Transactional Impact Monitor: Spain & Portugal – Vol. 4

31 July 2020

TTR’s Transactional Impact Monitor (TIM) is a Special Report combining local knowledge and market visibility from top dealmakers developed to address extraordinary situations affecting the macroeconomic stability and M&A outlook in core markets

Sponsored by:

INDEX

SPAIN

– M&A Outlook

– Capital Markets

– Private Equity

– Handling the Crisis

PORTUGAL

– M&A Outlook

– Private Equity

– Handling the Crisis

– Dealmaker Profiles

SPAIN

On the cusp of Spain’s summer holiday season, the country confronts the reality that its fight against SARS-CoV-19 may be far from over. The streets of Madrid are once again full of pedestrians, who are now required to wear masks in public, as reported cases surge to levels not seen since the beginning of May. New infections are being reported mainly among younger Spaniards, however, and haven’t resulted in the same level of hospitalizations, according to the local press.

The official death toll attributed to the novel corona virus stands just shy of 45,000, while in any given year, there are nearly 500,000 deaths overall in the country. Spain’s death rate has trended upwards over the past 10 years as the country’s population ages, with both cancer and circulatory system diseases each blamed for more than 100,000 deaths annually.

Nearly half of Spain’s autonomous communities are some semblance of normal, while the other half are considered high- or medium-risk by the authorities. Those who can work remotely, continue to do so across much of the country.

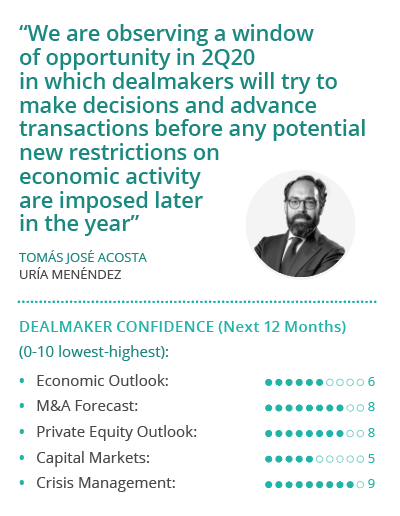

Dealmakers in the transactional market have remained incredibly busy, and the pipeline is looking robust for 2H20, sources told TTR. The workload for legal advisor Uría Menéndez has been surprisingly heavy, given the low expectations earlier in the year, despite the poor visibility about what will happen in the coming months, Partner Tomás Acosta told TTR.

Projections by the International Monetary Fund indicate a fall in global GDP of between 3% and 5%, while the Bank of Spain projects a 15% contraction in Spain, Acosta noted, but these figures too are in flux, making it difficult to predict what will happen by the close of the year.

“What I do see, and this will be key, is the need for government authorities to react decisively to avoid any major resurgence,” Acosta said, noting the new outbreaks seemed to be under control, even as reported cases escalate once again.

“We are observing a window of opportunity in 2H20 in which dealmakers will try to make decisions and advance transactions before any potential new restrictions on economic activity are imposed later in the year,” Acosta added.

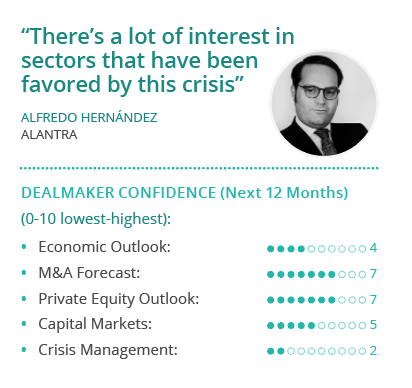

It won’t be until September or October that reality will set in, said Alantra Partner Alfredo Hernández, when companies will have three quarters of results to analyze. There will be a window between October and November to close deals, but the real boom will be in 1Q21, said Hernández. Alantra’s deal pipeline is stronger than it was at this point in 2019, Hernández said, but the type of deals has changed from overwhelmingly M&A-related to roughly half M&A and half financing transactions, he said.

When speaking with CEOs and CFOs, they are primarily concerned about their 2020 results, Hernández said. “The reality is that they still don’t know what the impact will be, though for those in the transportation and hospitality industries, the repercussions have been profound, and the impact is exceedingly clear,” he said.

There are already clear winners too, Hernández noted, citing the healthcare industry, certain consumer product segments and food production and distribution, which haven’t merely been resilient, they’ve growth by 20% to 30%. “All this has been made possible thanks to technology and communications, which have helped accelerate the existing trend of digitalization. “

Traditional retail, on the other hand, which was already suffering as e-commerce took at growing piece of the market, has been dealt a severe blow, Hernández noted. An acceleration of the migration online and away from brick and mortar among major retailers is a clear outcome of the current crisis, he said.

M&A Outlook

… Click here to access the fourth issue of Transactional Impact Monitor: Spain & Portugal – Vol. 4.

PORTUGAL

Portugal has registered a much lower toll from SARS-CoV-19 than its Iberian neighbor, with some 50,613 confirmed cases and 1,725 deaths attributed to the novel coronavirus. This hasn’t allowed the country to escape the devastating economic impacts associated with the pandemic threat, however, and the prospects for the economy are grim as the country enters peak summer holiday season, dealmakers told TTR.

“I am pessimistic about the economic outlook for Portugal,” said SLCM Managing Partner Luís Miguel Cortes Martins. “We are already seeing empty hotels; high-end restaurants also with very few clients. Many of them in fact reopened and then had to close again; that will generate a lot of unemployment and it will have a sharp impact on demand.”

The estimates for the Portuguese economy are not at all positive, Cortes Martins noted, and that will, in turn, drive away foreign investment. “I don’t see a V-shape recovery for the Portuguese economy,” he said.

“If Spain has a quick recovery, Portugal will be better off, since they are our main commercial partner,” he noted, and Portugal is also subject to the form the recovery will take across Europe, generally, especially in Germany. “Tourism is a main driver in our economy, and no one really knows when that will recover,” he said.

“I am somewhat pessimistic with regard to the economic outlook for 2021,” agreed EY Partner, Strategy and Transactions Miguel Farinha. “The pandemic’s economic impact will be greater than what most institutions, such as the IMF and the Bank of Portugal, are forecasting,” he cautioned. “Portugal will take a heavy blow, one which I think most people are not yet estimating correctly,” he said.

Portugal’s economy grew substantially in recent years, mostly thanks to its booming tourism sector, Farinha pointed out. Tourism typically represents about 15% of GDP in direct contributions and well over 20% including indirect contributions. The sudden flat line will bring severe economic hardship, he said.

Until a vaccine or some kind of treatment is made available, the downturn will persist, Farinha added. Notwithstanding his gloomy macroeconomic forecast, Farinha said the transactional market will be very strong, with a lot of very good acquisitions.

M&A Outlook

… Click here to access the fourth issue of Transactional Impact Monitor: Spain & Portugal – Vol. 4.