Transactional Impact Monitor: Andean Region – Vol. 2

9 June 2020

TTR’s Transactional Impact Monitor (TIM) is a Special Report combining local knowledge and market visibility from top dealmakers developed to address extraordinary situations affecting the macroeconomic stability and M&A outlook in core markets

INDEX

CHILE

– M&A Outlook

– Handling the Crisis

COLOMBIA

– M&A Outlook

– Handling the Crisis

PERU

– M&A Outlook

– Handling the Crisis

– The View from Milan

– Dealmaker Profiles

CHILE

Nearly a month after Chile tightened the initial restrictions on movement and business activities imposed in mid-March in Santiago, the minister of health announced on 2 June revised figures for the number of active cases under treatment for SARS-CoV-2, resulting in a decrease from 59,100 to 21,325 and an increase in reported recoveries from some 46,000 to just under 86,000. At the same time, health officials announced the deadliest day with 75 deaths attributed to the virus, bringing the total official death toll to just over 1,200 and 114,000 confirmed cases.

The country avoided a total lockdown from the outset by isolating specific districts with tight quarantines based on an aggressive testing program. This strategy allowed much economic activity to carry on uninterrupted, noted DLA Piper Partner Paulo Larrain.

Notwithstanding, there are industries that have been severely affected, Larrain said. “It’s a very bloody process for many.”

The country was still reeling from the social disruption in October 2019, when protests took over the capital calling for a greater focus on programs geared towards reducing persistent income inequality. “These demands are still pending,” Larrain said, noting the plebiscite on social and constitutional reforms has been relegated to October.

M&A Outlook

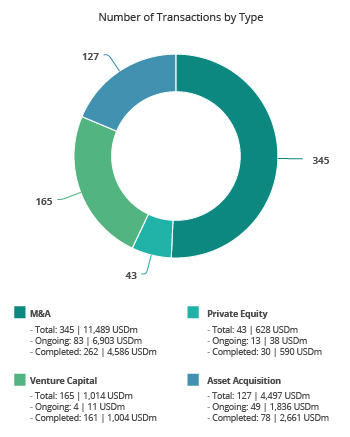

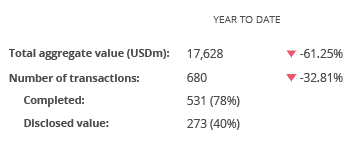

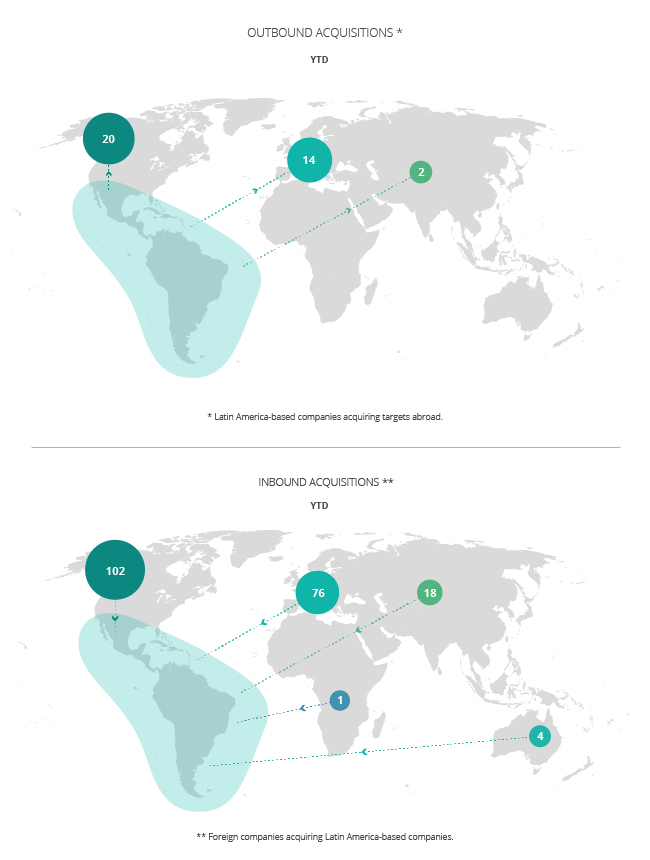

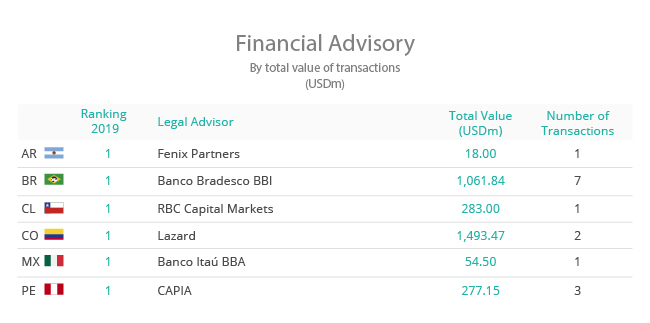

… Click here to access the third issue of Transactional Impact Monitor: Andean Region – Vol. 2

COLOMBIA

As May came to a close, hope for a swift return to a normal life was dashed for Colombians as President Iván Duque extended the period of mandatory self-quarantine through the end of June, while extending the public health emergency through to the end of August. The official death toll in the country attributed to Covid-19 stands at just over 1,000 with some 33,000 confirmed cases.

Under Colombia’s new phase of restrictions imposed to face the SARS-CoV-2 threat, 43 exceptions were granted permitting the reopening of several non-essential businesses, including museums, libraries, malls and hair salons, while limiting those venues to 30% occupancy. Residents of Bogotá remain confined to their homes until 15 June.

The rosy prospects of 3.7% GDP growth projected at the beginning of 2020 have long since faded, replaced by apprehension over the health threat, and increasingly, an economic recession likely to persist for the next several years, Inverlink Managing Partner Mauricio Saldarriaga told TTR.

“It’s a call to a simpler life,” said Saldarriaga. Inverlink presciently began implementing an internationalization in 2015, joining global boutique investment bank network IMAP and establishing its own footprint across the region. The move paid off, Saldarriaga said, noting the firm grew through several tough years, including 2018, when the presidential election featured a leftist candidate and many investments in the country were put on hold.

Despite Iván Duque’s victory, the following year was much slower than most thought it should be, Saldarriaga said. “People thought that within two months, things would be flying.” When the country finally turned the corner in early 2020 with a robust start to the year such as hadn’t been seen in a long time, with real estate and financial services deals booming, “the little meteor” of SARS-CoV-2 hit, he noted, and the situation changed entirely; many deals were put on hold, frozen. “Some will die, others are in the process of being reactivated, but everybody went into survival mode, to preserve cash.” In general, companies began to focus on reducing costs, “trimming the fat”, Saldarriaga said.

“Many companies will face difficulties, even those with healthy balance sheets,” he said. Restaurants, hotels, retailers, all commerce has been hit hard, and there are few winners, Saldarriaga said, namely personal care products, household cleaning products and food retail. “That’s about 10% of companies. Then there’s the 60% that have been heavily affected, and the rest that will have difficulty surviving.”

Colombia will now enter a period of repositioning and restructuring, Saldarriaga said. “We’re in discussions with a lot of providers of capital and getting started with the airlines, construction companies and industrial entities, which were already suffering. This was the final straw. We all know this is temporary, but with an undetermined duration, it’s very difficult to make plans.”

The crisis will cause great difficulty in Colombia and across Latin America over the next 24-to-36 months, he said, noting the region will face a slower recovery owing to the heavy dependence on commodities. “These economies are facing a huge setback, with an enormous impact on the middle class and on spending power. This will be a marathon, not a sprint. Resilience and survival is the name of the game.”

Colombia’s ambitious 4G program designed to develop the country’s airports, seaports, highways and social infrastructure, was already enduring growing pains Saldarriaga attributed to trying to go “from crawling to running from one day to the next”. The government’s capacity to keep these projects on track and make them a countercyclical engine of growth following this crisis is challenging in the context of the country’s fiscal issues, he said.

“Infrastructure has become a great lesson in all of this,” he said. The sector was seen as low risk, with low transaction costs, but the these assets are facing a grave impact as tolls evaporate along with traffic through airports, both previously considered predictably stable. It may be a hiccup, Saldarriaga said, and traffic will surely recover, but in the short term, the sector faces a liquidity crunch. “The materialization of risks in the sector will lead to much negotiation with the National Infrastructure Agency (ANI) and a lot of litigation, reclamations and negotiations between the government and concession holders as they hash out how to assign risks in the context force majeure, he said.

“This will be an opportunity for Canadian infrastructure funds, the Brookfields of the world, to recycle capital and keep companies afloat,” Saldarriaga said. Pension funds that have liquidity now can also benefit from the tight situation over the next six-to-12 months in which there will undoubtedly be a lot of distressed M&A and assets that change hands by necessity, he added. “Institutional investors are watching to see how this will play out.”

Colombia’s dependence on oil revenue, which represents nearly 50% of the federal budget, has led to a simultaneous shock that amplifies the economic shock brought about by restrictions imposed to contain the spread of SARS-CoV-2, Saldarriaga noted. The oil market is distorted and manipulated, and this dependence will make the recovery more difficult, Saldarriaga said. “It obligates us to seek ways to depend less on raw materials and more on value-added products,” he said. The falling value of the Colombian peso makes labor costs and many products more competitive, Saldarriaga added. “These are countries that don’t just need to bounce back, they need to reinvent themselves and bounce back, and we better do it, because oil is surely not a stable bet for the future.”

Diversifying its revenues beyond oil is an important goal for Colombia, but it’s rightly a medium-term project, Saldarriaga said, given the country is still heavily dependent on extractive resources to improve the standard of living for its citizens. “If we have natural resource wealth, we need to develop it. In the end, it’s what can bring us all prosperity.” The important contribution of hydropower powering Colombia’s electric grid makes the country unique, Saldarriaga pointed out, and balances out to an extent the dependence on oil for fiscal revenue. While the country has indeed put a growing emphasis on renewable energy development in recent years, incentivizing wind and solar, the debate underway in the US and the EU in which proponents are calling for de-carbonization as an engine of growth out of recession is more a first world dilemma at present, he said.

M&A Outlook

… Click here to access the third issue of Transactional Impact Monitor: Andean Region – Vol. 2

PERU

On 3 June, the government of Peru extended the country’s health emergency for another three months in the face of the highest death toll in the Andean Region attributed to SARS-CoV-2. The official toll stood at nearly 5,000 with more than 178,000 reported cases. The extension of the declared health emergency is in addition to the state of emergency in place until 30 June.

Peru was among the first countries in the region to implement strict health protocols, ground air travel and impose quarantines and curfews, noted APOYO Finanzas Corporativas Partner Eduardo Campos, “but we were already in a precarious situation”.

M&A Outlook

… Click here to access the third issue of Transactional Impact Monitor: Andean Region – Vol. 2

The View from Milan

The Special Report has sections on M&A, Private Equity and Handling the Crisis, as well as a first-hand account from Italy in The View From Milan, featuring EY Italy Managing Partner Tax & Law and Mediterranean Region Accounts Leader Stefania Radoccia.

Transactional Impact Monitor: Andean Region – Vol. 2