TTR DealMaker Q&A with Ramón y Cajal Abogados Partner Amado Giménez Bono

Amado Giménez Bonois partner within the banking & finance department at Ramón y Cajal Abogados. His practice encompasses almost all aspects of finance transactions including debt restructuring and refinancing (over 100 deals) during his career, structured corporate finance, project finance (renewable energy, water, and infrastructure) LBOs and MBO´s. He regularly advises main Spain banks and financial institutions, as well as debt funds, advising also listed and unlisted companies/sponsors

TTR – In terms of company restructurings, what is the current situation and what are the prospects for the following months?

A.G.- It seems that the measures taken by Public Authorities in terms of elapsing insolvency periods is letting companies take time to evaluate their situation prior to making a decision as to filing for bankruptcy or a pre-insolvency scheme or not.

Despite such measures, there is still a number of companies struggling to survive that have more concerns than just the insolvency liability periods being suspended/extended, thus liquidity constraints derived from stopped activity and income are blocking their businesses. Liquidity introduced via State Guarantee schemes seem to have been useful but there is a general feeling that such measures are only a starting point of a long and tough journey.

We anticipate a very heavy work load for the upcoming months in terms of restructuring deals.

TTR – What type of companies has been more affected by COVID-19?

A.G.- Tourism (in a wide sense, hostelry, restoration, etc.), automotive components, and in general all sectors that depend on a physical presence for trade to produce, such as retail for instance.

TTR – How would you describe the measures taken by the Spanish Government to weather the business crisis caused by COVID-19? Do you think additional measures are needed?

A.G.- As described above, the measures taken so far seem to have given relief to the first wave, but a clear picture of the effects of the Covid-19 Pandemic seems yet to come; so it is difficult to evaluate the accuracy of such measures.

State Guarantee schemes have proven to be useful in a first stage (although its implementation in the beginning was not as smooth as desired), but increasing debt levels may not be a solution itself in the long run for businesses that have been literally closed for weeks.

Let´s see how political negotiations take place and how the EU bazooka is channeled into the Spanish economy/companies.

TTR – Regarding the M&A sector, do you think the health crisis has generated business opportunities? Which sectors do you think are more interesting for financially strong investors?

A.G.- It seems that the green energy industry is going to take an important role in the post-pandemic Spanish M&A scheme, but I guess not the only one. It will depend, at a first stage, whom will be the first one in put price to certain assets.

Informe Mensal Brasil – Julho 2020

Posted on

Fusões e aquisições no Brasil têm redução de 21%, até julho

Investimentos em startups de tecnologia aumentam 29% em 2020

Investimentos em startups de saúde e higiene crescem 214% em 2020

Fundos de Private Equity e Venture Capital estrangeiros reduzem seus investimentos em 54%

Patrocinado pelo:

O mercado transacional brasileiro registrou até o mês de julho 646 transações com um valor total de BRL 84,5bi, segundo o informe mensal do TTR – Transactional Track Record. Isto representa uma diminuição de 47% do valor movimentado e uma redução de 21% no número de transações, em relação ao mesmo período de 2019.

Por sua vez, no mês de julho se registraram 104 transações de fusões e aquisições entre anunciadas e concluídas, por um valor total de BRL 28,7bi.

Os setor mais ativo do ano é o de Tecnologia com 182 transações até o fim de julho. Seguido pelo setor Financeiro e de Seguros com 86 operações e em terceiro lugar, o setor Imobiliário com 71 transações.

Âmbito Cross-Border

Os Estados Unidos reduziram suas aquisições no Brasil em 19%, mesmo assim, ainda são o investidor mais ativo com 55 transações até o fim de julho. Fundos de Private Equity e Venture Capital estrangeiros também reduziram seus investimentos no Brasil em 54%. Da mesma forma, empresas estrangeiras diminuíram em 17% seus investimentos no setor de Tecnologia e Internet no Brasil, na comparação anual.

Em relação a atuação brasileira no exterior, Estados Unidos é o destino favorito na hora de realizar investimentos, com dez transações até o fim de julho. O segundo lugar onde o Brasil investiu mais esse ano é a Colômbia com quatro transações.

Private Equity

Até julho, os fundos de Private Equity registraram BRL 1,9bi no valor transacionado, o que representa uma redução de 86% na comparação anual. O número de transações foi 45, diminuição de 21%.

Venture Capital

Os fundos de Venture Capital movimentaram um total de BRL 3,8bi até julho, diminuição de 38% em relação a 2019. Já as transações foram 162, representando um aumento de 17%. O setor que mais movimentou foi o de Tecnologia com 101 transações, aumento de 29% na comparação anual. Outro setor que teve um grande salto foi o de Saúde e Higiene, com 22 transações, crescimento de 214% na comparação anual.

A operação do setor de energia movimentou BRL 1bi. A transação contou com a assessoria em lei brasileira dos escritórios Tauil & Chequer Advogados Associado a Mayer Brown, do Stocche Forbes Advogados e do escritório Machado, Meyer, Sendacz e Opice Advogados.

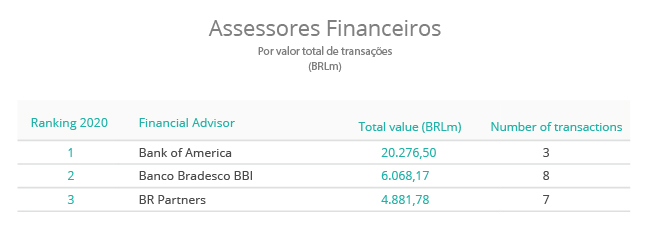

Ranking de assessores Jurídicos e Financeiros

Informe Mensal Portugal – Julho 2020

Posted on

Volume de fusões e aquisições encolhe 30% até julho

Estados Unidos reduziram suas aquisições em Portugal em 61%.

Volume de investimentos de Venture Capital sofre redução de 24%

Espanha continua sendo o país que mais investe em Portugal, com 19 transações

Patrocinado pelo:

O mercado transacional português registou até o mês de julho 182 transações com um valor total de EUR 10bi, segundo o relatório mensal do TTR -Transactional Track Record, o que representa um aumento de 50% do valor movimentado e uma redução de 30% no volume de negócios, em relação ao mesmo período de 2019.

Por sua vez, no mês de julho se registou um movimento de EUR 2,7bi e um volume de 18 transações de fusões e aquisições entre anunciadas e concluídas. Este aumento em relação ao número de transações de junho representa um rompimento, após uma redução consecutiva no número de operações mensal que vinha acontecendo desde fevereiro.

O setor mais ativo do ano é o Imobiliário com 51 transações até o fim de julho, aumento de 2% na comparação anual. Segue o setor de Tecnologia com 23 operações, redução de 47% em relação ao mesmo período de 2019.

Âmbito Cross-Border

Até o fim de julho, os Estados Unidos reduziram suas aquisições em Portugal em 61%. Fundos de Private Equity e Venture Capital estrangeiros também reduziram seus investimentos em Portugal em 67%. Da mesma forma, empresas estrangeiras diminuíram em 17% seus investimentos no setor de Tecnologia e Internet em Portugal, na comparação anual.

A Espanha continua sendo o país que mais investe em Portugal, com 19 transações até o fim de julho. Neste ano, França está na segunda colocação com 11 operações e Estados Unidos no terceiro lugar com nove transações. Igualmente, Espanha é o destino favorito de Portugal na hora de investir, com nove operações até o fim de julho.

Private Equity

Até julho, os fundos de Private Equity registraram EUR 1,9bi no valor transacionado, o que representa um aumento de 20% na comparação anual. Foram dez transações, diminuição de 67%.

Venture Capital

Os fundos de Venture Capital movimentaram um total de EUR 254m até julho, aumento de 52% em relação a 2019. Já as transações foram 32, representando uma redução de 24%. O setor que mais movimentou foi o de Tecnologia com 15 transações, diminuição de 44% na comparação anual. O segundo setor mais ativo foi o de Internet, com sete transações, crescimento de 17% na comparação anual.

El mercado transaccional español registra 1.080 operaciones hasta julio de 2020

En julio se han registrado 186 operaciones y un capital movilizado de EUR 7.796m

El sector Inmobiliario es el más activo del año, con 249 transacciones

En el año se registran 81 operaciones de Private Equity y 246 de Venture Capital

Patrocinado por:

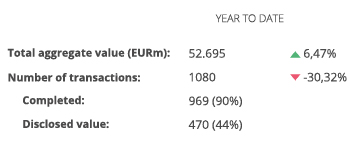

El mercado transaccional español ha registrado hasta el mes de julio un total de 1.080 operaciones con un importe agregado de EUR 52.695m, según el informe mensual de TTR , con el patrocinio de Drooms Cloud España.

Estas cifras suponen una disminución del 30,32% en el número de operaciones con respecto al mismo periodo de 2019, así como un aumento del 6,47% en el capital movilizado, debido principalmente al acuerdo de combinación de los negocios de Telefónica y Liberty en Reino Unido, operación valorada en aproximadamente EUR 22.600m.

Por su parte, en el mes de julio se han contabilizado 186 fusiones y adquisiciones, entre anunciadas y cerradas, por un importe agregado de EUR 7.796m.

En términos sectoriales, el sector Inmobiliario ha sido el más activo del año, con un total de 249 transacciones, seguido por el de Tecnología, con 189.

Ámbito Cross-Border

Por lo que respecta al mercado Cross-Border, hasta julio de 2020 las empresas españolas han elegido como principales destinos de inversión a Portugal y a Estados Unidos, con 19 y 12 operaciones, respectivamente. En términos de importe, Reino Unido es el país más destacado, con un valor aproximado de EUR 23.202,06m.

Por otro lado, Estados Unidos y Reino Unido, con 70 y 62 operaciones, respectivamente, son los países que mayor número de inversiones han realizado en España. Por importe destaca Estados Unidos, con un importe de EUR 5.288,50m.

Private Equity, Venture Capital y Asset Acquisitions

En lo que va de año se ha contabilizado un total de 81 operaciones de Private Equitypor EUR 6.318m, lo cual supone un descenso del 50,61% en el número de operaciones y del 71,08% en el importe de las mismas, respecto al mismo periodo del año anterior.

Por su parte, en el mercado de Venture Capitalse han llevado a cabo 246 transacciones con un importe agregado de EUR 3.555m, lo que implica una reducción del 16,04% en el número de operaciones y un aumento del 158,14% en el importe de las mismas, en términos interanuales.

En el segmento de Asset Acquisitions, hasta julio se han registrado 331 operaciones por un valor de EUR 9.185m, lo cual representa una disminución del 30,75% en el número de operaciones, y un descenso del 15,84% en el importe de éstas, en términos interanuales.

La operación, que ha registrado un importe de EUR 445m, ha estado asesorada por la parte legal por Bird & Bird España y por Linklaters Spain.

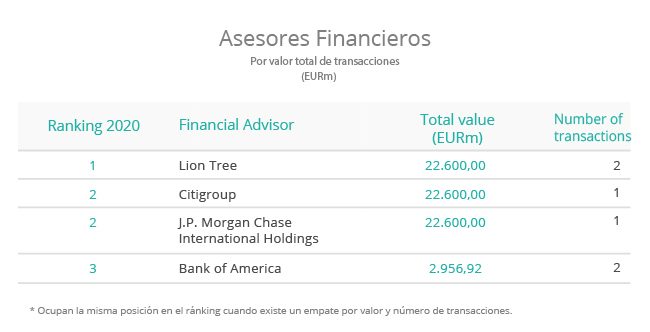

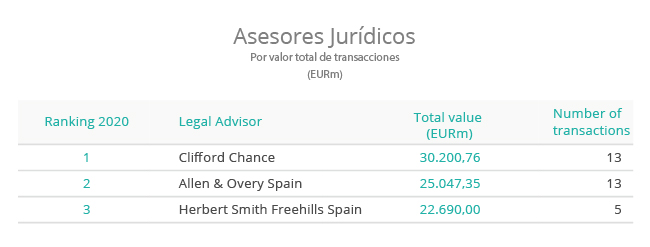

Ranking de asesores financieros y jurídicos

Transactional Impact Monitor: Spain & Portugal – Vol. 4

Posted on

Transactional Impact Monitor: Spain & Portugal – Vol. 4

31 July 2020

TTR’s Transactional Impact Monitor (TIM) is a Special Report combining local knowledge and market visibility from top dealmakers developed to address extraordinary situations affecting the macroeconomic stability and M&A outlook in core markets

Sponsored by:

INDEX

SPAIN – M&A Outlook – Capital Markets – Private Equity – Handling the Crisis

PORTUGAL – M&A Outlook – Private Equity – Handling the Crisis

– Dealmaker Profiles

SPAIN

On the cusp of Spain’s summer holiday season, the country confronts the reality that its fight against SARS-CoV-19 may be far from over. The streets of Madrid are once again full of pedestrians, who are now required to wear masks in public, as reported cases surge to levels not seen since the beginning of May. New infections are being reported mainly among younger Spaniards, however, and haven’t resulted in the same level of hospitalizations, according to the local press.

The official death toll attributed to the novel corona virus stands just shy of 45,000, while in any given year, there are nearly 500,000 deaths overall in the country. Spain’s death rate has trended upwards over the past 10 years as the country’s population ages, with both cancer and circulatory system diseases each blamed for more than 100,000 deaths annually.

Nearly half of Spain’s autonomous communities are some semblance of normal, while the other half are considered high- or medium-risk by the authorities. Those who can work remotely, continue to do so across much of the country.

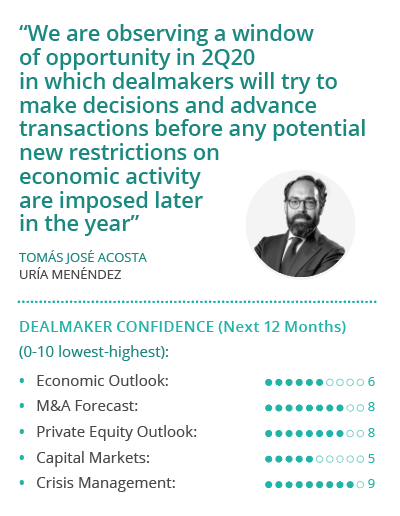

Dealmakers in the transactional market have remained incredibly busy, and the pipeline is looking robust for 2H20, sources told TTR. The workload for legal advisor Uría Menéndez has been surprisingly heavy, given the low expectations earlier in the year, despite the poor visibility about what will happen in the coming months, Partner Tomás Acosta told TTR.

Projections by the International Monetary Fund indicate a fall in global GDP of between 3% and 5%, while the Bank of Spain projects a 15% contraction in Spain, Acosta noted, but these figures too are in flux, making it difficult to predict what will happen by the close of the year.

“What I do see, and this will be key, is the need for government authorities to react decisively to avoid any major resurgence,” Acosta said, noting the new outbreaks seemed to be under control, even as reported cases escalate once again.

“We are observing a window of opportunity in 2H20 in which dealmakers will try to make decisions and advance transactions before any potential new restrictions on economic activity are imposed later in the year,” Acosta added.

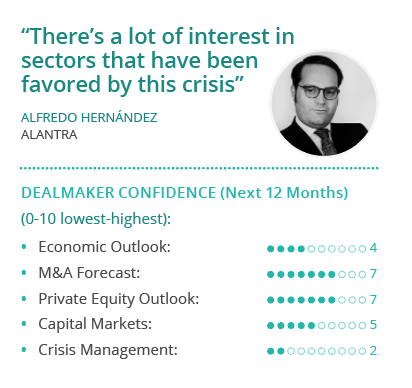

It won’t be until September or October that reality will set in, said Alantra Partner Alfredo Hernández, when companies will have three quarters of results to analyze. There will be a window between October and November to close deals, but the real boom will be in 1Q21, said Hernández. Alantra’s deal pipeline is stronger than it was at this point in 2019, Hernández said, but the type of deals has changed from overwhelmingly M&A-related to roughly half M&A and half financing transactions, he said.

When speaking with CEOs and CFOs, they are primarily concerned about their 2020 results, Hernández said. “The reality is that they still don’t know what the impact will be, though for those in the transportation and hospitality industries, the repercussions have been profound, and the impact is exceedingly clear,” he said.

There are already clear winners too, Hernández noted, citing the healthcare industry, certain consumer product segments and food production and distribution, which haven’t merely been resilient, they’ve growth by 20% to 30%. “All this has been made possible thanks to technology and communications, which have helped accelerate the existing trend of digitalization. “

Traditional retail, on the other hand, which was already suffering as e-commerce took at growing piece of the market, has been dealt a severe blow, Hernández noted. An acceleration of the migration online and away from brick and mortar among major retailers is a clear outcome of the current crisis, he said.

Portugal has registered a much lower toll from SARS-CoV-19 than its Iberian neighbor, with some 50,613 confirmed cases and 1,725 deaths attributed to the novel coronavirus. This hasn’t allowed the country to escape the devastating economic impacts associated with the pandemic threat, however, and the prospects for the economy are grim as the country enters peak summer holiday season, dealmakers told TTR.

“I am pessimistic about the economic outlook for Portugal,” said SLCM Managing Partner Luís Miguel Cortes Martins. “We are already seeing empty hotels; high-end restaurants also with very few clients. Many of them in fact reopened and then had to close again; that will generate a lot of unemployment and it will have a sharp impact on demand.”

The estimates for the Portuguese economy are not at all positive, Cortes Martins noted, and that will, in turn, drive away foreign investment. “I don’t see a V-shape recovery for the Portuguese economy,” he said.

“If Spain has a quick recovery, Portugal will be better off, since they are our main commercial partner,” he noted, and Portugal is also subject to the form the recovery will take across Europe, generally, especially in Germany. “Tourism is a main driver in our economy, and no one really knows when that will recover,” he said.

“I am somewhat pessimistic with regard to the economic outlook for 2021,” agreed EY Partner, Strategy and Transactions Miguel Farinha. “The pandemic’s economic impact will be greater than what most institutions, such as the IMF and the Bank of Portugal, are forecasting,” he cautioned. “Portugal will take a heavy blow, one which I think most people are not yet estimating correctly,” he said.

Portugal’s economy grew substantially in recent years, mostly thanks to its booming tourism sector, Farinha pointed out. Tourism typically represents about 15% of GDP in direct contributions and well over 20% including indirect contributions. The sudden flat line will bring severe economic hardship, he said.

Until a vaccine or some kind of treatment is made available, the downturn will persist, Farinha added. Notwithstanding his gloomy macroeconomic forecast, Farinha said the transactional market will be very strong, with a lot of very good acquisitions.