Mercado de Fusiones y Adquisiciones en Argentina registra 34 operaciones en el primer trimestre de 2019

12 operaciones registradas en el primer trimestre alcanzan un importe de USD 1.284m

Sector Alimentario es el más destacado del periodo, con 7 operaciones

El mercado de M&A en Argentina ha contabilizado en los tres primeros meses del año un total de 34 operaciones, de las cuales 12 suman un importe no confidencial de USD 1.284m, de acuerdo con el informe trimestral de Transactional Track Record. Estos datos reflejan un descenso del 42,37% en el número de operaciones y una baja del 9,54% en el importe de las mismas, respecto al primer trimestre de 2018.

De las operaciones contabilizadas de enero a marzo, el 2,94% pertenece a operaciones menores a USD 1m, el 2,94% pertenece a operaciones entre USD 1m y USD 10m; el 23,53% pertenece a operaciones entre USD 10m a USD 50m; el 2,94% pertenece a operaciones entre USD 100m y USD 500m; y el 2,94% pertenece a operaciones mayores a USD 500m.

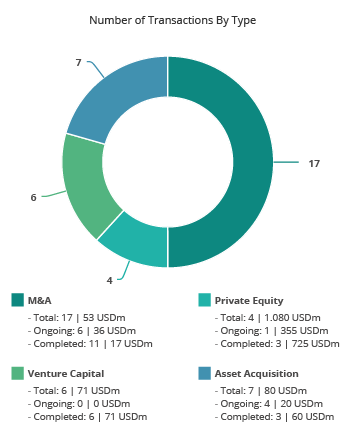

En términos sectoriales, el Alimentario es el que más transacciones ha contabilizado a lo largo de 2019, con un total de 7 operaciones, seguido por el de Petróleo y Gas, con 5 transacciones.

Ámbito Cross-Border

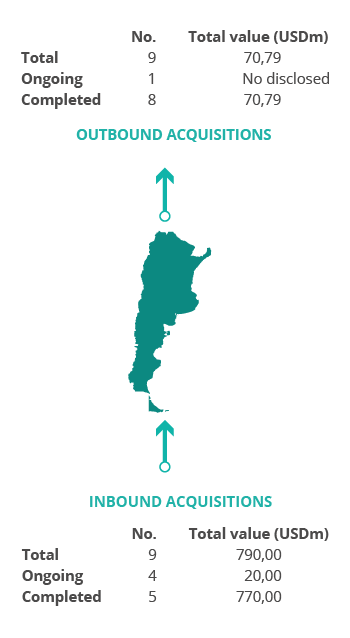

Por lo que respecta al mercado Cross-Border, en lo que va de año las empresas argentinas han apostado principalmente por invertir en Brasil y Uruguay, con 3 transacciones en cada país. Por importe, destaca Chile, con USD 30m.

Por otro lado, Estados Unidos, con 5 operaciones, es el país que más ha apostado por realizar adquisiciones en Argentina. Por importe destacan Estados Unidos y Países Bajos, con USD 725m por cada país.

PrivateEquity y Venture Capital

En el primer trimestre de 2019 se han producido un total de 4 transacciones de Private Equity valoradas en USD 1.080m, las cuales representan un alza del 100% en el número de operaciones y un aumento del 259% en el capital movilizado con respecto al primer trimestre de 2018.

Por su parte, en los tres primeros meses de 2019, Argentina ha registrado 6 operaciones de Venture Capital valoradas en USD 71m, lo que representa un descenso del 33,33% en el número de operaciones y un aumento del 150,05% en el capital movilizado con respecto al mismo periodo del año pasado.

La operación, que ha registrado un importe de USD 725m, ha estado asesorada por la parte legal por Baker McKenzie Argentina; Baker McKenzie US y Estudio Beccar Varela. Por la parte financiera la operación ha sido asesorada por BBVA Corporate & Investment Banking.

Ranking de asesores financieros y jurídicos

El informe publica los rankings de asesoramiento financiero y jurídico del mercado M&A argentino durante el primer trimestre de 2019, donde se informa de la actividad de las firmas destacadas por número de transacciones y por importe de las mismas.

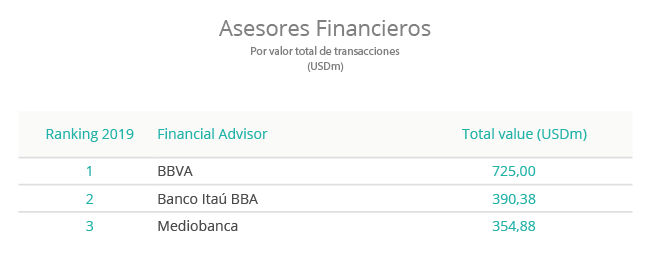

En el ranking TTR de asesores financieros, por importe, lideran en el primer trimestre de 2019 BBVA con USD 725m, y por número de operaciones, lidera Banco Itaú BBA, con 3 operaciones.

En el ranking argentino de asesores jurídicos en el segmento de Fusiones y Adquisiciones, Marval O’Farrell & Mairal, ha ocupado el primer lugar por número de transacciones, con 6 transacciones. Y por importe, han liderado Baker McKenzie Argentina y Estudio Beccar Varela, con USD 725m en cada firma.

Informe LatAm – 1Q19

Posted on

Mercado M&A de América Latina registra 446 operaciones en el primer trimestre de 2019

Chile, Colombia y México registran aumento del capital movilizadoen el transcurso de 2019

41dealsde Venture Capital registrados YTDalcanzan un importe de alrededor de USD 281m

El mercado transaccional de América Latina cierra los tres primeros meses del año con un total de 446 operaciones, de las cuales 173 tienen un importe no confidencial que suman aproximadamente USD 17.295m, según el más reciente informe de Transactional Track Record.

Estas cifras suponen una disminución del 18,01% en el número de operaciones y un descenso del 43,08% en el importe de las mismas, respecto al mismo periodo de 2018.

PrivateEquity y Venture Capital

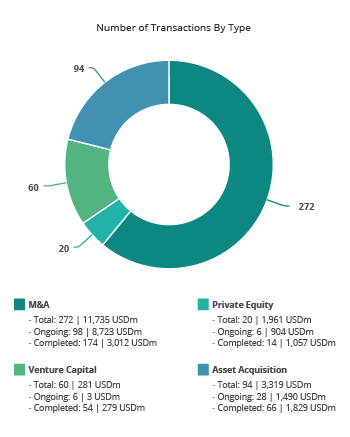

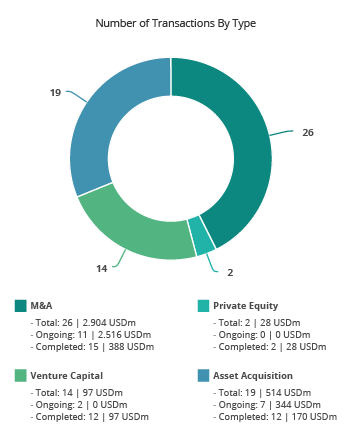

En el primer trimestre de 2019 se han contabilizado un total de 20 operaciones de PrivateEquity, de las cuales 9 transacciones tienen un importe no confidencial agregado de USD 1.961m. Esto supone una disminución del 50% en el número de operaciones y un descenso del 25,87% en el importe de estas con respecto al mismo periodo de 2018.

En cuanto al segmento de Venture Capital, a lo largo del año se han llevado a cabo 60 transacciones, de las cuales 41 operaciones tienen un importe no confidencial que suman alrededor de USD 281m, lo que supone un descenso del 31,82% en el número de transacciones y un descenso del 53,71% en el capital movilizado con respecto al primer trimestre del año pasado.

Ranking de operaciones por países

En el primer trimestre de 2019, por número de operaciones, Brasil lidera el ranking de países más activos de la región con 233 operaciones (disminución del 20%), y una baja del 59% en el capital movilizado en términos interanuales (USD 7.762m). Le sigue en el listado México, con 61 operaciones (baja del 38%), y con un descenso del 28% de su importe con respecto al mismo periodo del año pasado (USD 3.543m).

Por su parte, Chile sube en el ranking, con 57 operaciones (un aumento del 43%), y con un incremento del 162% en el capital movilizado (USD 2.128m). Colombia, por su parte, supera a Argentina en el ranking y registra 55 operaciones (aumento del 15%), con un descenso del 29% en capital movilizado (USD 972m).

Entre tanto, Argentina ha bajado en el ranking con un registro de 34 operaciones, lo cual representa un 42% menos, así como un descenso del 10% en su importe respecto al mismo periodo del año pasado (USD 1.284m). Perú, por su parte, ha registrado 28 operaciones (baja del 33%) y un descenso del 73% en su capital movilizado respecto al mismo periodo del año anterior (USD 806m).

Ámbito Cross-Border

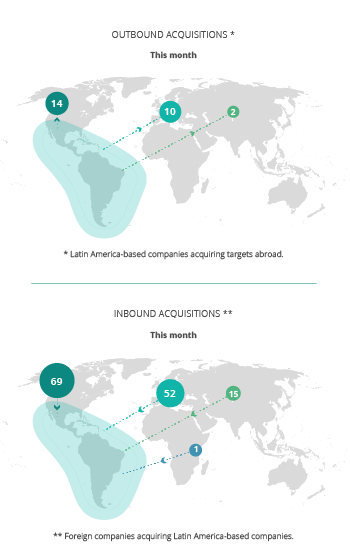

En el ámbito Cross-Border se destaca el apetito inversor de las compañías latinoamericanas en el exterior en el primer trimestre de 2019, especialmente en Norteamérica y Europa, donde se han llevado a cabo 14 y 10 operaciones, respectivamente. Por su parte, las compañías que más han realizado transacciones estratégicas en América Latina proceden de Norteamérica, con 69 operaciones, Europa (53), y Asia (15).

La transacción, valorada en USD 490m, ha estado asesorada por la parte legal por Philippi, Prietocarrizosa, Ferrero DU & Uría Perú; Posadas, Posadas & Vecino; Miranda & Amado Abogados y Ferrere. Por la parte financiera, la operación ha sido asesorada por BTG Pactual Perú; McKinsey & Company y PwC Perú. Por su parte, Llorente & Cuenca Perú ha sido asesor en el área de comunicaciones.

Ranking de asesores financieros y jurídicos

El informe publica los rankings de asesoramiento financiero y jurídico del primer trimestre de 2019 de operaciones de M&A, Private Equity, Venture Capital y Mercado de Capitales, donde se informa de la actividad de las firmas destacadas por número de transacciones y por importe de las mismas.

Informe México- 1Q19

Posted on

El importe de operaciones de Private Equity en México aumenta un 277% en el primer trimestre de 2019

En los tres primeros meses del año se han registrado 61 transacciones en el país

27operaciones registradas en el primer trimestre alcanzan un importe de USD 3.543m

El sector de Internet es el más destacado del periodo, con 13 operaciones

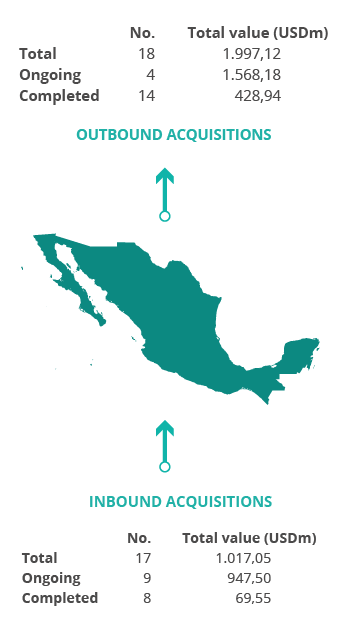

El mercado de M&A en México ha contabilizado en los tres primeros meses del año un total de 61 operaciones, de las cuales 27 suman un importe no confidencial de USD 3.543m, de acuerdo con el informe trimestral de Transactional Track Record. Estos datos reflejan un descenso del 37,76% en el número de operaciones y del 27,82% en el importe de las mismas con respecto al primer trimestre de 2018.

De las operaciones contabilizadas de enero a marzo, el 0,97% pertenece a operaciones entre USD 1m y USD 10m; el 3,68% pertenece a operaciones entre USD 10m a USD 50m; el 9,86% pertenece a operaciones entre USD 100m y USD 500m; y el 48,15% pertenece a operaciones mayores a USD 500m.

En términos sectoriales, el sector de Internet es el que más transacciones ha contabilizado a lo largo de 2017, con un total de 13 operaciones, seguido por el de Tecnología con 9, además del Financiero y de Seguros, con 8 operaciones.

Ámbito Cross-Border

Por lo que respecta al mercado Cross-Border, en lo que va de año las empresas mexicanas han apostado principalmente por invertir en Estados Unidos y España, con 3 transacciones en cada país. Por importe, destaca Brasil, con USD 912,13m.

Por otro lado, Estados Unidos es el país que más ha apostado por realizar adquisiciones en México, con 6 operaciones. Por importe destaca Reino Unido, con USD 808,40m.

PrivateEquity y Venture Capital

En el primer trimestre de 2019 se han producido un total de 2 transacciones de Private Equity valoradas en USD 28m, las cuales representan una disminución del 83,33% en el número de operaciones y un aumento del 277,35% en el capital movilizado con respecto al primer trimestre de 2018.

Por su parte, en los tres primeros meses de 2019, México ha registrado 14 operaciones de Venture Capital valoradas en USD 97m, lo que representa un descenso del 36,36% en el número de operaciones y una disminución del 45,04% en el capital movilizado con respecto al mismo periodo del año pasado.

AssetAcquisitions

En el mercado de adquisición de activos, se han cerrado en el primer trimestre 19 transacciones con un importe de USD 514m, lo cual implica un aumento del 5,56% en el número de operaciones y un descenso del 64,66% en su importe con respecto al mismo periodo de 2018.

La operación ha estado asesorada por la parte legal por Mijares, Angoitia, Cortés y Fuentes; Creel, García-Cuéllar, Aiza y Enríquez y por Ramírez, Gutiérrez-Azpe, Rodríguez-Rivero y Hurtado. En cuanto a la parte financiera, la operación ha sido asesorada por Inverlink y por UBS Bank México.

Ranking de Asesores Legales y Financieros

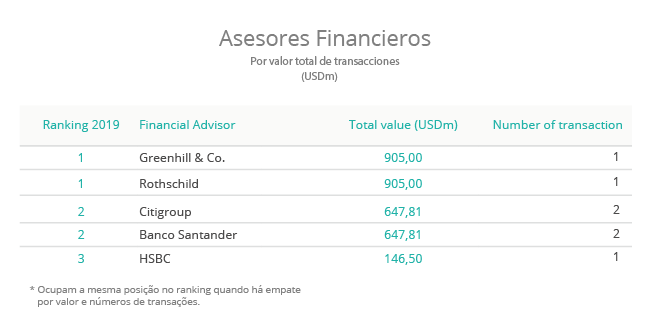

En el ranking TTR de asesores financieros, por importe, lideran en enero de 2019 Greenhill & Co, con USD 905y, por número de operaciones, lidera Citigroup, con dos operaciones.

En cuanto al ranking de asesores jurídicos, por importe y por número de operaciones, lideran las firmas Galicia Abogados y Mijares, Angoitia, Cortés y Fuentes, con importes de USD 801m y dos transacciones en cada firma.

DealMaker Q&A

Posted on

TTR DealMaker Q&A with Pérez Alati Grondona Benites & Arntsen Partner Eugenio Aramburu

Deal Summary:

On 2 November, PeCom Servicios Energía, a subsidiary of Argentine conglomerate Pérez Companc Family Group, closed the acquisition of pump and petrochemicals manufacturer Bolland y Cia. for ARS 1.5bn (USD 126.3m). The transaction was selected by TTR as Deal of the Quarter in Argentina for 4Q18. The deal follows the USD 98m acquisition of PeCom Servicios Energía in 2015 by the family-owned holding, marking the group’s reentry into the oil and gas business and the subsequent acquisition of Tel3 closed in August. The group had previously exited its energy holdings with the USD 1.1bn sale of Petrolera Pérez Companc to Petrobras in 2002.

EA: We’ve been working with the Pérez Companc

Family Group for a little more than a year-and-a-half. They knew of us through

a few other deals, including the sale of the family oil business to Petrobras

in 2002, when we represented the buyer. We also represented BRF when it bought

a number of brands from the family’s food business, Molinos Río de la Plata, in

2015. They had a chance to interact with us at the time and selected us because

we were one of the bigger firms in Argentina providing comprehensive legal

services and they liked how we worked.

TTR:

How did this deal come about?

EA: Pecom approached Bolland. Some

shareholders wanted to sell, some did not. Some were older and some had taken

equity in a recent management buy-out.

TTR:

Why was Pecom interested in expanding its holdings in Argentina’s oil and gas

industry?

EA: The Pérez Companc Family Group is

confident that the oil and gas industry is going to expand and they wanted to

expand into services they did not already offer to become a full-service

provider to the industry. Through this deal they can now offer integrated

solutions to all the operators throughout the oil and gas industry.

TTR:

Why was it a good time to invest full heartedly in this industry?

EA: Notwithstanding the international price

of oil, there is an absolute necessity from the standpoint of the Argentine

government to develop the Vaca Muerta reserves as it is one of the biggest

reserves of shale gas in the world. While development of these assets may be

slower because of international energy prices, Argentina is going to provide

incentives to develop this industry regardless. Argentina is currently

importing gas, from Venezuela and elsewhere, which will become unnecessary once

these reserves enter production. All these reasons motivated Pecom to have a bigger

presence in the gas industry.

TTR:

How did recent political and economic reforms in Argentina set the stage for

this deal?

EA: During the Kirchner administration you

would never have seen a transaction like this. The government had intervened in

oil and gas prices and investments in the industry were basically zero. These investments

that require a long term for amortization need a stable environment. When Macri

came to power, the situation changed drastically. The government set out to

stimulate investments in the energy market, which is where there have been more

transactions. This transaction couldn’t have happened before. This is a bet on

the part of the Perez Companc Group demonstrating confidence in the Argentine

government and the industry.

TTR:

What made this transaction challenging?

EA: Bolland had a lot of individual shareholders

and they didn’t all have the same interest in the sale, so it demanded a lot of

negotiations aligning all their different interests. Secondly, it was a very significant

deal for Pecom because it implied doubling the size of the company. Thirdly,

the regional nature of the deal, with Bolland having operating companies not

only in Argentina, but in Brazil, Bolivia and Colombia, made it quite complex.

The transaction took a lot of time, especially because we had to coordinate due

diligence throughout these different countries. Also, the target was run like a

family company, so we had to work a lot with the sellers to help them develop a

data room. Then, during the negotiations, Argentina devalued the peso, which

had a business impact on the target, so that had to be negotiated as well.

TTR:

How was the transaction financed and how long did it take to close?

EA: The Perez Companc Group has available

funds to finance the deal, so we did not have to negotiate any financing

agreement. It took 10 months between execution of the non-binding offer and

closing.

TTR:

Why was the target considered a good complement to Pecom’s existing operations?

EA: Bolland produced pumps for the oil and

gas industry, while Pecom didn’t have a pump business. They also had a

chemicals business, and that was also an area in which Pecom was not present.

It was a strategic acquisition that transformed Pecom into a full services

provider.

TTR:

What became of Bolland’s minority partner in the Colombian operating company?

EA: A Colombian businessman had a 30% stake

in the Colombian subsidiary. He’s a Colombian investor who saw an opportunity

to exit, so he tried to apply pressure for the sale of his stake, and Pecom

decided it was easier not to have a minority shareholder in Colombia. At the

time of closing we negotiated a term sheet for the acquisition of his stake and

that acquisition was negotiated and consummated after closing of the first

deal. It was not a substantial amount compared to the larger deal.

TTR:

How will Pecom leverage Bolland’s interntional presence?

EA: Increasing its operations across the

region is definitely an objective for Pecom now that it has become the biggest

local player in Argentina through this transaction. Bolland had operating

subsidiaries where Pecom didn’t have any presence at all and can now look at

how to increase their market participation in these markets with their full

portfolio of products and services.

TTR:

How hard will this acquisition be for Pecom to integrate?

EA: Integration will be a big challenge for

Pecom. It’s acquiring a target that’s almost as big as itself. Though Pecom is

a family-owned company, it was run more like an international company in terms

of corporate governance and labor standards. Bolland had almost 800 employees

that will need to adjust to new policies and a different compensation scheme.

From a real estate perspective, Pecom will have to move its headquarters to a

new building that is being constructed now because the entire staff couldn’t

all fit at the existing facility. IT systems will need to be integrated too,

which is also a challenge.

TTR:

What other deals do you see on the horizon for Pecom?

EA: We are now involved in one ongoing

transaction where the group is negotiating another important acquisition

related to the energy industry. I cannot offer more details on that as a binding

agreement has yet to be signed. Suffice it to say that they’re looking to

deepen their foothold in Argentina’s oil and gas industry and this is not the

last of their investments.

TTR:

How was the valuation arrived at and how pleased were the sellers?

EA: The sellers were satisfied with the

outcome. Despite the devaluation that happened in the midst of negotiations,

the purchase price, which was denominated in dollars, was not modified.

Some of the sellers considered their stake

in Bolland as a retirement plan to see dividends forever and many didn’t want to

assume liabilities and indemnifications with the sale. The fact that the price

was good helped appease the detractors.

TTR:

Which practice areas were critical to your firm’s work on the deal?

EA: In the diligence process we had lawyers

from all fields, including oil and gas and environmental because Bolland had a

chemicals business that produced products used to enhance the productivity of

wells. The real estate practice was also important because there were assets

located in border areas, which means you have apply for special permissions with

Argentina’s Ministry of the Interior owing to security issues. Labor law also come

into play because the target had unionized employees and commercial litigation attorneys

were also heavily involved.

TTR:

What makes this deal stand out among other transactions you’ve worked on?

EA: It’s not that common for an Argentine company

to acquire a regional target. The coordination required to perform due

diligence in four countries makes it stand out. Also, In Argentina, it’s not

that common to see such large transactions, though perhaps the sum is not that

material for an international transaction. Thirdly, from a business and

psychological aspect, it was a really keystone transaction for our client. The

client was really focused and needed to take care of every detail. For all

these reasons it was a very important transaction for us and it took a lot of

time. It was also really important for the client given that it resulted in the

biggest player in Argentina.

TTR:

What does this deal say about the level of confidence in Argentina?

EA: This transaction serves as a vote of

confidence, especially at a time when the Macri administration was having some

difficulties in the face of a recession and nervousness due to inflation, with

several investors, especially international investors, delaying their

investments. The first ones that take advantage of these opportunities are

local players, eager to take a chance. They’re here for the long run. Hopefully

international investors will follow.

DealMaker Q&A

Posted on

TTR DealMaker Q&A with Payet, Rey, Cauvi, Pérez Abogados Associate Alan García

Deal

Summary:

On 30 November 2018, Lima-based asset management firm Sigma SAFI acquired a 51% interest in the Parque Eólico Marcona and Parque Eólico Tres Hermanas from Grupo Cobra for USD 56m, consolidating its ownership of Peru’s largest wind farms with a combined installed capacity of 130MW between them. The wind farms were developed by Grupo Cobra, a Spain-based subsidiary of ACS, with financing provided by a consortium of institutions including Eximbank, KFW DEG, FMO, CAF, Proparco and Natixis.TTR DealMaker Q&A with Payet, Rey, Cauvi, Pérez Abogados Associate Alan García

Alan García

Payet, Rey, Cauvi, Pérez Abogados Associate Alan García discusses details of a complex transaction that saw Sigma SAFI consolidate its ownership of Peru’s largest wind farm assets by paying off legacy creditors in the country’s first ever co-issuance.

TTR: How long have you been working with Sigma SAFI and how did you land this mandate?

AG:

We’ve had a relationship with Sigma SAFI that spans several years. We

represented the fund manager in 2015 and 2016 when it acquired its initial 49%

interest in the two wind farms when Grupo Cobra retained its 51% stake. A

couple of months ago we carried out a restructuring of the debt held by each

entity, and from there we executed the acquisition. It was logical that we

could be of value to the buyer given our understanding of the refinancing

arrangement, which was a precursor to the acquisition. There were eight

financial entities involved with mirrored contracts for Tres Hermanas and

Marcona, each with its own project finance with all the associated step-in

rights.

TTR: What made this

transaction so complicated?

AG:

The deal was complex because it required prepaying debt held by international

development banks and simultaneously carrying out a private placement, all on

the heels of a refinancing. Each project company had to be handled

independently with their respective assets and concession agreements used as

guarantees to the creditors. The complexities of the deal relate to its

structure of guarantees that couldn’t be shared between entities and the

symmetrical contracts that were drafted under New York and Peruvian Laws. The

sequence of execution of the various contracts required to carry out the deal within

a short period given to eliminate prior liens made the transaction especially

challenging.

TTR: What makes this

deal unique?

AG:

This was the first co-issuance of notes by Peruvian issuers in Peru’s history. Being

a replacement of debt and guarantees, basically with one project finance

substituted by another, makes this deal stand out, especially given that

between them the two wind farms represent 60% of the wind power capacity in

Peru.

TTR: Which practice

areas were involved?

AG:

We had two teams working simultaneously, one dedicated to the acquisition and

the other to the refinancing. Both teams were led by Finance and Capital

Markets Partner Eduardo Vega and me, with parallel negotiations. We had corporate,

tax, regulatory and energy specialists in each with a total of eight attorneys.