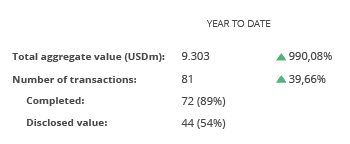

El mercado M&A en Argentina aumenta su actividad un 36% en 2021

- En el transcurso del año se han registrado 200 deals por USD 14.658m

- El sector Tecnología y Financiero y de Seguros, los más activos de 2021

- Empresas estadounidenses adquiriendo empresas argentinas han aumentado un 68% en el año

- Adquisiciones extranjeras en tecnología e Internet han aumentado un 67% en 2021

- Deal destacado: Pampa Energía vende el 51% de Edenor

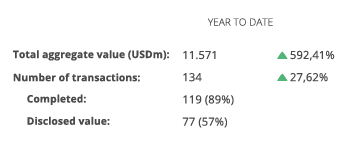

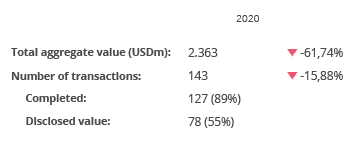

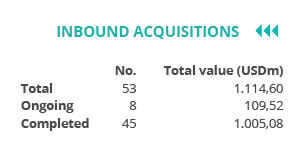

El mercado transaccional argentino ha registrado en 2021 un total de 200 fusiones y adquisiciones, entre anunciadas y cerradas, por un importe agregado de USD 14.658m, según el informe anual de Transactional Track Record.

Estas cifran suponen un aumento del 36% en el número de operaciones y un crecimiento del 516% en el importe de estas, con respecto a diciembre de 2020. Por su parte, en el cuarto trimestre de 2021 se han contabilizado un total de 61 operaciones con un importe agregado de USD 3.037m.

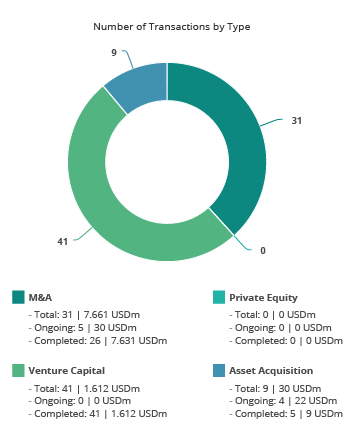

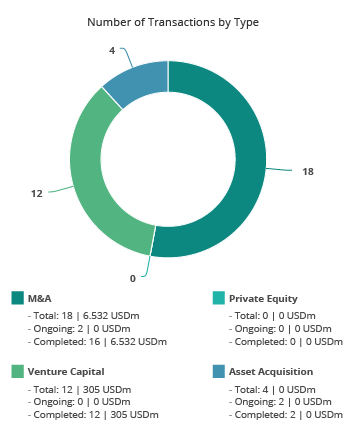

En términos sectoriales, el Tecnológico es el más activo del año, con un total de 77 transacciones, seguido por el sector Financiero y de Seguros, con 61, y el de Internet con 28 operaciones. En términos interanuales, el sector Tecnología ha registrado un aumento del 108%, el sector Financiero y de Seguros ha registrado un alza del 97%, mientras que el sector de Internet ha tenido aumento del 65% en su actividad con respecto a 2020.

Ámbito Cross-Border

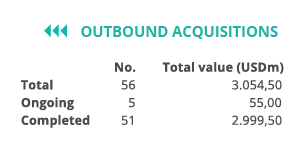

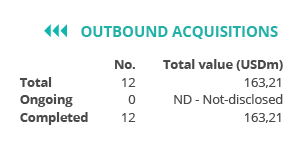

Por lo que respecta al mercado Cross-Border, a lo largo de 2021 las empresas argentinas han apostado principalmente por invertir en Brasil y México, con 39 y 14 transacciones, respectivamente. Por importe destaca España, con USD 2.290m.

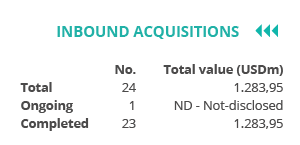

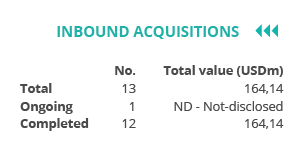

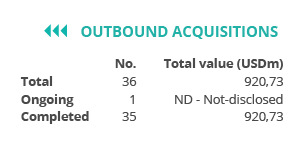

Por otro lado, Estados Unidos, es el país que más ha apostado por realizar adquisiciones en Argentina, con 32 operaciones, seguido de Brasil con 17 transacciones. Por importe, se destaca Estados Unidos, con USD 2.032m.

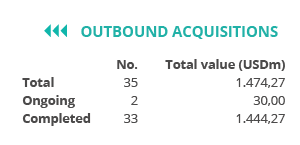

Por su parte, las empresas estadounidenses que adquieren empresas argentinas han aumentado en un 68% hasta el mes de diciembre, con respecto al mismo periodo de 2020, mientras que las adquisiciones extranjeras en los sectores de tecnología y Internet han registrado un aumento del 67% con respecto a diciembre de 2020.

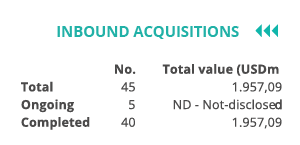

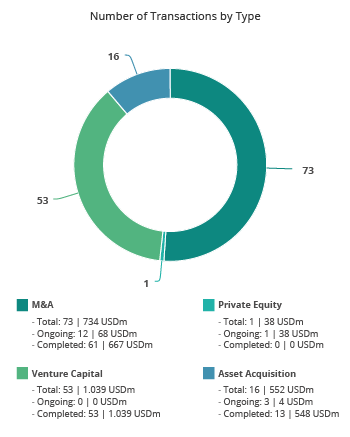

En cuanto los fondos extranjeros de Private Equity y Venture Capital invirtiendo en empresas argentinas, se han registrado 2 transacciones, lo que representa un aumento interanual del 100% en el transcurso de 2021.

Private Equity y Venture Capital

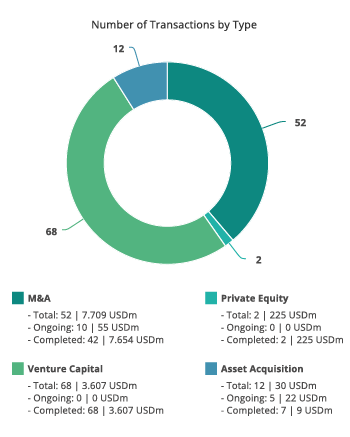

En 2021 se han producido un total de 2 transacciones de Private Equity valoradas en USD 225m, las cuales representan una tendencia estable en el número de operaciones y un aumento del 70% en el importe de las mismas con respecto al mismo periodo de 2020.

Por su parte, en 2021, Argentina ha registrado 103 operaciones de Venture Capital valoradas en USD 4.788m, lo que representa un aumento del 81% en el número de operaciones y un aumento del 359% en el capital movilizado con respecto al mismo periodo del año pasado.

Asset Acquisitions

En el mercado de adquisición de activos, se han cerrado hasta diciembre 14 transacciones con un importe de USD 855m, lo cual implica un descenso del 12% en el número de operaciones y un aumento del 56% en su importe con respecto al mismo periodo de 2020.

Transacción Destacada del Año

Para 2021, Transactional Track Record ha seleccionado como operación destacada la relacionada con Pampa Energía, la cual ha vendido el 51% de Edenor.

La operación, valorada en USD 95m, ha estado asesorada en la parte legal por Alfaro Abogados.

Por la parte financiera, la transacción ha sido asesorada por Santander Corporate Investment Banking (SCIB).

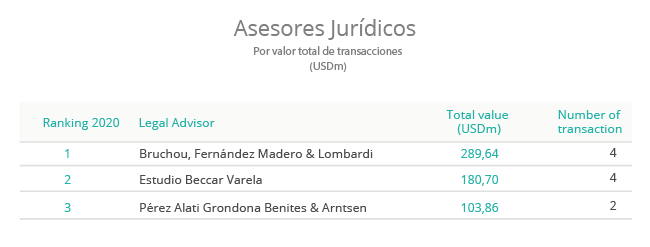

Ranking de Asesores Legales

En el ranking TTR de asesores jurídicos, por número de operaciones e importe, lidera en el año Marval O’Farrell Mairal con 9 operaciones y USD 530m.