2020 está sin duda muy marcada por la crisis sanitaria del COVID-19, ¿cómo describiría la situación de los players del mercado transaccional en Colombia y de la región en estos momentos?

Después de casi detenerse como resultado del Coronavirus, el mercado de fusiones y adquisiciones está comenzando a recuperarse. En términos generales, los actores tradicionales de fusiones y adquisiciones, tales como compradores estratégicos y fondos de capital privado, se están centrando actualmente en proteger el valor de sus propias compañías y activos, en lugar de llevar a cabo nuevas transacciones. Sin embargo, los compradores estratégicos y fondos que tienen efectivo disponible, ahora están comenzando a buscar activamente posibles objetivos para adquirir. Esto se debe al hecho que la crisis ha creado un mercado de compradores para fusiones y adquisiciones, con precios reducidos y múltiples oportunidades de inversión. Esto es particularmente evidente para las compañías latinoamericanas que invierten en otros países de la región, así como para las adquisiciones de compañías con una sólida reputación y presencia global. Con un aumento en los efectos negativos financieros de la crisis en las empresas locales, especialmente en los sectores de entretenimiento, transporte, hotelería e inmobiliario, es probable que tengamos un aumento en las transacciones de “distressed M&A” durante el segundo semestre de 2020 y los dos primeros trimestres de 2021.

¿Qué sectores diría usted que se han visto más afectados por esta situación? ¿Cuáles experimentarán una recuperación más rápida?

Aunque esta crisis ha afectado a toda la economía, los sectores más afectados son el de entretenimiento, transporte, hotelero e inmobiliario. El sector del petróleo y el gas también se ha visto afectado tanto por COVID-19 como por la reducción de los precios internacionales del petróleo crudo.

¿Qué medidas cree que podrían tomarse a nivel regulatorio para desatascar esta paralización?

El punto más crítico es reabrir la economía, con una apertura controlada de los viajes aéreos. El gobierno colombiano necesita aumentar los fondos disponibles para los diferentes paquetes de estímulo financiero (es decir, Colombia Responde, Colombia Responde para Todos, etc.), para proporcionar liquidez a las empresas locales. El ecosistema de pagos debe mejorarse permitiendo nuevos jugadores y diferentes opciones para la circulación de dinero y mecanismos de pago diferentes a los medios tradicionales como el efectivo. Esto también servirá para dar acceso al crédito y cierto nivel de formalización a más individuos y empresas. Definir qué sectores económicos son clave en la “nueva dinámica” y promoverlos con financiamiento subsidiado y/o incentivos tributarios.

¿En qué situación se encuentra Colombia respecto a la actividad transaccional de otros países de su entorno? ¿Esta paralización que vivimos se traslada de igual manera a otros países de América Latina?

La situación actual del mercado colombiano de fusiones y adquisiciones es bastante similar a la de nuestros pares en LatAm. Hemos estado monitoreando la situación con nuestros socios de M&A de la región y hemos visto que todos han experimentado una desaceleración en el número y tamaño de las transacciones de M&A.También hemos evidenciado que en la región de LatAm hay un mayor interés de compradores estratégicos y sponsors de capital privado para adquirir empresas y/o activos a un precio reducido. Actualmente, Dentons Latinoamérica y el Caribe está participando en varias transacciones intrarregionales y acuerdos internacionales de fusiones y adquisiciones que involucran a más de tres países de la región.

¿Qué cabe esperar que suceda en los próximos meses? ¿cree usted que se podrá recuperar la normalidad en 2020?

Consideramos que el mercado de fusiones y adquisiciones en Colombia continuará creciendo durante los próximos meses, pero no alcanzará la cantidad y el tamaño de las transacciones de los años anteriores. Estas transacciones serán más difíciles y puede que todo el proceso dure más tiempo. Todos los participantes en el mercado de fusiones y adquisiciones enfrentarán tiempos difíciles al determinar el valor justo de mercado del activo/empresa que se adquiere y asegurar el financiamiento a tasas razonables. Además, las reglas de distanciamiento social afectarán el proceso de negociación, ya que las negociaciones de “todas las partes sentadas en la misma mesa” serán difíciles de lograr. El tiempo para realizar un proceso de debida diligencia también se verá afectado, ya que la recopilación de documentos será más difícil para el target, dadas las limitaciones para que su personal esté físicamente presente en sus oficinas. También consideramos que las aprobaciones gubernamentales demorarán más en emitirse cuando sean necesarias. Se evidencia un aumento en las transacciones de “distressed M&A”, y probablemente este será uno de los motores del mercado de M&A durante los próximos 18 a 24 meses. Creo que sólo volveremos a la normalidad durante 2023.

4Q19 Energy Sector Spotlight – Latin America

Posted on

LatAm Energy M&A Up Overall in 2019 Real Estate sector leads Spanish transactional market, although 17.07% falls until December

Deal

volume down in Argentina and Mexico YoY

Oil

and gas transactions dominate regionally, despite 65% decline in Mexico

Solar

transactions outpace oil and gas deals in Chile, notwithstanding overall

decrease in renewable deals

Power

sector transactions increase throughout the region, except in Brazil

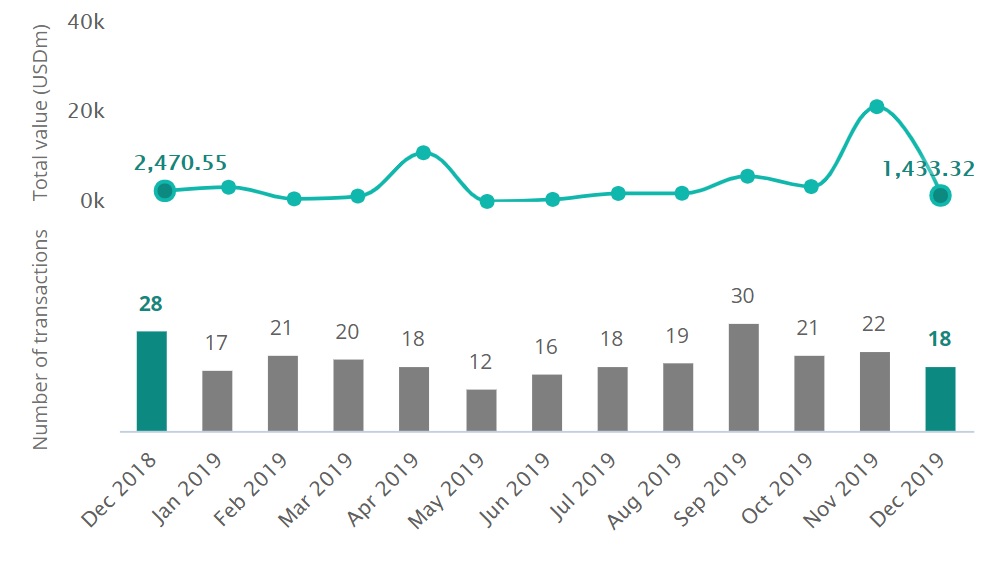

Madrid, 31 January, 2020. Deal volume in the energy sector across Latin America is down 5% to the close of 4Q19, while aggregate transaction value increased 153% over the same 12 months last year according to Transactional Track Record data.

Volume and aggregate value of energy sector in LatAm. December 2018 to December 2019. Source: Transactional Track Record

Brazil leads by the sheer number of energy deals across the region with 129 transactions, followed by Chile, which registered the sharpest upswing in aggregate value with a 190% increase to USD 2.9bn.

Colombia ranks third by number of energy deals with 27 for the year,

followed by Argentina with 25 and Peru with 15.

Mexico is in last place among the top six M&A markets in the region,

registering a 65% decline in energy sector transactions with just 13 deals to

the close of 4Q19.

Oil and gas transactions lead energy

sector deal volume in the top six M&A markets, with the exception of Chile

and Peru, where the number of transactions in the power sector outpaced

extractives. In the case of Colombia,

the oil and gas and power sectors were at par with seven deals apiece for the

year.

Conventional energy deals outpaced

renewables in every market except Chile, where there were more solar

transactions than oil and gas deals, despite a 33% drop in the number of solar

energy transactions over 2018. Investment

in wind assets fell across the board, except in Colombia, where wind deals

increased markedly over 2018.

Buyers based in the EU led inbound

dealmaking in the energy sector for the year, with 53 transactions, followed by

North American bidders, with 33 deals, ahead of buyers out of Asia, with 15

deals. The US led inbound energy investments in Brazil, Colombia and Mexico,

the UK led inbound energy deals in Argentina, Colombia led energy investments

in Peru and France dominated in Chile.

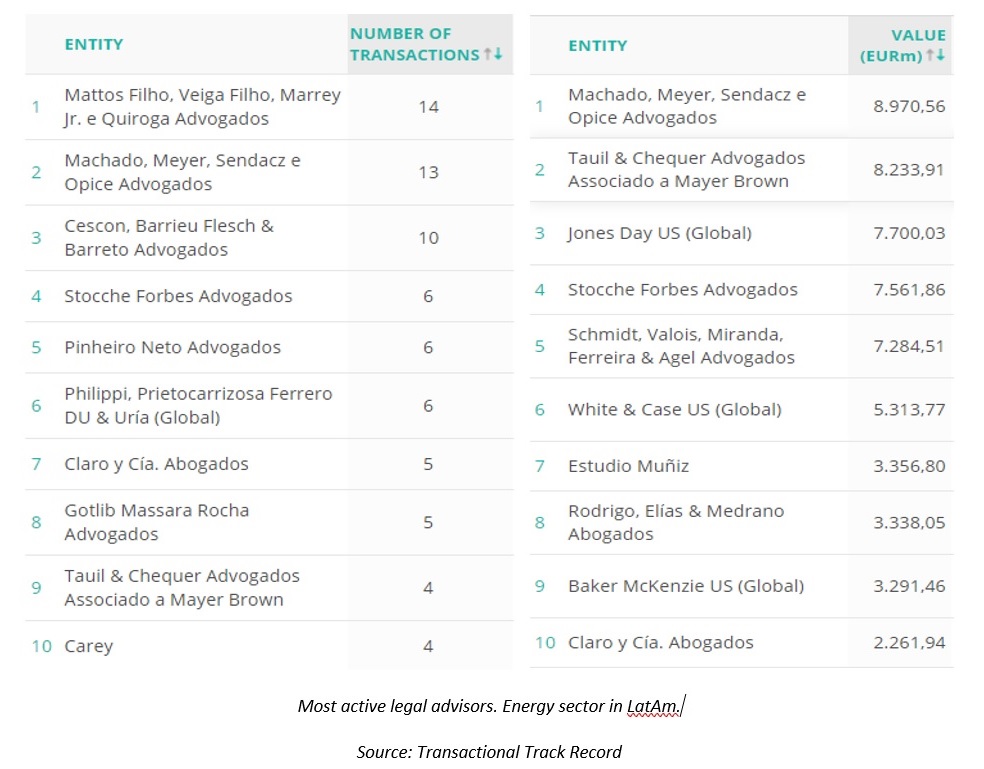

Mattos Filho, Veiga Filho, Marrey

Jr. e Quiroga Advogados tops the regional ranking with 14 transactions, while

Machado, Meyer Sendacz e Opice Advogados leads by aggregate value on deals

totaling just under USD 9bn.

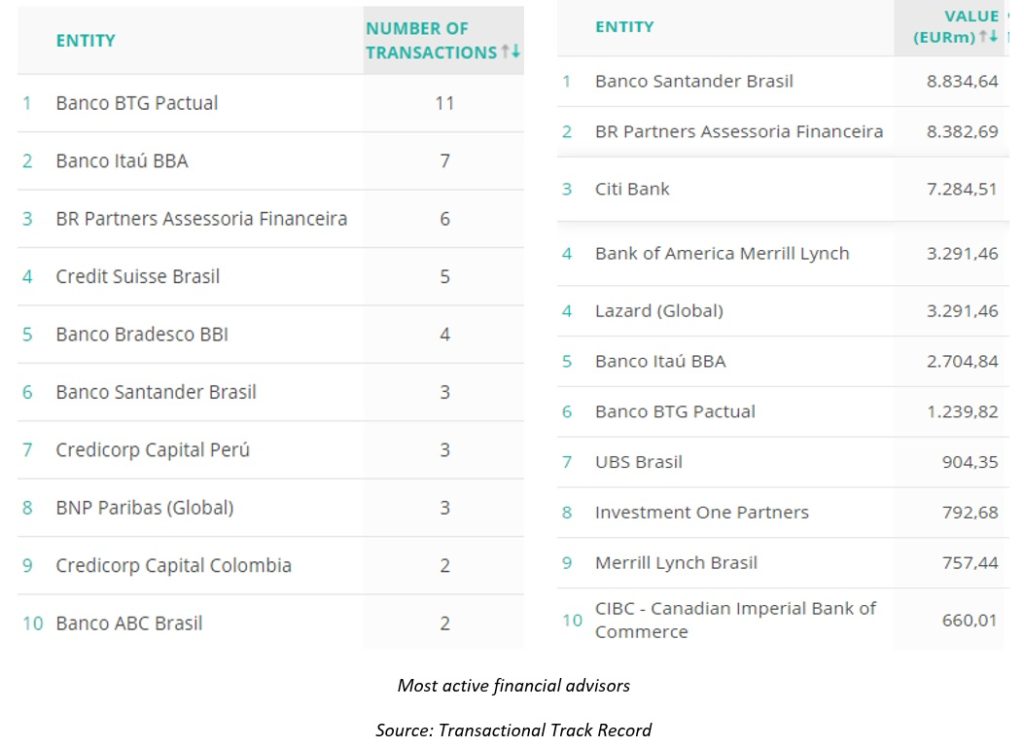

Banco BTG Pactual led energy sector dealmaking regionally in 2019 with 11 transactions worth a combined USD 1.24bn. Banco Santander leads by aggregate value, its three deals worth USD 8.83bn in aggregate.

TTR is a premium financial technology

platform that delivers unrivalled transactional data and actionable market

intelligence in real time, empowering professionals to seize opportunities and

make more informed strategic decisions. TTR aggregates transactional data from

thousands of sources, providing an indispensable resource of announced,

completed and cancelled transactions covering every industry.

DealMaker Q&A

Posted on

TTR DealMaker Q&A with PPU Peru Partner Rafael Boisset

Rafael Boisset, Partner in Philippi Prietocarrizosa Ferrero DU & Uría Perú, is an expert in corporate matters as well as mergers and acquisitions of private and listed companies in various industries of economy, representing both sellers and buyers. He has advised significant clients by his active participation in the strategic planning of acquisitions and corporate restructuring, project finance, and banking and corporate financing through capital markets. He has experience representing investment banks as well as companies that raise funds from international capital markets.

_____________________________________________

TTR – Firstly, Mr. Boisset, we would like you to share your opinion on the progress of the Peruvian market in 2019.

R. B. – Both the number and value of deals reported proved to be a quiet active year in terms of M&A transactions, which turns to be interesting considering the slowdown of the Peruvian economy and the political crisis we faced during the year and particularly in the last quarter. Once again the energy sector has been the most relevant in terms of size and complexity but we also saw relevant deals in the manufacturing industry, such as the Intradevco Industrial sell to Alicorp.

TTR – As an advisor in M&A deals, what could you tell us about the investors that show interest in Peru-based companies? What are the main attractions of those companies?

R. B. – I would say macroeconomic stability, low inflation, stable exchange rates, independency of the Central Bank, simplicity of its tax regime, and a deep potential growth of the middle class, which is an opportunity in several industries.

Despite the slowdown of the economy, Peru has proved to be a country, in which its macroeconomic fundamentals showed to be isolated from the political instability

TTR – In 2019, there was an interesting increase in agribusiness deals in the country. What can you tell us about that upsurge?

R. B. – Unlike other countries in the region, Peru’s large coast has some strategic keys for the agribusiness, such as predictable weather, access to ports for exportation, water supply and reasonable land prices and workforce costs. We have seen a consolidation of land and production of local investors in the last 10 to 15 years, that are now being acquired by bigger players that need such scale to invest.

TTR – What other sectors could potentially have a noteworthy increase in their activity in the mid-term? Why?

R. B. – It will of course depend on how the economy will move in the mid-term, but we expect that sectors related to the increase of the middle class be more active, such as education, retail, healthcare, and real estate.

Two other sectors that may be relevant are mining and infrastructure. In mining, the slowdown of commodity prices creates the need for some companies to divest and the opportunity to others to invest. In infrastructure, we expect the criminal trials to end in the midterm allowing new investors to acquire assets that the current conditions do not offer the transparency and security that are needed.

TTR – Lastly, what is your forecast for the next year?

R. B. – We believe it will be a very active year, probably even more active than 2019. Key sectors will be education, healthcare and manufacturing.

DealMaker Q&A

Posted on

TTR DealMaker Q&A with UNE Asesores Financieros Partner Eduardo Peláez

Eduardo Peláez

Eduardo Peláez is Partner of UNE Asesores Financieros, an M&A advisory boutique focused in Latin America Small/Mid-Market. Eduardo Peláez has conducted many transactions in diverse sectors including tourism, chemicals, real estate and agriculture. Previously Eduardo was associate of Miranda & Amado Abogados and Hernández & Cía. Abogados. Also, worked in Lindley.

He is Lawyer from Pontificia Universidad Católica del Perú and holds a MSc Management from Alliance Manchester Business School.

TTR: What’s your general outlook for the M&A market in Latin American this year, and specifically, in Peru?

EP: We believe the Latin American M&A market is experiencing a quite dynamic phase. Notwithstanding, the particular circumstances of each country in terms of macroeconomic conditions and political environment lead to diverse possibilities and projections.

In the region there are markets like Venezuela, a country with enormous potential but absolutely isolated, but also the case of Chile, a nation with very stable economy and government, but with less opportunities for high returns. Also, there are some up-and-coming countries like Paraguay that has established favorable market conditions through a pro-investment regulatory and tax set of rules.

The case of Peru is very particular. Despite of the political turbulence and the scandals of corruption, the economy is stable and the National Central Bank maintains its growth´s projections around 4%. The last two years have been marked by iconic transactions led by strategic investors pursuing market consolidation, such as the acquisition of the pharmacy chain MiFarma by Intercorp and the recent acquisition of Intradevco by Alicorp.

TTR: What are the primary factors influencing M&A decisions in the current economic climate? How do these economic fluctuations affect investment priorities?

EP: In the last decade, Peru has grown consistently. Even though the pace slowed since 2014, the Peruvian market maintains healthy indexes and presents opportunities for high returns, making it one of the most attractive markets in Latin America.

Likewise, the Private Equity industry is taking more prominence in Peru, generating more dynamism in M&A activity. Global funds like Advent and Carlyle are already active investors in the Peruvian market. Also, there are other relevant players specialized in the mid-market such as HIG, L Catterton, Southern Cross and Victoria Capital Partners, that are exploring opportunities in Peru.

From the sell-side standpoint, the political instability could make some businesses owners’ deciding to sell. Also, the new M&A regulation that will go into effect next year could accelerate the velocity of transactions and increase the volume of deals in the following months.

TTR: What is the state of the capital market in Perú? How has the country evolved in this respect in recent years? What is your forecast for the near-term?

EP: Peruvian capital market is still in an embryonic stage, characterized by low activity and hardly influenced by a few institutional investors. The exclusion of Credicorp from the FTSE Emerging Markets index is symptomatic.

There are some significant efforts of developing the MAV (capital market for mid-size companies with less than S/. 350MM of annual revenue), but the results are modest, with just 13 listed companies since its inception in 2013.

In this context, the recent creation of FIRBIs and FIBRAs, vehicles that have similarities with the American REITs, could represent a great opportunity to attract retail investors and increase the activity and liquidity of the capital market.

TTR: How difficult is it for corporates to access financing from local financial institutions in the current environment? What are the main barriers? How is financing structured?

EP: We have experienced a significant evolution in the volume of Peruvian companies accessing to the banking system in the past few years, going from 25% in 2014 to 40% in 2018, according to ASBANC.

The big challenge is the inclusion of the majority of small and medium enterprises that currently have very few options. The fintech market represents a very interesting alternative for this type of businesses, particularly in the way of factoring platforms.

Also, the increasing presence of foreign debt funds, especially Chilean, are becoming key participants, even in the small-and-mid size market. For example, recently we helped our client Llaxta Inmobiliaria y Constructora to obtain a US$ 10.5MM loan from Volcom Capital Chile for a real estate project in Piura, part of the social program “Techo Propio”.

TTR: Finally, we would like you to share with us your opinions and forecasts about the opening of the Peruvian market with other countries

EP: The Peru market presents many opportunities for all types of international investors, from strategic regional players to family offices and private equity and debt funds.

Beyond the usual M&A activity in the mining sector, we see interesting opportunities of consolidation in the agricultural business. For example, there is the case of Hortifrut that became the leading berry producer in the world after the acquisition of El Rocío. Likewise, last year we had the opportunity to advise the British trader Wealmoor and Limones Piuranos in the acquisition of the mango and avocado´s exporter Sunshine. Also, recently we led the sale of the mango´s exporter Dominus to the Peruvian-Danish joint venture Danper.

On the other hand, the real estate market still presents superiors return rates compared with other countries in Latin America, attracting global and regional real estate funds.

Finally, considering the current development of modern retail, we believe Peru represents an interesting possibility for regional companies dedicated to services related with cold chain and specialized storage.

Subscribe to our free newsletter:

This website uses cookies. By continuing to browse the site, you are agreeing to our use of cookies