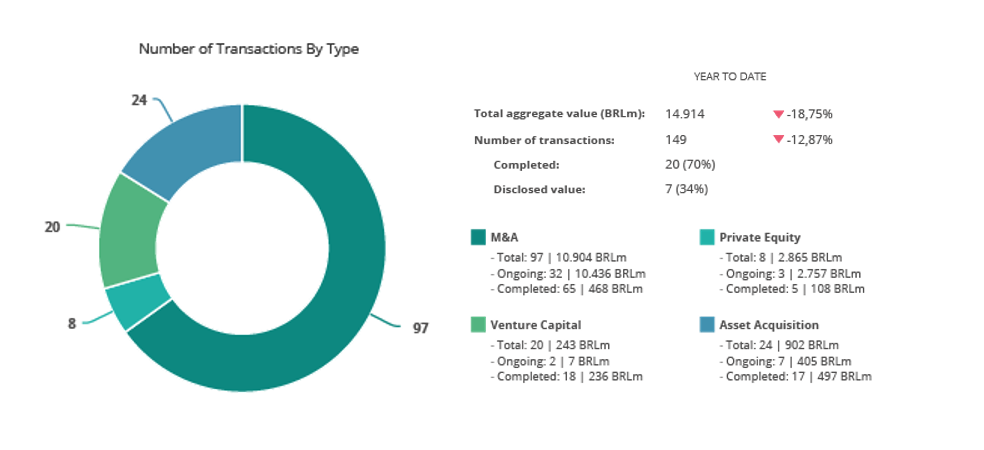

Mercado de M&A movimenta 330 milhões de euros em fevereiro

Foram registadas 48 transações desde o inicio do ano

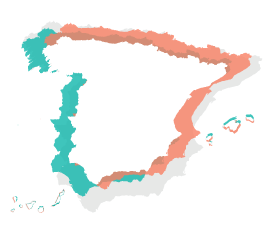

Espanha e Reino Unido são os maiores investidores no mercado nacional em 2019

De acordo com o Relatório Mensal de M&A da Transactional Track Record, os anúncios de compra e venda de participação que envolveram empresas portuguesas movimentaram 683 milhões de euros nos dois primeiros meses de 2019, queda de 53,36% ante o mesmo período do ano anterior. Nesse período foram registadas 48 operações, representativas de uma baixa de 12,7% em comparação ao reportado em igual intervalo de 2018.

O sector Imobiliário foi o de maior movimentação no primeiro bimestre, com 12 transações registadas. Tecnologia, com nove operações, e Financeiro e Seguros e Internet, com quatro deals cada, aparecem empatados na sequência.

No âmbito das operações cross-border inbound, em que empresas estrangeiras investiram em companhias baseadas em Portugal, os Espanhóis seguem como os mais ativos no mercado nacional. Entre janeiro e fevereiro foram contabilizadas dez investidas espanholas no país. Destas, dez foram aquisições no segmento Imobiliário, que somam 212 milhões de euros. Destaque também para os investimentos provenientes do Reino Unido, que em três operações injetou 171 milhões em empresas portuguesas.

No caminho inverso, as empresas portuguesas realizaram cinco aquisições no mercado externo, incluindo a entrada da Sonae IM no capital da ViSenze, empresa de Singapura que opera na área da inteligência artificial, que anunciou em fevereiro que angariou 17,69 milhões de euros numa ronda de financiamento série C.

Private Equity e Venture Capital

Na modalidade de investimentos de Venture Capital, alta de 67% no número de operações, dez, porém com baixa de 6.9% no valor agregado, 24 milhões de euros. Sete dessas operações foram anunciadas em fevereiro, com um total de 21,3 milhões de euros aportados. A Portugal Ventures esteve presente em três dessas rondas de financiamento, tendo adquirido participações nas startups Shiptmize, Logical Safety e Advertio, que irão receber 500 mil euros cada.

No segmento de Private Equity, as operações caíram 84% para 100 milhões de euros no decorrer dos dois primeiros meses em comparação com o período homólogo do ano anterior.

Transação do Mês

A transação eleita pela TTR como a de destaque do mês foi a venda da Energyco II pelo private equity espanhol Artá Capital à UBS Asset Management Funds, por 118 milhões de euros. A Energyco II é uma empresa ibérica que se dedica ao fornecimento de água quente ou de vapor a clientes empresariais.

A sociedade Cuatrecasas prestou assessoria jurídica ao fundo espanhol, que também recebeu consultoria da Haitong Bank Portugal. Por sua vez, a UBS Asset Management Funds contou com a assessoria do escritório CMS Rui Pena & Arnaut.

Ranking TTR

O Ranking TTR de Assessores Jurídicos de 2019 tem em fevereiro um empate na liderança entre CMS Rui Pena & Arnaut e Cuatrecasas Portugal, enquanto a Haitong Securities lidera o Ranking TTR de Assessores Financeiros, seguido por Crowe Horwath Portugal e Optimal nvestments, empatados na segunda colocação.

O relatório completo está disponível para download gratuito aqui.