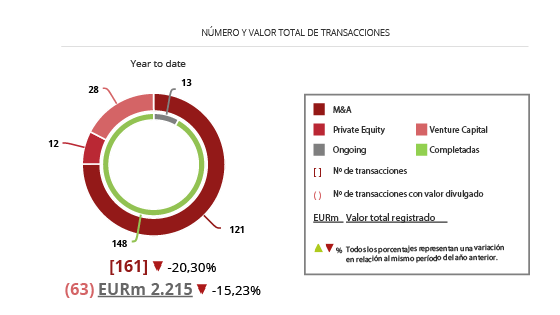

El mercado transaccional español registra EUR 2.215m de capital movilizado en enero de 2019

En el mes se han contabilizado 161 transacciones de M&A

El sector Inmobiliario es el más activo del periodo, con 56 transacciones

Enero registra 12 operaciones de Private Equity y 28 de Venture Capital

El mercado transaccional español ha registrado en el mes de enero 161 fusiones y adquisiciones, de las cuales 63 contabilizan un importe agregado de EUR 2.215m, según el informe mensual de TTR . Estas cifras suponen una disminución del 20,30% en el número de transacciones y un descenso del 15,23% en el importe de las mismas, con respecto al mes de enero de 2018.

En términos sectoriales, el sector Inmobiliario ha sido el más activo de enero, con un total de 56 transacciones, seguido por el de Tecnología, con 20.

Ámbito Cross-Border

Por lo que respecta al mercado Cross-Border en enero de 2019 las empresas españolas han elegido como principales destinos inversión a Portugal, con 7 operaciones, y a Brasil, con 5 transacciones. En términos de importe, Portugal es el país en el que España ha realizado un mayor desembolso, con un valor aproximado de EUR 212,20m.

Por otro lado, Estados Unidos y Reino Unido, con 12 operaciones cada uno, son los países que mayor número de inversiones han realizado en España. Por importe destaca Suiza, con un importe de EUR 297,33m.

PrivateEquity y Venture Capital

En el primer mes de 2019 se han contabilizado un total de 12 operaciones de PrivateEquity por EUR 280,44m, lo cual supone un descenso del 43% en el número de operaciones y del 22% en el importe de las mismas, respecto al mismo periodo del año anterior.

Por su parte, en el mercado de Venture Capital se han llevado a cabo 28 transacciones con un importe agregado de EUR 103,31m, lo que implica una reducción del 32% en el número de operaciones y del 72% en el importe de las mismas, en términos interanuales.

Mercado de capitales

En el mercado de capitales español se ha cerrado en el mes de enero cuatro ampliaciones de capital, por importe de EUR 285,43m.

La operación, que ha registrado un importe de EUR 1.647,66m, ha estado asesorada por la parte legal por DLA Piper España, Uría Menéndez España, Pérez-Llorca, Slaughter And May UK, Y Linklaters Spain. Por la parte financiera, han participado Goldman Sachs International, J.P. Morgan Securities, y Bank of America Merrill Lynch.

Por su parte, PwC España ha prestado servicio de fairness opinion; mientras que Linklaters Spain ha actuado en el proceso de Asesoría Jurídica en Financiación de Adquisiciones.

Ranking de Asesores Legales y Financieros

En el ranking TTR de asesores financieros del mercado M&A, por número de operaciones y por capital movilizado, lidera en 2019 Citigroup, con 2 transacciones y con EUR 570m registrados.

En cuanto al ranking de asesores jurídicos del mercado M&A, por importe y por número de transacciones, lidera la firma Latham & Watkins España con EUR 572,81m y 3 operaciones registradas.

Si estás interesado en saber cuales son las firmas más destacadas en España en asesoría jurídica y financiera, haz click aquí.

Relatório Mensal Brasil – Janeiro 2019

Posted on

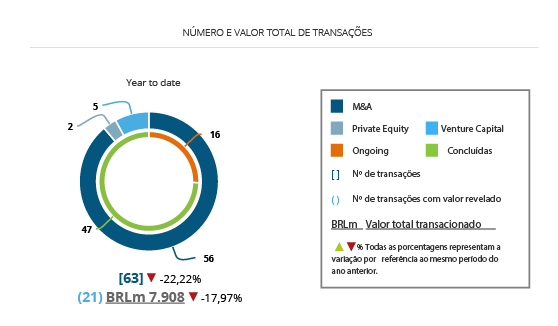

Fusões e Aquisições abrem 2019 com queda de 22% no volume de transações no Brasil

2019 inicia com 63 transações, queda de 22,2% em relação ao mesmo período de 2018

21 operações revelaram valores que chegaram a 7,9 bilhões, baixa de 17,9%

De acordo com o Relatório Mensal da Transactional Track Record, realizado em parceria com a LexisNexis e TozziniFreire Advogados, o primeiro mês de 2019 terminou com 63 anúncios de compra e venda de participação envolvendo empresas brasileiras, uma queda de 22,2% em comparação ao reportado no mesmo período de 2018. Destas, 21 operações tiveram seus valores revelados, totalizando aportes financeiros que chegaram a 7,9 bilhões de reais, baixa de 17,9% ante o mesmo intervalo do ano anterior. Os resultados marcam o pior início de ano desde 2015, quando o mercado de M&A brasileiro movimentou aproximadamente 4,3 bilhões de reais.

O segmento Tecnologia inaugura o ano como o mais alvejado pelos investidores no mercado nacional, contabilizando 16 transações no período, um salto de 23% nos movimentos em relação ao mesmo intervalo do ano anterior. O crescimento dos investimentos no setor acompanha a alta de 14,3% das aquisições estrangeiras no segmento de Tecnologia e Internet.

Financeiro e Seguros aparece na segunda colocação, com oito operações, em queda de 20%, enquanto o segmento Distribuição e Varejo cresceu 17% e fechou o mês com sete operações. O subsetor de Internet foi outro que fechou em queda de 14%, para seis transações.

No âmbito inbound, em que empresas estrangeiras investiram em companhias baseadas no Brasil, os norte-americanos seguem como os principais investidores estrangeiros no mercado nacional. Nesse início de ano, as empresas norte-americanas realizaram seis aquisições no país, metade das operações de janeiro de 2018, em um total de 150 milhões de reais em investimentos. Destas, duas foram no setor de Tecnologia e duas no segmento de Telecomunicações.

Em termos de valores aportados, destaque para a venda pela Enel Green Power Brasil Participações, braço de energia renovável do grupo italiano Enel no Brasil, de três usinas renováveis para a chinesa CGN Energy International Holdings, por cerca de 2,9 bilhões de reais. Foi a única operação da China no país no mês.

No caminho inverso, as empresas brasileiras realizaram três aquisições no mercado externo, tendo como alvos duas companhias nos Estados Unidos e uma na Costa Rica.

Private Equity e Venture Capital

Se 2018 fechou com os fundos de Private Equity e Venture Capital investindo alto no mercado nacional, o mesmo entusiasmo não se traduziu em investimentos em janeiro, especialmente por parte dos fundos estrangeiros, que realizaram apenas duas operações no país no mês.

As operações de private equity registradas no Brasil em janeiro sofreram uma queda 67% no número de deals – foram apenas dois, enquanto o volume financeiro registrado, oito milhões de reais, ficou muito abaixo do que o anotado no mês homólogo do ano anterior, aproximadamente 2,9 bilhões de reais.

Nem os investimentos de Capital de Risco conseguiu trazer a tendência de crescimento do ano anterior para 2019. As cinco operações registradas no TTR, 72% abaixo mesmo período de 2018, revelaram valores que somam 107,2 milhões de reais, total 80% inferior aos 524,6 milhões investidos no ano passado, e também abaixo dos resultados de 2017, quando foram aportados 366,9 milhões de reais.

A última etapa da operação foi realizada neste mês, após a Suzano efetuar o pagamento de 27,8 bilhões de reais aos acionistas da Fibria, que se tornam acionistas da Suzano, nova marca da empresa. Segundo a Suzano, a nova companhia nasce com capacidade de produção de 11 milhões de toneladas de celulose de mercado e de 1,4 milhão de toneladas de papel por ano.

A Suzano foi assessorada na operação pelos escritórios Cescon, Barrieu Flesch & Barreto Advogados e BMA – Barbosa Müssnich Aragão, e também recebeu assessoria do Banco Itaú BBA, Riza Capital, Banco Bradesco BBI e Bank of America. Por seu lado, a Fibria contou com a atuação de Mattos Filho, Veiga Filho, Marrey Jr. e Quiroga Advogados e Ulhôa Canto, Rezende e Guerra – Advogados. TozziniFreire Advogados e Morgan Stanley assessoraram os vendedores.

Rankings

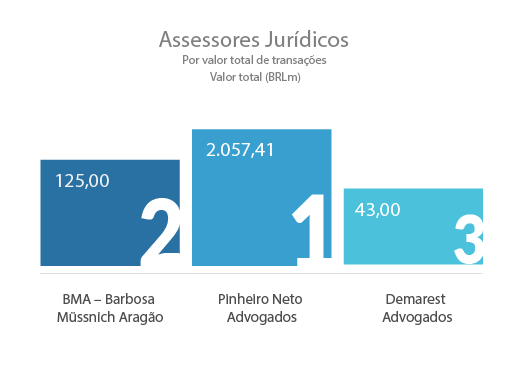

Pinheiro Neto Advogados entra 2019 na liderança do Ranking TTR dos Assessores Jurídicos, com a marca de 2 bilhões de reais transacionados. Na sequência aparecem BMA – Barbosa Müssnich Aragão, com 125 milhões de reais, e Demarest Advogados, 43 milhões de reais.

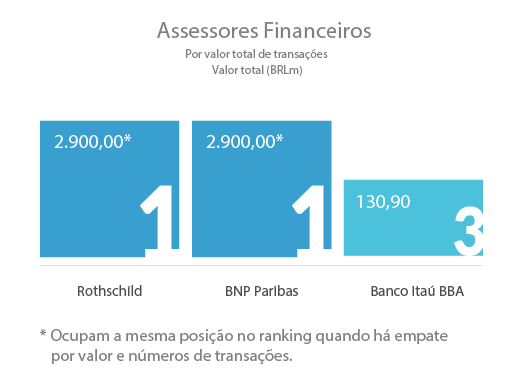

Já o ranking dos Assessores Financeiros é inaugurado com um empate entre BNP Paribas e Rothschild, ambos com 2,9 bilhões contabilizados cada, seguidos por Banco Itaú BBA, com 130,9 milhões de reais contabilizados.

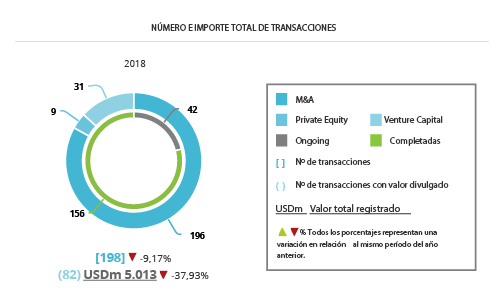

Fusiones y Adquisiciones en Argentina registran198 operaciones en 2018

En el cuarto trimestre se han registrado 41 transacciones en el país por USD 618m

82operaciones registradas en el año alcanzan un importe de USD 5.013m

Sector Financiero y de Seguros es el más destacado del año, con 36 operaciones

El mercado de M&A en Argentina ha registrado hasta diciembre de 2018 un total de 198 operaciones, de las cuales 82 tienen un importe no confidencial que suman aproximadamente USD 5.013m, según el más reciente informe de Transactional Track Record. Estas cifras suponen una disminución del 9,17% en el número de operaciones y del 37,93% en el importe de las mismas, con respecto a las cifras de 2017.

Por su parte, en el cuarto trimestre del año se han producido un total de 41 transacciones, de las cuales 16 registran un importe conjunto de USD 618m, lo que implica un descenso del 19,61% en el número de operaciones y del 85,53% en el importe de las mismas, con respecto al cuarto trimestre del año pasado.

De las operaciones contabilizadas de enero a diciembre, 69 son de mercado bajo (importes inferiores a USD 100m), 11 de mercado medio (entre USD 100m y USD 500m) y 2 de mercado alto (mayores de USD 500m).

En términos sectoriales, el Financiero y de Seguros es el que más transacciones ha contabilizado a lo largo de 2018, con un total de 36 operaciones, seguido por el sector de Distribución y Retail, con 24 operaciones, junto con el Inmobiliario, con 23 transacciones.

Ámbito Cross-Border

Por lo que respecta al mercado Cross-Border, en lo que va de año las empresas argentinas han apostado principalmente por invertir en Brasil y Chile, con 7 y 5 operaciones en cada país, respectivamente. Por importe, destaca Arabia Saudí, con USD 144m.

Por otro lado, Estados Unidos (19 operaciones), Brasil (10), México (8) y Reino Unido (6), son también los países que más han apostado por realizar adquisiciones en Argentina. Por importe destaca Brasil, con USD 1.248,79 m.

Venture Capital

En transcurso de 2018 se han producido 31 operaciones de Venture Capital, con un importe revelado de USD 250,79m, las cuales representan un aumento del 41% en el número de operaciones y un crecimiento del 31% en el importe, con respecto a diciembre de 2017

La operación, valorada en USD 126,30m, ha estado asesorada por la parte legal por Pérez Alati Grondona Benites & Arntsen, Bazán, Cambré & Orts, y Eppens & Coppola – Abogados Consultores.

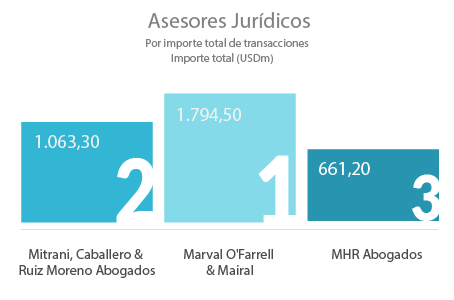

En el ranking argentino de asesores jurídicos en el segmento de Fusiones y Adquisiciones, Marval O’Farrell & Mairal ha ocupado el primer lugar por capital movilizado y por número de transacciones asesoradas, con 14 transacciones y con USD 1.794,50m.

Informe Trimestral Perú – 4T 2018

Posted on

Capital movilizado en el mercado M&A de Perú aumenta un 85% en 2018

A lo largo del año se han registrado 155 operaciones y un importe de USD 9.133m

En el trimestre se han registrado 35 operaciones con un importe de USD 2.164m

El sector Financiero y de Seguros lidera el mercado transaccional en 2018

El mercado de M&A en Perú ha registrado en 2018 un total de 155 operaciones, de las cuales 78 tienen un importe no confidencial que suman aproximadamente USD 9.133m, según el más reciente informe de Transactional Track Record. Estas cifras suponen un aumento del 1,97% en el número de operaciones y un alza del 85% en el importe de las mismas, con respecto a las cifras de 2017.

Por su parte, en el cuarto trimestre del año se han producido un total de 35 transacciones, de las cuales 15 registran un importe conjunto de USD 2.164m, lo que implica un descenso del 14,63% en el número de operaciones y una baja del 22,27% en el importe de las mismas, con respecto al cuarto trimestre del año anterior.

De las operaciones contabilizadas de enero a diciembre, 58 son de mercado bajo (importes inferiores a USD 100m) y 14 de mercado medio (entre USD 100m y USD 500m), y 6 de mercado alto (superior a USD 500m).

En términos sectoriales, el subsector Financiero y de Seguros es el que más transacciones ha contabilizado a lo largo de 2018, con un total de 17 operaciones cada uno, seguidos por el Minero, con 14 operaciones.

Ámbito Cross-Border

Por lo que respecta al mercado Cross-Border, en el año las empresas peruanas han apostado principalmente por invertir en Colombia, con 6 operaciones, seguido de Bolivia y Chile, con 3 transacciones en cada sector.

Por otro lado, Estados Unidos y Chile, con 13 operaciones en cada país, son las regiones que más han apostado por realizar adquisiciones en Perú. Por importe destaca Estados Unidos, con USD 2.368,75m.

PrivateEquity y Venture Capital

En el transcurso de 2018, Perú ha registrado 10 operaciones de PrivateEquity, de las cuales 3 registran un importe conjunto de USD 1.090,77m, lo que representa un aumento del 100% en el número de operaciones, así como un aumento del 859% en el capital movilizado con respecto a diciembre de 2017.

En cuanto al segmento de Venture Capital, Perú ha registrado 11 operaciones en 2018, de las cuales 6 contabilizan un importe conjunto de USD 17,13m, lo que representa un aumento del 83% en el número de operaciones y un aumento del 774% en el importe de las mismas con respecto al año anterior.

En el ranking peruano de asesores jurídicos en el segmento de Fusiones y Adquisiciones, Estudio Muñiz ha ocupado el primer lugar por número de transacciones y por importe de las mismas, con 24 operaciones y con un capital movilizado de USD 3.168,32m, respectivamente.

DealMaker Q&A

Posted on

TTR DealMaker Q&A with Pérez Alati Grondona Benites & Arntsen Partner Eugenio Aramburu

Deal Summary:

On 2 November, PeCom Servicios Energía, a subsidiary of Argentine conglomerate Pérez Companc Family Group, closed the acquisition of pump and petrochemicals manufacturer Bolland y Cia. for ARS 1.5bn (USD 126.3m). The transaction was selected by TTR as Deal of the Quarter in Argentina for 4Q18. The deal follows the USD 98m acquisition of PeCom Servicios Energía in 2015 by the family-owned holding, marking the group’s reentry into the oil and gas business and the subsequent acquisition of Tel3 closed in August. The group had previously exited its energy holdings with the USD 1.1bn sale of Petrolera Pérez Companc to Petrobras in 2002.

EA: We’ve been working with the Pérez Companc

Family Group for a little more than a year-and-a-half. They knew of us through

a few other deals, including the sale of the family oil business to Petrobras

in 2002, when we represented the buyer. We also represented BRF when it bought

a number of brands from the family’s food business, Molinos Río de la Plata, in

2015. They had a chance to interact with us at the time and selected us because

we were one of the bigger firms in Argentina providing comprehensive legal

services and they liked how we worked.

TTR:

How did this deal come about?

EA: Pecom approached Bolland. Some

shareholders wanted to sell, some did not. Some were older and some had taken

equity in a recent management buy-out.

TTR:

Why was Pecom interested in expanding its holdings in Argentina’s oil and gas

industry?

EA: The Pérez Companc Family Group is

confident that the oil and gas industry is going to expand and they wanted to

expand into services they did not already offer to become a full-service

provider to the industry. Through this deal they can now offer integrated

solutions to all the operators throughout the oil and gas industry.

TTR:

Why was it a good time to invest full heartedly in this industry?

EA: Notwithstanding the international price

of oil, there is an absolute necessity from the standpoint of the Argentine

government to develop the Vaca Muerta reserves as it is one of the biggest

reserves of shale gas in the world. While development of these assets may be

slower because of international energy prices, Argentina is going to provide

incentives to develop this industry regardless. Argentina is currently

importing gas, from Venezuela and elsewhere, which will become unnecessary once

these reserves enter production. All these reasons motivated Pecom to have a bigger

presence in the gas industry.

TTR:

How did recent political and economic reforms in Argentina set the stage for

this deal?

EA: During the Kirchner administration you

would never have seen a transaction like this. The government had intervened in

oil and gas prices and investments in the industry were basically zero. These investments

that require a long term for amortization need a stable environment. When Macri

came to power, the situation changed drastically. The government set out to

stimulate investments in the energy market, which is where there have been more

transactions. This transaction couldn’t have happened before. This is a bet on

the part of the Perez Companc Group demonstrating confidence in the Argentine

government and the industry.

TTR:

What made this transaction challenging?

EA: Bolland had a lot of individual shareholders

and they didn’t all have the same interest in the sale, so it demanded a lot of

negotiations aligning all their different interests. Secondly, it was a very significant

deal for Pecom because it implied doubling the size of the company. Thirdly,

the regional nature of the deal, with Bolland having operating companies not

only in Argentina, but in Brazil, Bolivia and Colombia, made it quite complex.

The transaction took a lot of time, especially because we had to coordinate due

diligence throughout these different countries. Also, the target was run like a

family company, so we had to work a lot with the sellers to help them develop a

data room. Then, during the negotiations, Argentina devalued the peso, which

had a business impact on the target, so that had to be negotiated as well.

TTR:

How was the transaction financed and how long did it take to close?

EA: The Perez Companc Group has available

funds to finance the deal, so we did not have to negotiate any financing

agreement. It took 10 months between execution of the non-binding offer and

closing.

TTR:

Why was the target considered a good complement to Pecom’s existing operations?

EA: Bolland produced pumps for the oil and

gas industry, while Pecom didn’t have a pump business. They also had a

chemicals business, and that was also an area in which Pecom was not present.

It was a strategic acquisition that transformed Pecom into a full services

provider.

TTR:

What became of Bolland’s minority partner in the Colombian operating company?

EA: A Colombian businessman had a 30% stake

in the Colombian subsidiary. He’s a Colombian investor who saw an opportunity

to exit, so he tried to apply pressure for the sale of his stake, and Pecom

decided it was easier not to have a minority shareholder in Colombia. At the

time of closing we negotiated a term sheet for the acquisition of his stake and

that acquisition was negotiated and consummated after closing of the first

deal. It was not a substantial amount compared to the larger deal.

TTR:

How will Pecom leverage Bolland’s interntional presence?

EA: Increasing its operations across the

region is definitely an objective for Pecom now that it has become the biggest

local player in Argentina through this transaction. Bolland had operating

subsidiaries where Pecom didn’t have any presence at all and can now look at

how to increase their market participation in these markets with their full

portfolio of products and services.

TTR:

How hard will this acquisition be for Pecom to integrate?

EA: Integration will be a big challenge for

Pecom. It’s acquiring a target that’s almost as big as itself. Though Pecom is

a family-owned company, it was run more like an international company in terms

of corporate governance and labor standards. Bolland had almost 800 employees

that will need to adjust to new policies and a different compensation scheme.

From a real estate perspective, Pecom will have to move its headquarters to a

new building that is being constructed now because the entire staff couldn’t

all fit at the existing facility. IT systems will need to be integrated too,

which is also a challenge.

TTR:

What other deals do you see on the horizon for Pecom?

EA: We are now involved in one ongoing

transaction where the group is negotiating another important acquisition

related to the energy industry. I cannot offer more details on that as a binding

agreement has yet to be signed. Suffice it to say that they’re looking to

deepen their foothold in Argentina’s oil and gas industry and this is not the

last of their investments.

TTR:

How was the valuation arrived at and how pleased were the sellers?

EA: The sellers were satisfied with the

outcome. Despite the devaluation that happened in the midst of negotiations,

the purchase price, which was denominated in dollars, was not modified.

Some of the sellers considered their stake

in Bolland as a retirement plan to see dividends forever and many didn’t want to

assume liabilities and indemnifications with the sale. The fact that the price

was good helped appease the detractors.

TTR:

Which practice areas were critical to your firm’s work on the deal?

EA: In the diligence process we had lawyers

from all fields, including oil and gas and environmental because Bolland had a

chemicals business that produced products used to enhance the productivity of

wells. The real estate practice was also important because there were assets

located in border areas, which means you have apply for special permissions with

Argentina’s Ministry of the Interior owing to security issues. Labor law also come

into play because the target had unionized employees and commercial litigation attorneys

were also heavily involved.

TTR:

What makes this deal stand out among other transactions you’ve worked on?

EA: It’s not that common for an Argentine company

to acquire a regional target. The coordination required to perform due

diligence in four countries makes it stand out. Also, In Argentina, it’s not

that common to see such large transactions, though perhaps the sum is not that

material for an international transaction. Thirdly, from a business and

psychological aspect, it was a really keystone transaction for our client. The

client was really focused and needed to take care of every detail. For all

these reasons it was a very important transaction for us and it took a lot of

time. It was also really important for the client given that it resulted in the

biggest player in Argentina.

TTR:

What does this deal say about the level of confidence in Argentina?

EA: This transaction serves as a vote of

confidence, especially at a time when the Macri administration was having some

difficulties in the face of a recession and nervousness due to inflation, with

several investors, especially international investors, delaying their

investments. The first ones that take advantage of these opportunities are

local players, eager to take a chance. They’re here for the long run. Hopefully

international investors will follow.

Subscribe to our free newsletter:

This website uses cookies. By continuing to browse the site, you are agreeing to our use of cookies