Roberto MacLean, socio del estudio Miranda & Amado.

Abogado por la Pontifica Universidad Católica del Perú con Maestría en Derecho por la Universidad de Nueva York. Socio de Miranda & Amado desde el año 1999. Tiene amplia experiencia en diversas transacciones corporativas, financieras y de mercados de capitales, principalmente en adquisiciones, financiamiento de proyectos y proyectos de infraestructura.

Abogado por la Pontifica Universidad Católica del Perú con Maestría en Derecho por la Universidad de Nueva York. Socio de Miranda & Amado desde el año 1999. Tiene amplia experiencia en diversas transacciones corporativas, financieras y de mercados de capitales, principalmente en adquisiciones, financiamiento de proyectos y proyectos de infraestructura.

Sr. MacLean, en primer lugar ¿podría ofrecernos una valoración general en cuanto a la marcha actual del mercado de M&A en Latinoamérica en comparación con ejercicios anteriores?

Las cifras que dan los reportes de TTR a octubre parecen indicar que en cuanto a número de transacciones este podría ser igual o mayor al año anterior. Sin embargo, el valor en dólares es menor y viene bajando consistentemente en los últimos cuatro años.

Como profesional en el asesoramiento de fusiones y adquisiciones, ¿podría contarnos brevemente cuáles son los sectores que están experimentando en Perú mayores cambios en el volumen de sus transacciones y por qué?

Basados en la experiencia que hemos tenido en el estudio, los sectores más dinámicos han sido infraestructura, agricultura, el sector financiero, educación e inmobiliario. El sector de infraestructura se explica por la crisis de las constructoras brasileñas y los problemas financieros de otras dos constructoras internacionales con proyectos importantes, así como el deseo de constructoras peruanas que buscan sobreponerse a la crisis coyuntural que esto ha generado. El sector agrícola está activo debido a que Perú se ha convertido en un exportador importante de varios productos bien cotizados internacionalmente, lo cual ha generado una ola de adquisiciones y operaciones de private equity. El sector financiero, educación e inmobiliario están reflejando un reacomodo de actores.

Como experto en el asesoramiento de proyectos que requieren financiación ¿podría explicarnos, a grandes rasgos, en qué consiste el proceso de las modalidades más empleadas para la obtención de crédito?

En el caso peruano y de adquisiciones donde el adquirente es operador del negocio que ha adquirido o es un grupo empresarial consolidado, la fuente de financiamiento popular son los bonos. Cuando el adquirente es un fondo de inversión éstos tienden a recurrir primero a deuda bancaria, que luego puede ser refinanciada por una emisión de bonos por parte de la empresa adquirida.

¿Cuáles son las principales barreras o dificultades a las que se enfrentan las empresas a la hora de solicitar dichos préstamos?

Diría que la principal barrera en el caso peruano son las restricciones a la llamada asistencia financiera, que limita la capacidad de los adquirentes de utilizar los activos de la empresa adquirida para financiar la adquisición. Por esta razón, el financiamiento de adquisiciones es más sencillo cuando se adquiere una empresa al 100% (o una mayoría muy grande y con muy pocos accionistas minoritarios) y sin deuda o muy poca deuda concentrada en uno o pocos acreedores.

En relación con la pregunta anterior ¿Cree que podría realizarse algún cambio legislativo que facilitase el acceso a este financiamiento para las empresas, teniendo en cuenta las condiciones que ahora mismo existen?

Considero que en el Perú podrían eliminarse las restricciones a la asistencia financiera bajo ciertas condiciones, protegiendo a minoritarios de conflictos de intereses que puedan presentarse entre los intereses del accionista adquirente y los minoritarios. Es mejor que restringirla por completo.

Por último, ¿qué sectores destacaría usted como potenciales targets para lo que resta de 2017 en el mercado de M&A latinoamericano? ¿Por qué?

El gobierno chino parece enfocado en asegurarse la disponibilidad de diversos recursos naturales a largo plazo, esto genera que las empresas chinas estén enfocadas en adquirir activos en toda la región que ayuden a este fin. La liquidez generada en la región y en otras partes del mundo ha fomentado la creación de fondos de capital privado de toda clase y tamaño, enfocados en una gran diversidad de actividades. Por otro lado, varias empresas de nuestros países han adoptado la estrategia de convertirse en actores regionales, sumándose a las ya conocidas multilatinas en su estrategia de crecimiento regional. Todo esto genera un grupo importante de entidades que están en búsqueda de oportunidades de inversión. Por el lado de la venta están los negocios que sufren reacomodos por razones locales o regionales, como en el caso de las constructoras y las mineras. Por esto, considero que para el resto del año y el año que viene, en el caso del Perú los sectores más dinámicos podrían ser infraestructura, inmobiliario, agricultura, recursos naturales, energía, pesca, educación y salud. Mirándolo desde el radar regional, sin embargo, las transacciones más relevantes por su valor en USD serán en el sector minero, energía, infraestructura y pesca.

Para leer de las transacciones en las que Roberto MacLean ha participado, haz click aquí.

Para leer de la firma Miranda & Amado Abogados en Perú y sus transacciones, haz click aquí.

English

Mr. MacLean, first of all, could you offer us a general assessment concerning the current development of the M&A market in Latin America in comparison the previous period?

The figures that the TTR reports offers until October seem to indicate that the number of transactions could be the same or more than last year. However, the value in dollars is smaller and has been going down consistently for the last four years.

As a professional in the advice of mergers and acquisitions, could you tell us briefly what are the sectors in Peru that are showing more changes in the volume of their transactions and why?

Based on the experience that we have had in the firm, the most dynamic sectors have been infrastructure, agriculture, the financial sector, education and the real-estate sector.

The good development of the infrastructure sector is due to the crisis of Brazilian building companies and the financial problems of two others international companies with important projects, as well as the wish of the Peruvian building companies that look forward to overcoming the relevant crisis that it has generated. The agricultural sector is active because Peru has become an important exporting country of several well-valued products at international level. This situation has generated an outbreak of acquisitions and operations of private equity. The financial sector, the education sector and real-estate sector are reflecting a new adjustment of actors.

As a legal advisory expert in projects that require financing, could you explain us the process of the most usual methods for getting credit?

In the Peruvian case in acquisitions where the purchaser is operator of the business that has purchased or it’s a consolidated business group, the source of popular financing is the bonus. When the purchaser is a fund of investment, these tends to go first to banking debt, which can then be refinanced by a bond issue by the acquired company.

What are the main difficulties that companies face to when applying for such loans?

I would say that the main barrier in the case of Peru are the restrictions to the financial assistance that restrict the ability of the purchasers of using the assets of the purchased company to finance the acquisition. For this reason, financing the acquisitions is easier when a company is purchased completely at 100% (or in a very big majority and with very little minority shareholders) and without debts or very few debts condensed in one or few creditors.

Regarding the previous question, do you think that is possible to do some legislative changes to facilitate the access of this kind of financing for the companies keeping in mind the conditions which exist now?

I consider that in Peru the restrictions for financial assistance could be deleted under some conditions, protecting minorities against conflicts of interests that may appear between the interests of the purchased shareholder and minorities. This situation It’s better than restrict it completely.

Finally, what sectors would you consider as main targets for the rest of 2017 in the Latin American market of M&A? Why?

The Chinese government seems to be focus on assure the availability of different natural resources in a long-term, in consequence Chinese companies would be focused on purchasing assets in all the region that helps achieving this objective. The liquidity generated in the region and in other parts of the world has encouraged the creation of funds of private capital in every class and size, focused on a great diversity of activities. On the other hand, several companies of our countries have adopted the strategy of becoming regional actors, incorporating themselves to the great Latin-American companies with their strategy of regional growing. All of this generates an important group of entities which are in search for opportunities of investment.

On the side of the sales are the business which suffer adjustments because of local or regional reasons like building or mining companies. For this reason, I consider that by the rest of the year and for 2018, in the case of Peru, the most dynamic sectors could be: infrastructure, the real-estate, agricultural, natural resources, energy, education, health and fishing. Looking through the regional radar, however, the most important transactions due to their USD Value will be the mining sector, energy, infrastructure and fishing.

To know about Roberto MacLean and transactions he has participated in, click here.

To read about transactions of the firm Miranda & Amado Abogados in Peru, click here.

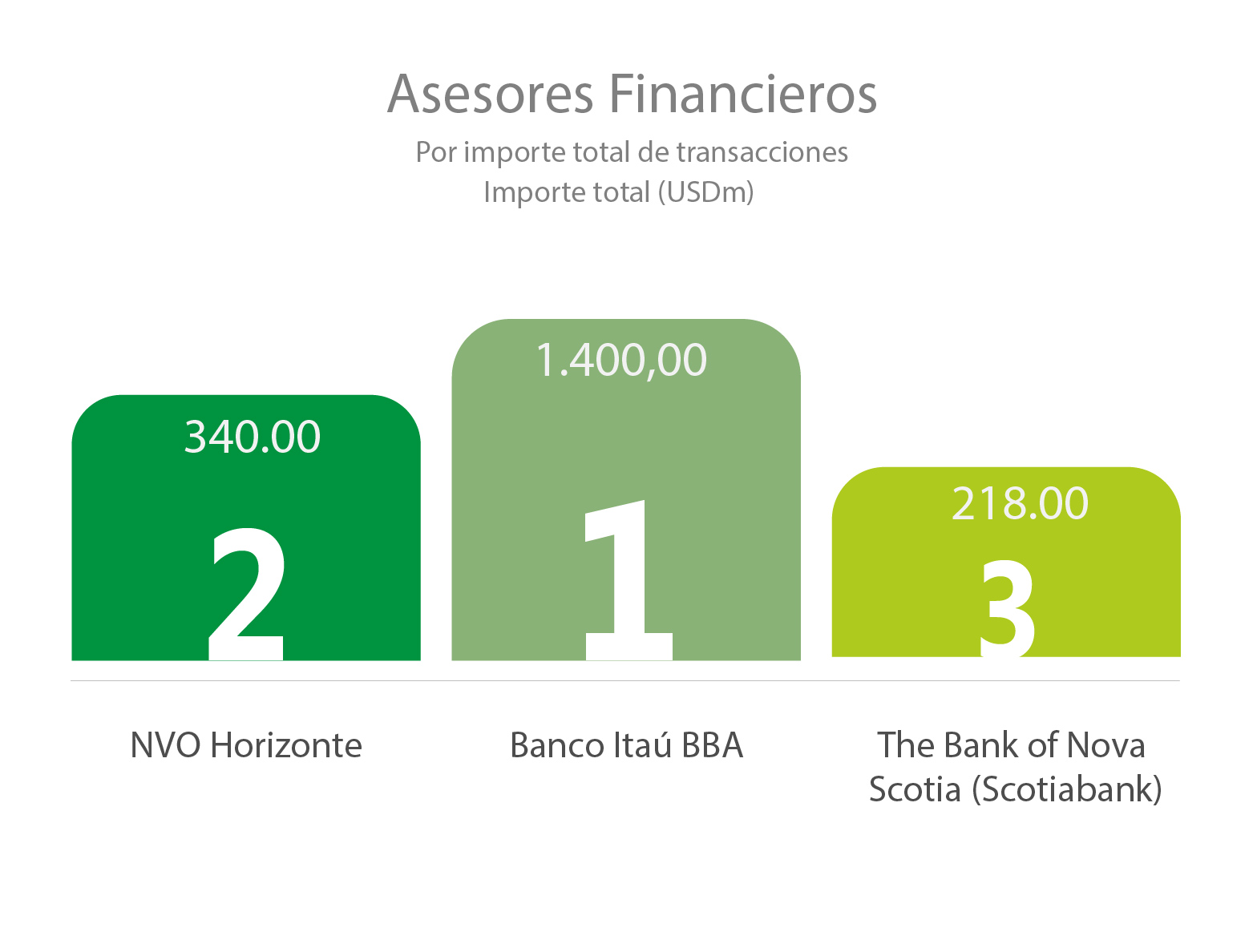

TTR selected The Mosaic Company’s USD 1.4bn acquisition of a 40% stake in Compañia Minera Miski Mayo as Deal of the Month in February. The Peru-based target mines potassium, phosphate, kaolin and potash in the region of Piura. Estudio Muñiz represented the target in the deal, which represents 41% of Peru’s aggregate transaction value YTD.

TTR selected The Mosaic Company’s USD 1.4bn acquisition of a 40% stake in Compañia Minera Miski Mayo as Deal of the Month in February. The Peru-based target mines potassium, phosphate, kaolin and potash in the region of Piura. Estudio Muñiz represented the target in the deal, which represents 41% of Peru’s aggregate transaction value YTD.