Las transacciones de M&A en México disminuyen un 23% en el primer trimestre de 2021

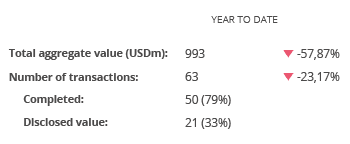

En los tres primeros meses de 2021 se han registrado 63 transacciones por USD 993m

El sector Financiero y de Seguros es el más destacado del periodo, con 20 operaciones

Operaciones de Venture Capital aumentan un 14,81% en el primer trimestre de 2021

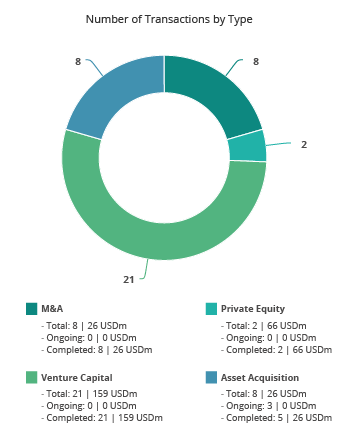

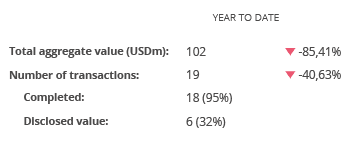

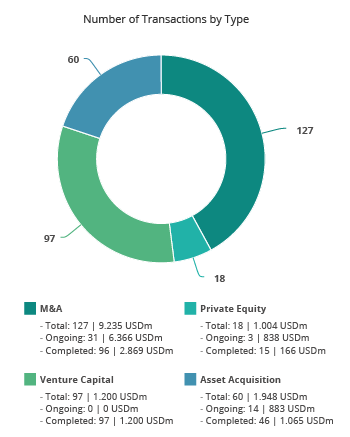

El mercado de M&A en México ha contabilizado en los tres primeros meses del año un total de 63 operaciones, de las cuales 21 suman un importe no confidencial de USD 993m, de acuerdo con el informe trimestral de Transactional Track Record. Estos datos reflejan un descenso del 23,17% en el número de operaciones y del 57,87% en el importe de las mismas con respecto al primer trimestre de 2020.

En términos sectoriales, el Financiero y de Seguros es el más activo del año, con un total de 20 transacciones, con un aumento del 33% con respecto al primer trimestre de 2020; seguido por el sector Tecnológico, con 19 operaciones y un aumento interanual del 19%, y el de Internet, que registra un aumento del 38% al registrar 11 operaciones.

Ámbito Cross-Border

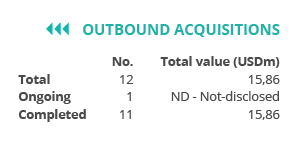

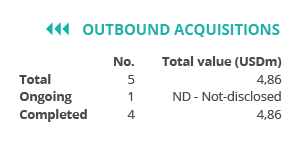

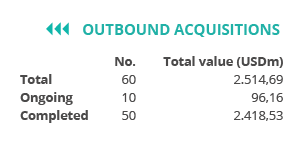

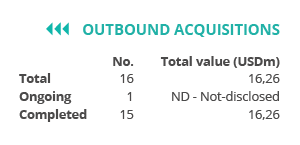

Por lo que respecta al mercado Cross-Border, en lo que va de año las empresas mexicanas han apostado principalmente por invertir en Chile, con 5 transacciones, seguido por España y Estados Unidos, con 3 operaciones en cada país. Por importe, destaca España, con USD 10,86m.

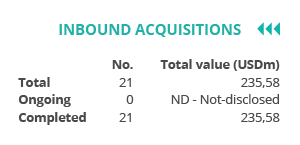

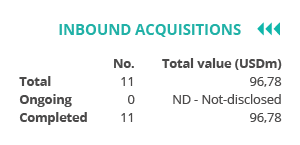

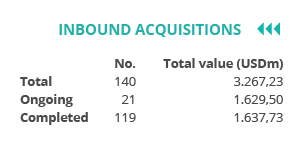

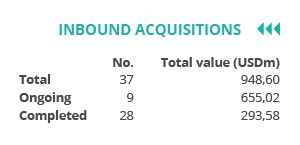

Por otro lado, Estados Unidos es el país que más ha apostado por realizar adquisiciones en México, con 21 operaciones, seguido de España con 6 operaciones. En términos de importe, destaca España con un importe de USD 657,45m.

Private Equity y Venture Capital

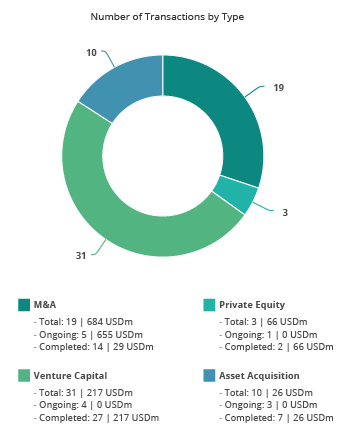

En el primer trimestre de 2021 se han producido un total de 3 transacciones de Private Equity valoradas en USD 66m, las cuales representan una disminución del 25% en el número de operaciones y un descenso del 47,76% en el capital movilizado con respecto al primer trimestre de 2020.

Por su parte, en los tres primeros meses de 2021, México ha registrado 31 operaciones de Venture Capital valoradas en USD 217m, lo que representa un aumento del 14,81% en el número de operaciones y un descenso del 29,64% en el capital movilizado con respecto al mismo periodo del año pasado.

Asset Acquisitions

En el mercado de adquisición de activos, se han cerrado en el primer trimestre 10 transacciones con un importe de USD 26m, lo cual implica un descenso del 44,44% en el número de operaciones y un descenso del 94,90% en su importe con respecto al mismo periodo de 2020.

Transacción del trimestre

Para el primer trimestre de 2021, Transactional Track Record ha seleccionado como operación destacada la relacionada con Advent International a través de su filial Advent International México, en la que ha vendido su participación en Grupo Gayosso a Servicios Funerarios GG.

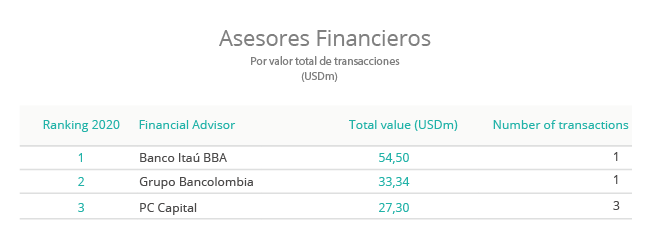

La operación, valorada en USD 54,45m, ha estado asesorada por la parte legal por Mijares, Angoitia, Cortés y Fuentes; Ritch Mueller; Sarur y por Llaguno Name y Moreno.

Ranking de asesores jurídicos