Content available in English and Spanish (scroll down)

TTR DealMaker Q&A with Gómez-Acebo & Pombo España Patner Íñigo Erlaiz Cotelo

Íñigo Erlaiz Cotelo – Gómez-Acebo & Pombo Spain

Head of Corporate and Commercial and head of Private Equity.

He obtained a Degree in Law and Diploma in Corporate Legal Consulting magna cum laude from the Universidad Pontificia de Comillas (ICADE) in 1999. He obtained his Diploma in Bankruptcy Law from the Madrid Bar Association in 2004. Master’s degree in Human Resources Management.

He joined Gómez-Acebo & Pombo in 1999. In 2008 he worked as a foreign associate with Debevoise & Plimpton. Secretary and member of the Board of Directors of Gómez-Acebo & Pombo.

TTR: What’s your outlook for the M&A market in the aftermath of the current crisis? What were the most notable trends in 2020?

I. E.: It has been a complex year. The uncertainty generated by the pandemic paralysed investment activity for a while. In the most affected sectors, some projects were abandoned. But in the most resilient sectors, the appearance of the vaccine and the greater visibility on the evolution of the disease allowed for a quick recovery of investments. In some more affected sectors in 2020 there were rescue financing transactions which, along with ICO injections, gave breathing room to a lot of companies. Thus, activity has been varied and erratic and has required flexibility and versatility from the teams to be able to respond to the different situations that our clients have experienced. Thanks partly to the ability of our M&A practice to adapt, 2020 was a good year for us, despite the difficult circumstances, with turn over growth at around 10%, well above average in market. This is something that, bearing in mind that the statistics note a more than 20% decline in transactional activity, makes us feel very proud, strong and confident going into 2021.

TTR: In 4Q20, the number of transactions returned to “prepandemic” values, with a total of 639 deals. How do you interpret this upward trend with respect 2Q20 and 3Q20? What is your outlook for 1Q21 in terms of deal volume in Spain?

I. E.: Before the pandemic, there was a lot of liquidity in the market. After the first hit and as visibility increased, overall in 4T with the vaccine push, that money began to work, chiefly in growth investments and deals in the less-affected sectors (healthcare, technology, food), but also in more opportunistic transactions and turnaround in the most stressed-sectors (industrial, hospitality). This trend will continue in 2021.

TTR: Regarding corporate restructuring, what was the situation in 2020 and what are the prospects for 2021 in Spain?

I. E.: Once the possible immediate effects of the pandemic on the balance sheets were assessed, some businesses began restructuring processes, both corporate restructurings and reorganisation of businesses seeking efficiencies, synergies or preparing some units for sale, and also debt restructuring processes. Regarding corporate restructurings, at the Firm, we have participated in company merger or spinoff processes, including various listed companies, for a value of more than 15 billion euros. The breathing room from the ICO financing has allowed some companies to gain time, but in many cases, they will have to wind up tackling these processes, once they have visibility on the final impact of the situation on their balance sheets and on their business plans. Thus, we expect that this restructuring activity will continue and even intensify in 2021. Our restructuring team is already working on many of these processes in which SEPI, who we are advising for example on the restructuring of Duro Felguera, is going to have a key role.

TTR: Gómez-Acebo & Pombo was one of the leading advisors on technology deals in Spain in 2020. What is the reason for the growth of this sector and what factors will drive consolidation in the space in 2021?

I. E.: For some years now we have supported building a team specialised in technology transactions that advises both VC and PE funds, and companies at different stages. The market and the type of transaction in Spain have evolved a lot. So, the size of deals we are advising on is increasing as is the sophistication of such transactions, with very relevant international investors attracted by companies with high potential. We already have advised in various transactions in this sector which have exceeded one billion in deal value. We have a leading practice in the market, a very experienced team which Alex Pujol has recently joined, who is another standout top tier lawyer in the sector. For us it is a clear strategic sector of the future, so we are wagering on it. In a world where globalisation and economies of scale are encountering various sorts of limits, technology has become a necessary asset to overcome them as well an essential element to generate value in itself. This explains investor interest in the technology sector, which will undoubtedly continue in 2021.

TTR: What have been the greatest achievements in the 50-year history of Gómez-Acebo & Pombo with respect to the firm’s transactional market? What will be the main challenges for law firms that advise on M&A deals in Spain in 2021?

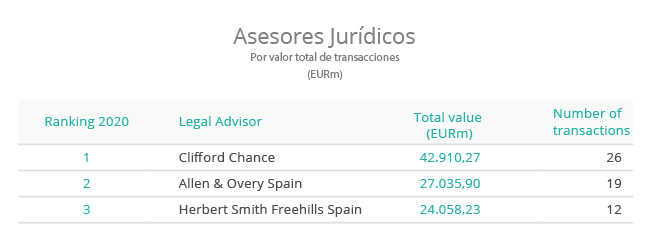

I. E.: Over the last 50 years, Gómez-Acebo & Pombo has cemented itself, despite being a smaller firm than the others, as one of the four leading Spanish independent law firms. This is essentially due to our business focus, which is very oriented toward high added-value advising and a type of client that has allowed us to participate from the beginning on large transactions in Spain and Portugal and to consolidate this leading position. Over the last few years, we have also pushed our transaction practice heavily, which has grown both in size (with an invoicing increase of around 40% over the last four years) as well as in position, as is reflected in our top-ten TTR ranking, both in the number of deals as well as in the value advised on. This position, in which we find ourselves together with much larger firms, I think says a lot about the quality of our practice. Our aim is to continue working along these lines, constantly improving and to be the point of reference for transactional matters on the Iberian peninsula. Regarding challenges for 2021, I think the main challenge will be to continue to have a versatile and broad structure of specialists that allows us to cover transactional activity which will continue to be varied, in which normal investment exists alongside distress. The specialised knowledge and sector knowledge, very important in some sectors (technology, insurance, hotels, healthcare, energy and regulated sectors) will continue to make the difference.

Spanish version

Íñigo Erlaiz Cotelo – Gómez-Acebo & Pombo España

Coordinador de Mercantil y coordinador de Capital Privado.

Licenciado en Derecho y diplomado en Asesoría Legal de Empresas, con matrícula de honor, por la Universidad Pontificia de Comillas (ICADE), 1999. Máster en Dirección de Recursos Humanos, UNED.

Diplomado en Derecho Concursal (Ilustre Colegio de Abogados de Madrid) en el 2004.

Se incorporó a Gómez-Acebo & Pombo en 1999. Foreign associate en Debevoise & Plimpton (oficina de Nueva York) en el 2008. Secretario y Miembro del Consejo de Administración de Gómez-Acebo & Pombo.

TTR: ¿Que pronóstico tiene para el mercado de fusiones y adquisiciones después de la crisis actual? ¿Cuáles fueron las tendencias más notables en 2020?

I. E.: Ha sido un año complejo. La incertidumbre generada por la pandemia paralizó la actividad inversora durante un tiempo. En los sectores más afectados se abortaron algunos proyectos. Pero en los más resilientes, la aparición de la vacuna y la mayor visibilidad sobre la evolución de la enfermedad, permitieron reactivar pronto las inversiones. En algunos de los sectores más afectados ha habido en 2020 operaciones de rescue financing que, junto con las inyecciones ICO han dado oxígeno a muchas compañías. La actividad, por tanto, ha sido variada y arrítmica, y ha requerido de flexibilidad y versatilidad en los equipos para poder dar respuestas a las distintas situaciones que han vivido nuestros clientes. Gracias en parte a esa capacidad de adaptación nuestra práctica de M&A se ha comportado muy bien en 2020, a pesar de ese difícil contexto, con un crecimiento cercano al 10% de facturación, muy por encima del mercado. Algo que, teniendo en cuenta que las estadísticas apuntan un descenso superior al 20% de la actividad transaccional, nos hace sentirnos orgullosos y fuertes y confiados de cara al 2021.

TTR: En el cuarto trimestre de 2020, el número de transacciones ha vuelto a los valores de la ‘prepandemia’, con un total de 639 deals. ¿Cómo interpreta esta tendencia al alza con respecto al segundo y tercer trimestre del año?, ¿Que perspectiva tiene para el primer trimestre de 2021 en cuanto al volumen de transacciones en España?

I. E.: Antes de la pandemia había mucha liquidez en el mercado, Ese dinero quedó embalsado durante los primeros meses. Superado el primer golpe y conforme se iba ganando en visibilidad, y sobre todo en el 4T con el empuje de la vacuna, ese dinero se puso a funcionar, principalmente en compras e inversiones de growth en los sectores menos afectados (salud, tecnología, alimentación), pero también en operaciones más oportunistas y de turn around en los sectores más estresados (industrial, hospitality). Esta tendencia continuará en 2021.

TTR: En cuanto a reestructuraciones societarias, ¿cuál fue la situación en 2020 y cuáles son las perspectivas para 2021 en España?

I. E.: Una vez calibrados los posibles efectos inmediatos de la pandemia en los balances, algunos negocios han iniciados procesos de restructuración, tanto societaria y de reorganización de negocios buscando eficiencias, sinergias o preparando algunas unidades para la venta, como de restructuración del pasivo. En cuanto a las restructuraciones societarias desde el Despacho hemos participado en procesos de fsuiones o escisiones de comapñías, inclyuyendo varias cotizadas, por valor de más de 15 mil millones de euros. El oxígeno de las ayudas ICO ha permitido algunas compañías ganar tiempo pero, en muchos casos, tendrán que acabar acometer igualmente esos procesos, una vez que tengan visibilidad del impacto final de la situación en sus balances y en sus planes de negocio. Por tanto esperamos que esa actividad de restructuración continúe e incluso se intensifique en 2021. Nuestro equipo de restructuraciones está ya trabajando en varios de esos procesos en los que SEPI, a quien estamos asesorando, por ejemplo en la restructuración de Duro Felguera, va a tener también un papel clave.

TTR: Gómez-Acebo & Pombo ha sido uno de los principales asesores líderes en operaciones de tecnología en España en el último año, ¿A qué se debe el crecimiento de este sector en 2020 y cuáles serán los drivers mas relevantes para la consolidación de este sector en 2021?

I. E.: Desde hace años hemos apostado por construir un equipo especializado en transacciones con componente tecnológico, que asesora a fondos, tanto de VC como de PE, y compañías en sus distintas fases. El mercado y el tipo de operación en España ha evolucionado mucho. Así que las operaciones en las que asesora son cada vez de mayor volumen y sofisticación, con inversores muy potentes atraídos por compañías de alto potencial. Tenemos ya varias operaciones en este sector que han superado los mil millones de deal value. Tenemos una práctica líder en el mercado, a la que recientemente se ha incorporado, además, Alex Pujol, que es otro abogado estrella del sector. Y vemos claro que es un sector estratégico y de futuro, así que seguiremos apostando por ella. En un mundo donde la globalización y las economías de escala están topándose con límites de distinto orden, la tecnología se ha convertido en un activo necesario para superarlos y en un elemento esencial para generar valor en sí mismo. Eso explica el interés inversor en el sector tecnología, que continuará sin duda en 2021.

TTR: ¿Cuáles han sido los más grandes logros en los 50 años de trayectoria de Gómez-Acebo & Pombo en lo que respecta al mercado transaccional?, ¿Cuáles podrían ser los principales retos para los despachos de abogados que asesoran en operaciones de M&A en España durante 2021?

I. E.: En estos 50 años Gómez-Acebo & Pombo se ha consolidado, a pesar de tener un tamaño menor, como uno de los cuatro despachos líderes españoles. Eso ha sido esencialmente por el enfoque de negocio, muy orientado al asesoramiento de alto valor añadido y a un tipo de cliente que nos ha permitido participar desde nuestros comienzos en las grandes operaciones que se han realizado en nuestro país y consolidar esa posición de liderazgo. En los últimos años hemos dado además un gran impulso a nuestro practica transaccional, que ha crecido tanto en tamaño (con un incremento cercano al 40% de facturación en los últimos 4 años) como en posicionamiento, como reflejan nuestro ranking dentro del top ten de las tablas de TTR, tanto número de operaciones como en valor asesorado. Esa posición, en la que estamos junto con otros despachos muy superiores en tamaño creo que dice mucho de la calidad de nuestra práctica. Nuestro objetivo es seguir trabajando en esa línea de mejora constante y ser el despacho ibérico de referencia para asuntos transaccionales. En cuanto a los retos para 2021 creo que el principal seguirá siendo tener una estructura versátil y amplia de especialistas que permita dar cobertura ante una actividad transaccional que seguirá siendo variada, en la que convivirán la inversión normal con la actividad distress. El conocimiento especializado y también el sectorial, muy importante en algunos sectores (tecnológico, seguros, hotelero, health, energía y sectores regulados) seguirá marcando la diferencia.