Volume de fusões e aquisições encolhe 30% até julho

Estados Unidos reduziram suas aquisições em Portugal em 61%.

Volume de investimentos de Venture Capital sofre redução de 24%

Espanha continua sendo o país que mais investe em Portugal, com 19 transações

Patrocinado pelo:

O mercado transacional português registou até o mês de julho 182 transações com um valor total de EUR 10bi, segundo o relatório mensal do TTR -Transactional Track Record, o que representa um aumento de 50% do valor movimentado e uma redução de 30% no volume de negócios, em relação ao mesmo período de 2019.

Por sua vez, no mês de julho se registou um movimento de EUR 2,7bi e um volume de 18 transações de fusões e aquisições entre anunciadas e concluídas. Este aumento em relação ao número de transações de junho representa um rompimento, após uma redução consecutiva no número de operações mensal que vinha acontecendo desde fevereiro.

O setor mais ativo do ano é o Imobiliário com 51 transações até o fim de julho, aumento de 2% na comparação anual. Segue o setor de Tecnologia com 23 operações, redução de 47% em relação ao mesmo período de 2019.

Âmbito Cross-Border

Até o fim de julho, os Estados Unidos reduziram suas aquisições em Portugal em 61%. Fundos de Private Equity e Venture Capital estrangeiros também reduziram seus investimentos em Portugal em 67%. Da mesma forma, empresas estrangeiras diminuíram em 17% seus investimentos no setor de Tecnologia e Internet em Portugal, na comparação anual.

A Espanha continua sendo o país que mais investe em Portugal, com 19 transações até o fim de julho. Neste ano, França está na segunda colocação com 11 operações e Estados Unidos no terceiro lugar com nove transações. Igualmente, Espanha é o destino favorito de Portugal na hora de investir, com nove operações até o fim de julho.

Private Equity

Até julho, os fundos de Private Equity registraram EUR 1,9bi no valor transacionado, o que representa um aumento de 20% na comparação anual. Foram dez transações, diminuição de 67%.

Venture Capital

Os fundos de Venture Capital movimentaram um total de EUR 254m até julho, aumento de 52% em relação a 2019. Já as transações foram 32, representando uma redução de 24%. O setor que mais movimentou foi o de Tecnologia com 15 transações, diminuição de 44% na comparação anual. O segundo setor mais ativo foi o de Internet, com sete transações, crescimento de 17% na comparação anual.

El mercado transaccional español registra 1.080 operaciones hasta julio de 2020

En julio se han registrado 186 operaciones y un capital movilizado de EUR 7.796m

El sector Inmobiliario es el más activo del año, con 249 transacciones

En el año se registran 81 operaciones de Private Equity y 246 de Venture Capital

Patrocinado por:

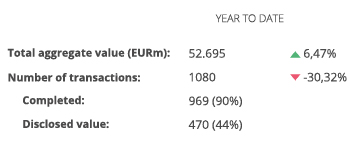

El mercado transaccional español ha registrado hasta el mes de julio un total de 1.080 operaciones con un importe agregado de EUR 52.695m, según el informe mensual de TTR , con el patrocinio de Drooms Cloud España.

Estas cifras suponen una disminución del 30,32% en el número de operaciones con respecto al mismo periodo de 2019, así como un aumento del 6,47% en el capital movilizado, debido principalmente al acuerdo de combinación de los negocios de Telefónica y Liberty en Reino Unido, operación valorada en aproximadamente EUR 22.600m.

Por su parte, en el mes de julio se han contabilizado 186 fusiones y adquisiciones, entre anunciadas y cerradas, por un importe agregado de EUR 7.796m.

En términos sectoriales, el sector Inmobiliario ha sido el más activo del año, con un total de 249 transacciones, seguido por el de Tecnología, con 189.

Ámbito Cross-Border

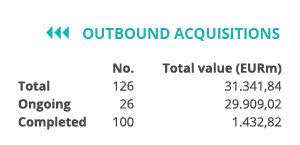

Por lo que respecta al mercado Cross-Border, hasta julio de 2020 las empresas españolas han elegido como principales destinos de inversión a Portugal y a Estados Unidos, con 19 y 12 operaciones, respectivamente. En términos de importe, Reino Unido es el país más destacado, con un valor aproximado de EUR 23.202,06m.

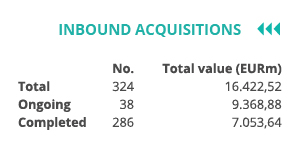

Por otro lado, Estados Unidos y Reino Unido, con 70 y 62 operaciones, respectivamente, son los países que mayor número de inversiones han realizado en España. Por importe destaca Estados Unidos, con un importe de EUR 5.288,50m.

Private Equity, Venture Capital y Asset Acquisitions

En lo que va de año se ha contabilizado un total de 81 operaciones de Private Equitypor EUR 6.318m, lo cual supone un descenso del 50,61% en el número de operaciones y del 71,08% en el importe de las mismas, respecto al mismo periodo del año anterior.

Por su parte, en el mercado de Venture Capitalse han llevado a cabo 246 transacciones con un importe agregado de EUR 3.555m, lo que implica una reducción del 16,04% en el número de operaciones y un aumento del 158,14% en el importe de las mismas, en términos interanuales.

En el segmento de Asset Acquisitions, hasta julio se han registrado 331 operaciones por un valor de EUR 9.185m, lo cual representa una disminución del 30,75% en el número de operaciones, y un descenso del 15,84% en el importe de éstas, en términos interanuales.

La operación, que ha registrado un importe de EUR 445m, ha estado asesorada por la parte legal por Bird & Bird España y por Linklaters Spain.

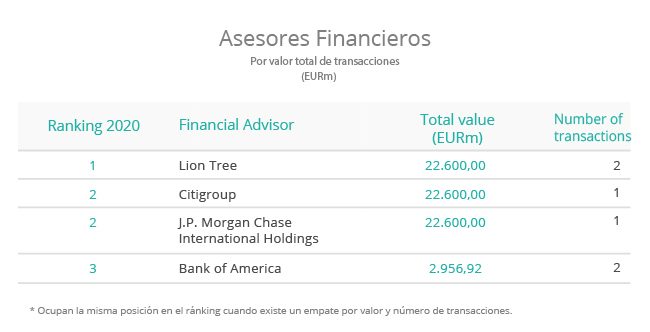

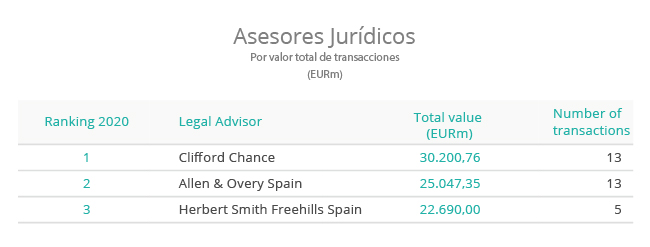

Ranking de asesores financieros y jurídicos

Transactional Impact Monitor: Spain & Portugal – Vol. 4

Posted on

Transactional Impact Monitor: Spain & Portugal – Vol. 4

31 July 2020

TTR’s Transactional Impact Monitor (TIM) is a Special Report combining local knowledge and market visibility from top dealmakers developed to address extraordinary situations affecting the macroeconomic stability and M&A outlook in core markets

Sponsored by:

INDEX

SPAIN – M&A Outlook – Capital Markets – Private Equity – Handling the Crisis

PORTUGAL – M&A Outlook – Private Equity – Handling the Crisis

– Dealmaker Profiles

SPAIN

On the cusp of Spain’s summer holiday season, the country confronts the reality that its fight against SARS-CoV-19 may be far from over. The streets of Madrid are once again full of pedestrians, who are now required to wear masks in public, as reported cases surge to levels not seen since the beginning of May. New infections are being reported mainly among younger Spaniards, however, and haven’t resulted in the same level of hospitalizations, according to the local press.

The official death toll attributed to the novel corona virus stands just shy of 45,000, while in any given year, there are nearly 500,000 deaths overall in the country. Spain’s death rate has trended upwards over the past 10 years as the country’s population ages, with both cancer and circulatory system diseases each blamed for more than 100,000 deaths annually.

Nearly half of Spain’s autonomous communities are some semblance of normal, while the other half are considered high- or medium-risk by the authorities. Those who can work remotely, continue to do so across much of the country.

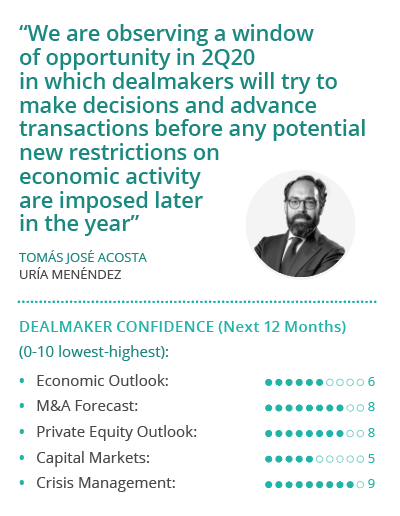

Dealmakers in the transactional market have remained incredibly busy, and the pipeline is looking robust for 2H20, sources told TTR. The workload for legal advisor Uría Menéndez has been surprisingly heavy, given the low expectations earlier in the year, despite the poor visibility about what will happen in the coming months, Partner Tomás Acosta told TTR.

Projections by the International Monetary Fund indicate a fall in global GDP of between 3% and 5%, while the Bank of Spain projects a 15% contraction in Spain, Acosta noted, but these figures too are in flux, making it difficult to predict what will happen by the close of the year.

“What I do see, and this will be key, is the need for government authorities to react decisively to avoid any major resurgence,” Acosta said, noting the new outbreaks seemed to be under control, even as reported cases escalate once again.

“We are observing a window of opportunity in 2H20 in which dealmakers will try to make decisions and advance transactions before any potential new restrictions on economic activity are imposed later in the year,” Acosta added.

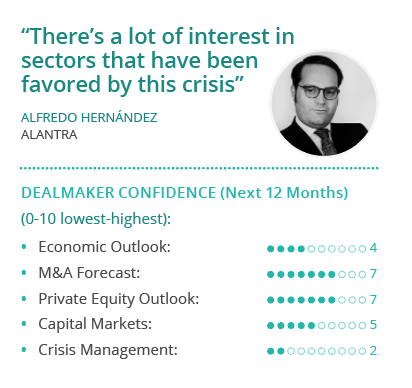

It won’t be until September or October that reality will set in, said Alantra Partner Alfredo Hernández, when companies will have three quarters of results to analyze. There will be a window between October and November to close deals, but the real boom will be in 1Q21, said Hernández. Alantra’s deal pipeline is stronger than it was at this point in 2019, Hernández said, but the type of deals has changed from overwhelmingly M&A-related to roughly half M&A and half financing transactions, he said.

When speaking with CEOs and CFOs, they are primarily concerned about their 2020 results, Hernández said. “The reality is that they still don’t know what the impact will be, though for those in the transportation and hospitality industries, the repercussions have been profound, and the impact is exceedingly clear,” he said.

There are already clear winners too, Hernández noted, citing the healthcare industry, certain consumer product segments and food production and distribution, which haven’t merely been resilient, they’ve growth by 20% to 30%. “All this has been made possible thanks to technology and communications, which have helped accelerate the existing trend of digitalization. “

Traditional retail, on the other hand, which was already suffering as e-commerce took at growing piece of the market, has been dealt a severe blow, Hernández noted. An acceleration of the migration online and away from brick and mortar among major retailers is a clear outcome of the current crisis, he said.

Portugal has registered a much lower toll from SARS-CoV-19 than its Iberian neighbor, with some 50,613 confirmed cases and 1,725 deaths attributed to the novel coronavirus. This hasn’t allowed the country to escape the devastating economic impacts associated with the pandemic threat, however, and the prospects for the economy are grim as the country enters peak summer holiday season, dealmakers told TTR.

“I am pessimistic about the economic outlook for Portugal,” said SLCM Managing Partner Luís Miguel Cortes Martins. “We are already seeing empty hotels; high-end restaurants also with very few clients. Many of them in fact reopened and then had to close again; that will generate a lot of unemployment and it will have a sharp impact on demand.”

The estimates for the Portuguese economy are not at all positive, Cortes Martins noted, and that will, in turn, drive away foreign investment. “I don’t see a V-shape recovery for the Portuguese economy,” he said.

“If Spain has a quick recovery, Portugal will be better off, since they are our main commercial partner,” he noted, and Portugal is also subject to the form the recovery will take across Europe, generally, especially in Germany. “Tourism is a main driver in our economy, and no one really knows when that will recover,” he said.

“I am somewhat pessimistic with regard to the economic outlook for 2021,” agreed EY Partner, Strategy and Transactions Miguel Farinha. “The pandemic’s economic impact will be greater than what most institutions, such as the IMF and the Bank of Portugal, are forecasting,” he cautioned. “Portugal will take a heavy blow, one which I think most people are not yet estimating correctly,” he said.

Portugal’s economy grew substantially in recent years, mostly thanks to its booming tourism sector, Farinha pointed out. Tourism typically represents about 15% of GDP in direct contributions and well over 20% including indirect contributions. The sudden flat line will bring severe economic hardship, he said.

Until a vaccine or some kind of treatment is made available, the downturn will persist, Farinha added. Notwithstanding his gloomy macroeconomic forecast, Farinha said the transactional market will be very strong, with a lot of very good acquisitions.

TTR’s Transactional Impact Monitor (TIM) is a Special Report combining local knowledge and market visibility from top dealmakers developed to address extraordinary situations affecting the macroeconomic stability and M&A outlook in core markets

Sponsored by:

INDEX

– M&A Outlook – Private Equity – Capital Markets – Handling the Crisis – Dealmaker Profiles

On 1 July 2020, the United States-Mexico-Canada Agreement (USMCA) went into effect, replacing the North American Free Trade Agreement signed in 1994. The pact reset the commercial relationship between the three North American nations and reaffirmed Mexico’s preferential trade partner status. The visit of Mexican President Andrés Manuel López Obrador, popularly known as AMLO, to Washington a week later to celebrate the signing of the accord demonstrated that the relationship between the two nations isn’t as tenuous as either leader has depicted in their rhetoric, and underscored the co-dependence that unites both countries.

In their response to the threat of a pandemic, the two leaders have exhibited a remarkably similar attitude: dismissive, contradictory and aloof. Both Mexico and the US have rapidly increased testing for Covid-19 in recent weeks, after initially limiting testing to government labs in March and April. Where the two countries have differed most in their response to the threat of pandemic, is in the release of public funds to shore up liquidity in the markets, with the US distributing trillions of dollars with little oversight or accountability, and Mexico essentially leaving the private sector to fend for itself. Concern over the impact of job losses on the economy is mounting in both countries, alongside a surge in announced Covid-19 cases that puts the US at the top of the chart, followed by Brazil, with Mexico seventh globally, according to official stats.

The outlook at the beginning of 2020 was good, there was a lot of anticipation associated with the new free trade agreement between Mexico, the US and Canada, but there was also uncertainty, said Greenberg Traurig Shareholder Arturo Pérez-Estrada. The private sector was still jarred after Mexico City’s new airport project was scrapped, but there was cautious optimism after a slow year for M&A leading up to AMLO’s election, and the transactional market had begun to stabilize, with an improving pipeline of deals.

The private sector had a tough time shaking off the jitters after AMLO’s election, agreed fellow Greenberg Traurig Shareholder Víctor Manuel Frías Garcés, as Mexico’s largest companies are accustomed to a cozy relationship with government, and it quickly became apparent that this administration wouldn’t nurture such ties.

The pipeline of new investments in the country was sparse, as foreign investors remained reserved, but companies that already had a presence in the country were sticking to their plans, Frías said. “We were facing an outlook of slow economic growth. The government’s policies were not directed towards the strata that promotes M&A,” Frías noted.

Since March, the economy has gone from slow to stagnant, overall, similar to what has happened in other markets, particularly in the US, and companies have become very conservative in the face of weak signals of support from the Mexican government, Pérez-Estrada said. The majority of companies have been reorganizing themselves and have put their expansion plans on hold, he added. “The signing of the new free trade agreement was good news, and of course there will be winners in the downturn, from e-commerce to last-mile logistics and manufacturers of health and cleaning products, but almost everybody else is facing obstacles and preserving cash,” Pérez-Estrada said.

TTR’s Transactional Impact Monitor (TIM) is a Special Report combining local knowledge and market visibility from top dealmakers developed to address extraordinary situations affecting the macroeconomic stability and M&A outlook in core markets

INDEX – M&A Outlook – Private Equity – Capital Markets – Handling the Crisis – Dealmaker Profiles

Three months after Brazil began to implement its patchwork response to the SARS-CoV-2 threat, dealmakers report widely varying levels of confidence in the strength of an economic recovery as the first half of 2020 draws to a close.

Despite the monumental level of public spending, Brazil has not yet been able to control the spread of SARS-CoV-2 and the death toll continues to mount, noted Lefosse Advogados Partner Carlos Mello.

It’s been three months since Brazilians were encouraged to self-quarantine, some under more strict guidelines than others, depending on the measures deemed appropriate by state governors, who took the health threat more or less seriously, depending on their individual assessment of the risk and their political alignment with President Jair Bolsonaro.

The authorities allowed many non-essential businesses to continue operating, including industrial production in São Paulo, Mello noted, which could have contributed to a delay in the number of reported Covid-19 cases tapering off.

Social distancing guidelines could be in effect in Brazil until September, and that will naturally create difficulties for the Brazilian market, said Mello, noting the real economy will suffer for a long time.

We are still in uncharted territory, noted veteran investor and CIO of GOW Capital, João Tourinho, but Brazil is well positioned for a quick rebound thanks to the private savings accumulated over the past four years, that were channeled to corporates seeking capital, whether via the debt or equity capital markets. These savings, he said, have provided unprecedented levels of liquidity to the market, while financial technology has served as an efficient vector, making funding readily available and affordable to credit worthy enterprises. Combined, these factors represent a disruptive force, transforming the way business is carried out in Brazil, Tourinho said.

There is a clear split between the performance of companies that meet the basic needs of society, on the one hand, and those whose products fall under discretionary spending, according to Vinci Partners Head of Financial Advisory Felipe Bittencourt. Consolidation is very likely in those sectors suffering the most, including tourism, aviation, the auto industry, manufacturing and education, Bittencourt said.

Sectors that continue to perform well, meanwhile, include healthcare, services, food, cleaning products, e-commerce and agriculture, Bittencourt said. Deals in these sectors have been proceeding with minimal disruption, he noted.

Vinci closed two transactions following the mid-March lockdown in Brazil, with a third deal reaching an exclusive phase, he said. In the first deal, Vinci was advising a seller of a financial services company, and there was no need to renegotiate terms, he said. In the second deal, Vinci was advising the buyer and the deal value was renegotiated, he added. In the transaction pending close, Vinci is advising the seller in the sale of a construction materials company to a strategic buyer based in the EU. The seller has a specific use in mind for the cash and will exit the business completely, otherwise it wouldn’t have been a good time to sell, he said.

“As advisors we take a conservative approach, we do a lot of technical analysis,” Bittencourt said. “In a period like this, you run different scenarios, the negotiations take a long time.” For those sectors that are suffering, more analysis is required as there’s more risk involved in an acquisition, especially on the buy side, he said. Vinci has other deals underway in the healthcare space, financial services, cleaning products, tourism, automotive and manufacturing, he noted.

Vinci is fielding calls related to new deal origination that can be split into two groups, Bittencourt said. On the one hand, local companies are studying partnerships, acquisitions and mergers to gain efficiencies and resolve capital structure weaknesses, he said. The economic fallout from measures imposed to mitigate the SARS-CoV-2 threat has accelerated these types of discussions, he said.

On the other hand, Vinci is fielding interest from international investors that have been looking at opportunities in Brazil for a long time and consider the currency depreciation advantageous, he said. “They believe it’s a good time to buy assets here for a decent price,” he said, noting those initiatives represented a confluence of the long-term view of these international investors and a situational opportunity.

All the firm’s non-strategic mandates with international financial sponsors, on the other hand, have been put on ice, he said. “They’ve frozen their operations in Brazil.”

Local private equity players, including Vinci’s own fund manager, remain active, however, he said. Local funds have been looking at opportunistic acquisitions while reviewing their own portfolios throughout the crisis, he said.