Relatório mensal sobre o mercado transacional brasileiro – Julho 2025

Posted on

Fusões e Aquisições movimentam BRL 173,3bi em 2025

Setor de Internet, Software & IT Services é o mais ativo do ano, com 187 transações

Estados Unidos é o país que mais investiu no Brasil, com 89 aquisiçõeso país que mais investiu no Brasil, com 56 aquisições

Volume de transações registra crescimento de 3% no período

Em Asset Acquisitions, houve um aumento de 14% volume de operações

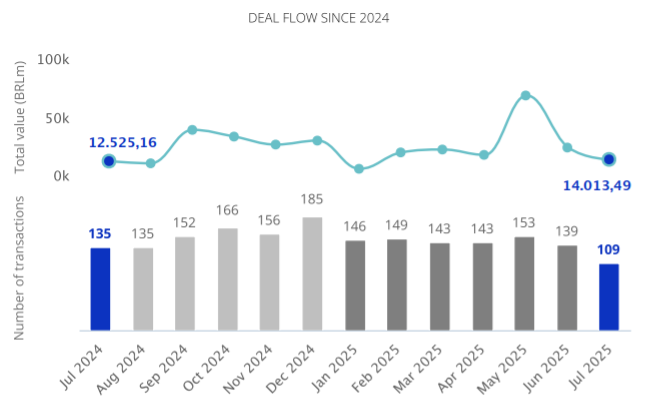

O cenário transacional brasileiro foi objeto de análise no relatório mensal do TTR Data, que revelou 982 transações movimentando um total de BRL 173,3bi até julhode 2025.

Esses números representam um crescimento de 3% no número de transações em relação ao mesmo período de 2024, tal como um aumento no capital mobilizado em 33%. Do total das transações, 37% possuem os valores revelados e 82% das operações já estão concluídas.

Em julho, 109 fusões e aquisições foram registradas, entre anunciadas e concluídas, e um valor total de BRL 14,0bi.

O setor de Internet, Software & IT Services é o mais ativo com 187 transações, apresentando uma queda de 2% em relação a 2024, seguido pelo setor de Real Estate, com 92 transações.

Operações do mercado transacional de julho de 2024 a julho de 2025 Fonte: TTR Data.

Âmbito Cross-Border

Empresas brasileiras voltaram-se principalmente para os Estados Unidos, realizando 34 transações no valor de BRL 8,0bi até julho de 2025, seguido por Portugal com oito operações.

Por outro lado, os Estados Unidos e o Reino Unido lideraram os investimentos no Brasil, com 89 e 19 transações, respectivamente.

Empresas norte-americanas que adquirem negócios brasileiros registraram uma queda de 6%, as aquisições estrangeiras nos setores de Tecnologia e Internet diminuiram em 12%.

Em relação aos fundos estrangeiros de Private Equity e Venture Capital que investem em empresas brasileiras, houve uma queda de 12% em 2025.

Private Equity, Venture Capital e Asset Acquisitions

No segmento de Private Equity, houve 56 transações totalizando BRL 16,9bi, com um crescimento de 49% no capital mobilizado.

Em Venture Capital, 205 rodadas de investimento movimentaram BRL 7,2bi, representando um aumento de 16% no total investido.

O segmento de Asset Acquisitions registrou 179 transações e BRL 44,0bi até julho, refletindo um crescimento de 14% no volume em comparação ao mesmo período do ano passado.

Transação do mês

A transação destacada pelo TTR Data em julho de 2025, foi a conclusão da venda de 20% pela EDP Brasil do Porto de Pecém para a Diamante Geração de Energia. O valor da transação é de BRL 200m. A operação contou com a assessoria jurídica em lei brasileira dos escritórios Miguel Neto Advogados; Faveret | Lampert Advogados; Pinheiro Guimarães; Cescon, Barrieu Flesch & Barreto Advogados. O Banco Bradesco BBI realizou a assessoria financeira.

Entrevista com Candido Martins Kukier

Henrique de Faria Martins, sócio fundador do Candido Martins Kukier, conversou com o TTR para esta edição e analisou o desempenho do mercado brasileiro de fusões e aquisições e as dinâmicas do ritmo das operações em 2025: “O mercado brasileiro de fusões e aquisições tem sofrido bastante desde 2023 e 2025 não está diferente. No entanto, depois de alguns anos ruins, estamos vendo alguns sinais de recuperação e adaptação após um período de incertezas macroeconômicas e políticas. Observamos que os investidores estratégicos estão olhando mais para o país. No entanto os motivos podem ser desde a desvalorização da nossa moeda, falta de oportunidades em outros países ou estabilidade. Estamos presenciando uma busca por consolidação em setores fragmentados e oportunidades de aquisição de ativos em situação especial (special situations). Os fundos de private equity estão mais focados nos add-ons (investidas comprando outras empresas) do que em teses novas. Estão mais seletivos. Notamos o crescimento de investidores estrangeiros olhando para o Brasil com foco em estruturas societárias mais robustas, compliance e planejamento sucessório. Apesar de todas as questões políticas e fiscais, o Brasil segue como uma alternativa muito boa e com estabilidade. O Brasil continua oferecendo ativos de alta qualidade a valuations atrativos.”

O relatório publica os rankings de assessoria financeira e jurídica até julho de 2025 em M&A, Private Equity, Venture Capital e Mercados de Capitais, onde a atividade dos assessores é refletida pelo número de transações e pelo valor total.

Quanto ao ranking de assessores financeiros, por número de transações e em valor lidera em 2025 o Banco Bradesco BBI com 19 operações e um total de BRL 46,2bi.

No que se refere ao ranking de assessores jurídicos, por número de transações e em valor lidera o escritório Mattos Filho, com 53 operações e contabilizando um total de BRL 47,5bi.

Relatório mensal sobre o mercado transacional brasileiro – Maio 2025

Posted on

Fusões e Aquisições movimentam BRL 120,0bi até maio de 2025

Setor de Internet, Software & IT Services é o mais ativo do ano, com 126 transações

Estados Unidos é o país que mais investiu no Brasil, com 56 aquisições

Capital mobilizado registra crescimento de 45% no período

Em Asset Acquisitions, houve um aumento de 18% volume de operações

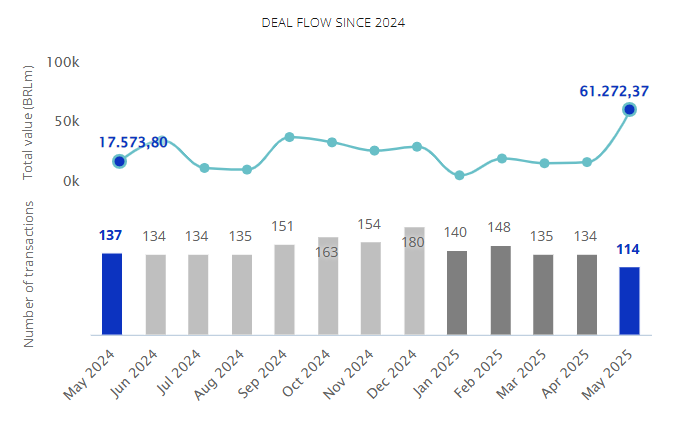

O cenário transacional brasileiro foi objeto de análise no relatório mensal do TTR Data, que revelou 671 transações movimentando um total de BRL 120,0bi até maio de 2025.

Esses números representam uma diminuição de 1% no número de transações em relação ao mesmo período de 2024, no entanto, o capital mobilizado cresce em 45%. Do total das transações, 36% possuem os valores revelados e 82% das operações já estão concluídas.

Em maio, 114 fusões e aquisições foram registradas, entre anunciadas e concluídas, e um valor total de BRL 61,2bi.

O setor de Internet, Software & IT Services é o mais ativo com 126 transações, apresentando uma queda de 2% em relação a 2024, seguido pelo setor de Real Estate, com 63 transações.

Operações do mercado transacional de maio de 2024 a maio de 2025 Fonte: TTR Data.

Âmbito Cross-Border

Empresas brasileiras voltaram-se principalmente para os Estados Unidos, realizando 27 transações no valor de BRL 1,4bi até maio de 2025, seguido por Portugal com sete operações.

Por outro lado, os Estados Unidos e o Reino Unido lideraram os investimentos no Brasil, com 56 e 11 transações, respectivamente.

Empresas norte-americanas que adquirem negócios brasileiros registraram uma queda de 20%, as aquisições estrangeiras nos setores de Tecnologia e Internet diminuiram em 21%.

Em relação aos fundos estrangeiros de Private Equity e Venture Capital que investem em empresas brasileiras, houve uma queda de 6% em 2025.

Private Equity, Venture Capital e Asset Acquisitions

No segmento de Private Equity, houve 39 transações totalizando BRL 14,8bi, com um crescimento de 114% no capital mobilizado.

Em Venture Capital, 145 rodadas de investimento movimentaram BRL 5,4bi, representando um aumento de 21% no total investido.

O segmento de Asset Acquisitions registrou 130 transações e BRL 33,9bi até maio, refletindo um crescimento de 18% no volume em comparação ao mesmo período do ano passado.

A operação contou com a assessoria jurídica em lei brasileira dos escritórios Demarest Advogados; Coelho & Dalle Advogados; e Pinheiro Neto Advogados. A KPMG Portugal realizou a assessoria financeira.

Ranking de assessores financeiros e jurídicos

O relatório publica os rankings de assessoria financeira e jurídica até maio de 2025 em M&A, Private Equity, Venture Capital e Mercados de Capitais, onde a atividade dos assessores é refletida pelo número de transações e pelo valor total.

Quanto ao ranking de assessores financeiros, por número de transações e em valor lidera em 2025 o Banco Itaú BBA com 11 operações e contabilizando um total de BRL 7,5bi.

Quanto ao ranking de assessores financeiros, por número de transações lidera em 2025 o Banco Itaú BBA com 13 operações. Em valor, lidera o BTG Pactual contabilizando um total de BRL 28,1bi.

No que se refere ao ranking de assessores jurídicos, por número de transações em 2025 lidera o escritório Mattos Filho, com 33 operações. Em valor, lidera o Lefosse contabilizando um total de BRL 35,1bi.

Dealmaker Q&A

Posted on

TTR Data Dealmaker Q&A with Brigard Urrutia M&A Partner Tomás Holguín

Partner since 2020, with more than 10 years of experience. In the time he has been practicing, he has worked in different areas of practice as antitrust and corporate law and is recognized for his knowledge in corporate law. He worked as a foreign associate at Pinheiro Neto Advogados in Brazil (2012) and in Simpson Thacher & Barleth in New York (2016).

He is a graduate of the Universidad del Rosario and earned his Master of Law degree from the University of Columbia Law School, New York in 2015.

TTR: What is your assessment of the performance of the M&A market in Colombia and Latin America during the first months of 2025? What dynamics are setting the tone for investors and advisors?

The M&A market in Colombia and Latin America is seasonal—it typically starts slowly in the early months of the year and gains momentum over time. However, uncertainty stemming from recently adopted U.S. tariff policies has undoubtedly impacted investment decisions, adding an extra handbrake to the already slow start of the year.

Having said that, we have seen some interesting activity in large-scale deals during these first months, such as the share purchase agreement signed between Millicom and Telefónica for the acquisition of Telefónica’s stake in Coltel (Movistar), which adds dynamism to the M&A market in Colombia. As has happened before, we expect market stabilization to lead to a rebound in the number of acquisitions and integrations in the remainder of the year.

TTR:In strategic sectors such as energy, infrastructure, technology, or financial services, what would you say are the main regulatory or structural challenges currently faced by transactions in Colombia and Latin America?

In Colombia, more than regulatory entry barriers—which certainly remain—we’ve observed operational hurdles, particularly due to difficulties in obtaining regulatory approvals from government agencies, which sometimes do not operate at the same pace as business decisions.

TTR:How have geopolitical changes and regulatory developments in Colombia impacted M&A transactions with foreign participation? Has cross-border dealmaking become more complex so far in 2025?

We are watching closely to see what Colombia’s access to the New Silk Road will bring for several sectors, including the renewable energy market, which continues to show significant activity. Despite global uncertainty regarding U.S. tariff policy in the region, tariffs for Colombia remain low, which gives us more room to maneuver in contrast.

That said, it is no secret that foreign investment from the U.S. in Colombia has declined compared to previous years. Regulatory changes and uncertainty about the direction of public policy in key economic sectors now require more detailed and rigorous legal analysis. Paradoxically, this adds dynamism to the market by pushing investors to make decisions quickly.

TTR:Has Brigard Urrutia noticed a change in the predominant buyer profile so far this year? What role are investment funds playing compared to corporate buyers?

Bluntly: no. In Colombia, we continue to see traditional players carrying out local acquisitions. We’ve also observed investment funds entering the market, as well as strategic buyers executing long-term investment plans.

TTR:What are your expectations for the second half of the year? What local or global factors could boost or slow down M&A activity in Colombia?

We anticipate an increase in transactions in the technology sector due to widespread demand for these services. Given the government’s focus on sustainability and energy transition, we also expect deals in the renewable energy sector to develop further. All of this will depend on the stabilization of the regulatory framework, supply chains, interest rates, and how bilateral relations with the United States and China unfold.

TTR:What are the main challenges Brigard Urrutia faces in the current Colombian transactional market? In what types of deals are you observing greater sophistication or sensitivity?

The economic and political environment undoubtedly permeates the M&A market. Law firms face the challenge of adapting to new realities within short timeframes while continuing to deliver top-tier legal services. Keeping up with both domestic and international regulatory changes has become a daily task, and a necessity for strategically planning transactions and overcoming obstacles in real time. This requires us to be more creative, more thorough, and to better leverage our experience—which we enjoy!

TTR:From your experience, what benefits does the TTR Data platform provide in your day-to-day legal work in M&A? How does it help you detect opportunities or anticipate movements?

TTR Data helps us stay informed in real time about the latest market movements and emerging trends, which allows us to predict, to some extent, how the market might behave in the medium term. It also helps keep things in perspective by providing a regional outlook and offering useful precedents when navigating uncertain times.

This strengthens our understanding of the market and its players and deepens our ability to align current market conditions with our clients’ objectives and needs. It enables us to help clients build informed investment strategies while assessing, as accurately as possible, the risks inherent to each transaction.

Socio desde 2020, con más de 10 años de experiencia. En el tiempo que lleva ejerciendo su profesión, se ha desempeñado en diferentes áreas de práctica como competencia y derecho corporativo y es reconocido en el medio por su conocimiento en derecho societario. Trabajó como asociado extranjero en las firmas Pinheiro Neto Advogados en Brasil (2012) y en Simpson Thacher & Barleth en Nueva York (2016).

Es egresado de la Facultad de Jurisprudencia del Colegio Mayor de Nuestra Señora del Rosario y obtuvo su título de Magíster en Derecho en la Facultad de Derecho de la Universidad de Columbia, Nueva York en 2015.

TTR: ¿Cuál es su evaluación sobre el desempeño del mercado de M&A en Colombia y América Latina durante los primeros meses de 2025? ¿Qué dinámicas están marcando el tono para inversores y asesores?

El mercado de M&A en Colombia y América Latina es estacional: suele comenzar con lentitud en los primeros meses del año y ganar impulso con el tiempo. Sin embargo, la incertidumbre derivada de las políticas arancelarias recientemente adoptadas por EE. UU. ha impactado sin duda las decisiones de inversión, añadiendo un freno adicional al ya lento inicio del año.

Dicho esto, hemos observado cierta actividad interesante en operaciones de gran escala durante estos primeros meses, como el acuerdo de compraventa de acciones firmado entre Millicom y Telefónica para la adquisición de la participación de Telefónica en Coltel (Movistar), lo cual aporta dinamismo al mercado de M&A en Colombia. Como ha sucedido antes, esperamos que la estabilización del mercado conlleve un repunte en el número de adquisiciones e integraciones en lo que resta del año.

TTR: En sectores estratégicos como energía, infraestructura, tecnología o servicios financieros, ¿cuáles diría que son hoy los principales retos regulatorios o estructurales que enfrentan las transacciones en Colombia y América Latina?

En Colombia, más que barreras regulatorias de entrada —que ciertamente persisten— hemos observado obstáculos operativos, particularmente por las dificultades para obtener aprobaciones regulatorias por parte de entidades gubernamentales, que en ocasiones no operan al mismo ritmo que las decisiones empresariales.

TTR: ¿Cómo han impactado los cambios geopolíticos y regulatorios en Colombia a las transacciones de M&A con participación extranjera? ¿Se ha vuelto más complejo el dealmaking cross-border en lo que va de 2025?

Estamos observando de cerca lo que implicará el acceso de Colombia a la Nueva Ruta de la Seda para varios sectores, incluido el de energía renovable, que sigue mostrando una actividad significativa. A pesar de la incertidumbre global sobre la política arancelaria de EE. UU. en la región, los aranceles para Colombia siguen siendo bajos, lo que nos da un mayor margen de maniobra en contraste.

Dicho eso, no es un secreto que la inversión extranjera proveniente de EE. UU. en Colombia ha disminuido en comparación con años anteriores. Los cambios regulatorios y la incertidumbre sobre la orientación de la política pública en sectores económicos clave hoy exigen un análisis jurídico más riguroso y detallado. Paradójicamente, esto dinamiza el mercado al empujar a los inversionistas a tomar decisiones con mayor rapidez.

TTR: ¿Ha notado Brigard Urrutia un cambio en el perfil predominante de comprador en lo que va del año? ¿Qué papel están desempeñando los fondos de inversión frente a los compradores corporativos?

De forma directa: no. En Colombia, seguimos viendo a los actores tradicionales realizando adquisiciones locales. También hemos observado la entrada de fondos de inversión y compradores estratégicos que están ejecutando planes de inversión de largo plazo.

TTR: ¿Cuáles son sus expectativas para el segundo semestre del año? ¿Qué factores locales o globales podrían impulsar o ralentizar la actividad de M&A en Colombia?

Anticipamos un aumento en las transacciones del sector tecnológico debido a la alta demanda generalizada de estos servicios. Dado el enfoque del gobierno en sostenibilidad y transición energética, también esperamos que se desarrollen más operaciones en el sector de energías renovables. Todo esto dependerá de la estabilización del marco regulatorio, las cadenas de suministro, las tasas de interés y la evolución de las relaciones bilaterales con Estados Unidos y China.

TTR: ¿Cuáles son los principales desafíos que enfrenta Brigard Urrutia en el mercado transaccional colombiano actual? ¿En qué tipos de operaciones están observando mayor sofisticación o sensibilidad?

El entorno económico y político sin duda permea el mercado de M&A. Las firmas legales enfrentamos el desafío de adaptarnos a nuevas realidades en plazos cortos, sin dejar de ofrecer servicios jurídicos de primer nivel. Estar al día con los cambios regulatorios locales e internacionales se ha vuelto una tarea cotidiana y una necesidad para planificar estratégicamente las transacciones y sortear obstáculos en tiempo real. Esto nos exige ser más creativos, más minuciosos y aprovechar mejor nuestra experiencia —¡y lo disfrutamos!

TTR: Desde su experiencia, ¿qué beneficios les aporta la plataforma TTR Data en su trabajo jurídico diario en M&A? ¿Cómo les ayuda a detectar oportunidades o anticipar movimientos?

TTR Data nos permite mantenernos informados en tiempo real sobre los últimos movimientos del mercado y tendencias emergentes, lo que nos ayuda a prever, hasta cierto punto, cómo puede comportarse el mercado en el mediano plazo. También contribuye a mantener la perspectiva al ofrecer una visión regional y brindar precedentes útiles en tiempos de incertidumbre.

Dealmaker Q&A

Posted on

TTR Data Dealmaker Q&A con Carolina Albuerne, socia de Uría Menéndez

Carolina Albuerne se incorporó a Uría Menéndez en septiembre de 2005. Es abogada del equipo de Corporate-M&A de la oficina de Madrid, ha estado desplazada en las oficinas de Barcelona y Nueva York y es socia de la firma desde 2022. Carolina ha adquirido una amplia experiencia en el ámbito societario, M&A, mercado de valores así como en el área regulatorio bancario. Nombrada mejor abogada de España menor de 40 años por Forbes en 2019, en 2020 la reconocida publicación británica Global Banking Regulation Review (GBRR) nombró a Carolina una de las 45 mejores abogadas del mundo en regulación bancaria menores de 45 años. Carolina Albuerne asesora en grandes operaciones de fusiones y adquisiciones y en reorganizaciones y reestructuraciones corporativas transfronterizas y nacionales en las que participan bancos españoles.

Carolina también asesora en operaciones que implican deuda híbrida y otros instrumentos de capital cualificados según la normativa bancaria, así como en el diseño de estructuras de capital eficientes desde una perspectiva regulatoria. Proporciona también asesoramiento jurídico de forma recurrente a los bancos en materia de gobierno corporativo y en la aplicación de la normativa de resolución.

¿Cuáles son las tendencias más destacadas que están moldeando el mercado de fusiones y adquisiciones en España y Europa en 2025? ¿Cómo crees que estas tendencias influirán en la estrategia de las firmas legales en los próximos años?

Las tensiones geopolíticas y, más recientemente, las comerciales están marcando la agenda. El anuncio de tarifas de Estados Unidos está teniendo un efecto devastador en la confianza del mercado. En este contexto, la reacción de muchos inversores a la incertidumbre es la habitual: protegerse y wait and see, y eso se ve en el menor apetito inversor.

El marco global favorece —al menos parcialmente— los procesos de renacionalización de las cadenas de producción y suministro. Quizás también con un menor énfasis global en la descarbonización. Es difícil que la Unión Europea pueda ser ajena a estas macrotendencias.

Una solución rápida y satisfactoria de la crisis tarifaria sería muy positiva para la confianza del mercado en Europa. Si se logra, los grandes programas de inversión pública europeos, especialmente el de Alemania, puede tener efectos muy positivos en ciertas industrias, como la de defensa o la de telecomunicaciones.

Para el sector bancario quizás la perspectiva sea más mixta. Por un lado, los mayores programas de inversión pública y las mayores tarifas comerciales pueden tener efectos inflacionarios a medio plazo, pero a corto plazo la volatilidad del mercado podría obligar a los bancos centrales a moderar o bajar los tipos de interés.

¿Qué sectores económicos están mostrando mayor dinamismo y oportunidades en términos de operaciones de M&A en España? ¿Qué factores están impulsando este crecimiento en dichos sectores?

Como apuntaba, quizás los sectores relacionados con defensa, telecomunicaciones, minería y sector financiero son aquellos con un entorno previsiblemente más favorable; pero todo puede cambiar rápidamente.

¿Qué impacto podría tener la actividad del mercado transaccional en el sector bancario en España y en la consolidación del mercado financiero europeo?

Los programas de gasto público ligados a la defensa podrían previsiblemente tener un efecto inflacionario que provoque un entorno con tipos de interés más elevados de los esperados hace unos meses.

Y esto sería positivo para el sector financiero, y en particular para el bancario. En ese entorno, cabría esperar en la Unión Europea nuevos procesos de M&A, buscando mayores economías de escala, en un entorno donde la mayor parte de los bancos europeos están fuertemente capitalizados, con baja morosidad y, por fin, con una elevada rentabilidad.

Sin embargo, no es menos cierto que la enorme volatilidad del mercado en los últimos días puede incrementar la mentalidad defensiva en el sector bancario y provocar un nuevo retraso en estos procesos de consolidación.

Las perspectivas para 2025 y para 2026 podrá depender, además del componente macro (que no es menor), de la evolución de los procesos de concentración bancaria que actualmente protagonizan las entidades italianas, y en particular Unicredit. Habrá que ver si tiene éxito en su operación con Commerzbank, porque se trataría de la primera integración bancaria transfronteriza en muchos años, un verdadero breakthrough. No es un secreto que las instituciones comunitarias, como la Comisión Europea o el Banco Central Europeo, están muy interesadas en los procesos de concentración transfronterizos en la Unión para crear entidades con escala para competir globalmente con las entidades americanas o chinas.

Creo también que la posible desaparición de la incertidumbre regulatoria puede ayudar a dar mayor claridad a los inversores bancarios. Y parece que la música ha cambiado por primera vez en casi veinte años: por primera vez se habla seriamente de desregulación. Esto puede actuar como un incentivo adicional para el M&A en este sector.

Considerando tu participación en grandes operaciones internacionales, ¿cuáles son los principales desafíos que enfrentan las firmas legales al asesorar en transacciones transfronterizas? ¿Cómo se pueden superar estos obstáculos para garantizar el éxito de las operaciones?

Lo primero es que para un buen delivery en estas operaciones no se necesita tener una oficina en cada país. De hecho, una de las cosas que nos da más flexibilidad, y que en despachos como Uría Menéndez podemos hacer, es elegir —para cada jurisdicción— los despachos que queremos tener en nuestro equipo para cada operación, típicamente nuestra red de best friends, despachos de elite en los principales países europeos.

Pero tenemos muchas otras opciones en el caso, por ejemplo, de que estén conflictuados o por la razón que sea consideremos que otro asesor encaja mejor en una determinada operación. Además de buenos abogados locales en los que confíes, necesitas flexibilidad, experiencia y, por encima de todo, la capacidad para coordinar grandes equipos en múltiples geografías, a veces en husos horarios distintos. Y esto último (la coordinación para que el trabajo sea homogéneo y acorde a nuestro estándar) es, en mi opinión, lo más complicado, pero donde se marca la diferencia para el cliente.

Desde 2021, has sido reconocida como una de las principales asesoras legales en el mercado de fusiones y adquisiciones en España. Mirando hacia atrás en tu trayectoria, ¿Qué factores consideras que han sido clave para tu crecimiento y reconocimiento en un sector tradicionalmente dominado por perfiles jurídicos masculinos?

Es difícil resumirlo. En mi caso, si tuviera que destacar algunos factores clave, serían la perseverancia y la fiabilidad. Tener una base sólida de conocimientos jurídicos se da por sentado en una firma como la nuestra. Pero lo que marca la diferencia es estar siempre preparada, dar lo mejor de una misma y dejarse la piel por los clientes y por los compañeros. Creo que eso ha sido determinante para ganarme su confianza y para que me involucraran en operaciones relevantes.

A lo largo de los años, no todo ha salido siempre como esperaba, pero cuando tienes claras tus prioridades, es más fácil mantener el rumbo y seguir trabajando con determinación.

En relación con la diversidad, en Uría Menéndez nunca me han hecho sentir “de menos” —tampoco “de más”— por ser mujer. Mi recomendación para cualquier mujer que se plantee una carrera en un despacho es trabajar duro, y los resultados llegarán

Con la evolución constante del entorno económico y regulatorio, ¿qué cambios anticipas en el mercado de fusiones y adquisiciones en el corto y mediano plazo? ¿Cómo deberían prepararse las firmas legales para adaptarse a estos cambios?

Por ahora, no se vislumbran grandes cambios, aparte de los potenciales sectores que pueden ser más protagonistas en el M&A. Todo parece indicar que el private equity seguirá siendo el protagonista de las operaciones de inversión y desinversión, pero habrá que estar a la incierta evolución del mercado.

Previsiblemente, a medida en que se avance en la integración del mercado común, veremos más y más operaciones transfronterizas, así que el perfil de abogado con capacidad de liderar operaciones internacionales es clave. Tampoco se puede ignorar el papel de la inteligencia artificial en el sector legal, con capacidad para automatizar las tareas más rutinarias y de menor valor añadido. Pero no olvidemos una cosa, un buen abogado tiene que ser por encima de todo un asesor de la operación, alguien en quien el cliente confíe. Nuestro rol nunca debe ser el de un mero redactor de contratos.

Por eso, para nosotros, es fundamental seguir invirtiendo en nuestro principal activo, nuestros abogados. En los tiempos que corren, no hay excusas para que un buen abogado no solo tenga que saber de derecho, hablar idiomas y vivir cómodamente en la tecnología; tiene que tener capacidades comerciales y el conocimiento del mercado para ganarse la confianza de sus clientes

Relatório Mensal Portugal – Novembro 2019

Posted on

Mercado português regista 346 Fusões e Aquisições até novembro, alta de 8,4%

No período de janeiro a novembro o mercado transacional português acumula 346 transações, alta de 8,46% em relação ao mesmo período do ano anterior, e caminha para fechar 2019 com números muito próximos ao de 2018, que terminou com 367 negócios mapeados. No período, 130 transações tiveram seus valores divulgados que somaram 8,4 bilhões de euros, o que representa uma redução de 7% ante ao período homólogo de 2018, de acordo com o mais recente Relatório de M&A do TTR -Transactional Track Record

Somente no mês de novembro foram mapeadas pelo TTR – Transactional Track Record 21 transações e um valor total de 143,89 milhões de euros, frente as 26 registadas em novembro de 2018.

O sector Imobiliário apesar de apresentar

ligeira retração, 2%, manteve a posição de mais ativo no período, com 79

transações registadas. Tecnologia em segundo com 52 operações, alta de 27% e

Financeiro aparece em terceiro com 38 deals, alta de 15%

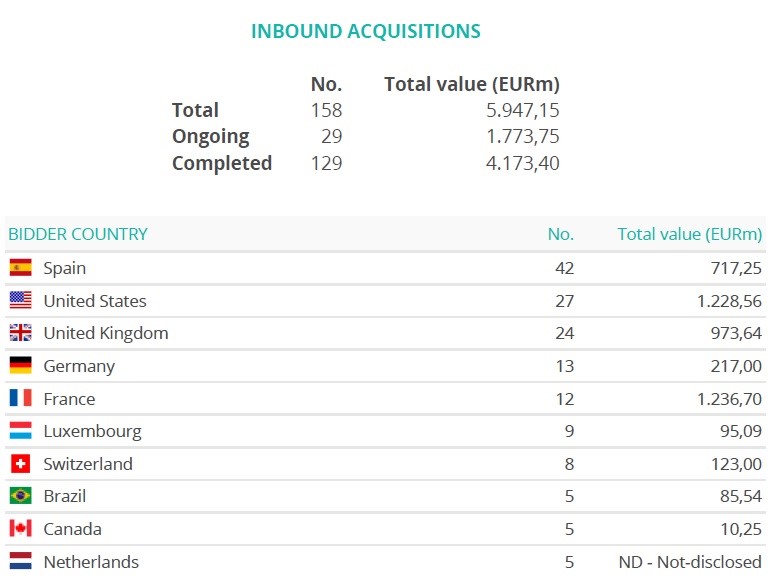

No âmbito das operações cross-border

inbound, em que empresas estrangeiras investiram em companhias baseadas em

Portugal, foram registadas 158 transações. As empresas espanholas seguem como as

mais ativas, com 42 aquisições no período, e especial preferência pelo sector

Imobiliário. Em segunda posição estão as empresas dos Estados Unidos com 27

transações, o que representa um aumento de 35% em relação ao mesmo período do

ano anterior.

Venture Capital

Os investimentos realizados por fundos

de Venture Capital registou alta de 67,5% no número de operações, 67, além de

registar alta de 51,7% no valor total investido que alcançou 348 milhões de

euros.

No número total de investimentos

predominam os de âmbito cross-border, 37 negócios, onde fundos estrangeiros

realizam investimentos em empresas portuguesas.

As empresas que atuam no segmento de

Tecnologia foram as que mais receberam

investimentos com um total de 34 operações, o que representa uma alta de

70%. A Portugal Ventures é a mais ativa com 18 investimentos.

Private Equity

Os investimentos realizados por fundos

de Private Equity somaram 33 negócios até novembro, o que representa redução de

15,38% se comparado ao mesmo período de 2018. Em relação aos valores investidos

apenas oito destes negócios tiveram valores divulgados que somaram 1,59 bilhões

de euros.

Dealmakers

Do ponto de vista dos Dealmakers, termo utilizado pelo TTR para demoninar os profissionais de assessoria, que são atores importantes na dinâminca do mercado de fusões e aquisições português, o relatório traz um completo ranking de assessoria jurídica em transações de Fusões e Aquisições em lei portuguesa, tendo em conta transações que se iniciaram em 2019.

Subscribe to our free newsletter:

This website uses cookies. By continuing to browse the site, you are agreeing to our use of cookies