Importe de operaciones de M&A en América Latina aumenta un 3,08% en el tercer trimestre de 2019

666 operaciones registradas hasta septiembre alcanzan un importe de USD 71.297m

En el tercer trimestre del año se han registrado 522 transacciones en la región

Brasil, Colombia y Chile, países que registran aumento en capital y en transacciones

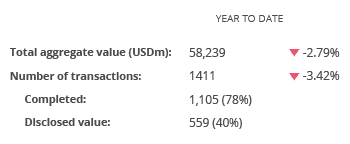

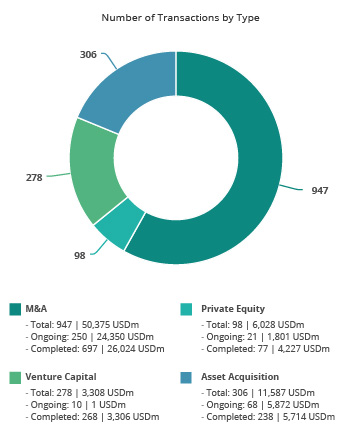

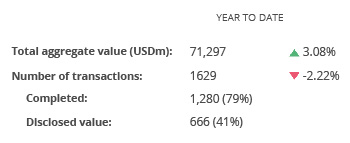

El mercado de M&A en América Latina ha contabilizado en los nueve primeros meses del año un total de 1.629 operaciones, de las cuales 666 suman un importe no confidencial de USD 71.297m, de acuerdo con el informe trimestral de Transactional Track Record.

Estos datos reflejan un aumento del 3,08% en el capital movilizado y una disminución del 2,22% en el número de operaciones, con respecto al mismo periodo de 2018.

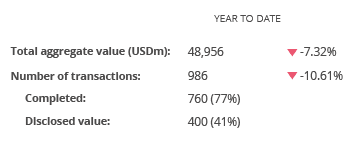

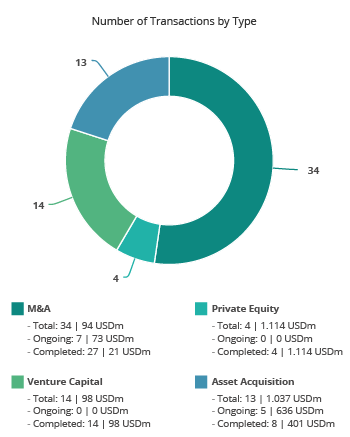

Por su parte, en el tercer trimestre de 2019 se han contabilizado un total de 522 operaciones con un importe agregado de USD 21.991,01m.

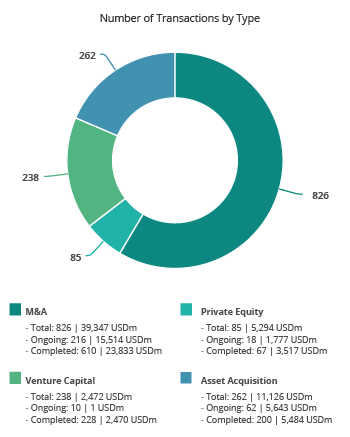

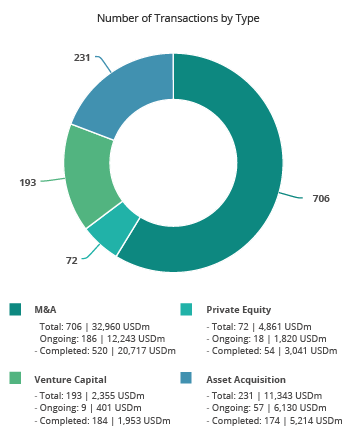

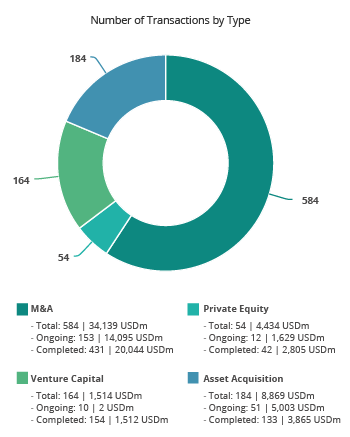

Private Equity y Venture Capital

Hasta el tercer trimestre de 2019 se han contabilizado un total de 98 operaciones de Private Equity, de las cuales 44 transacciones tienen un importe no confidencial agregado de USD 6.028m. Esto supone una disminución del 15,52% en el número de operaciones y una baja del 27,78% en el importe de las mismas con respecto al mismo periodo de 2018.

En cuanto al segmento de Venture Capital, en el semestre se han llevado a cabo 278 transacciones, de las cuales 169 operaciones tienen un importe no confidencial que suman alrededor de USD 3.308m, lo que supone un aumento del 11,65% en el número de transacciones y un crecimiento del 78,33% en el capital movilizado con respecto al mismo periodo del año pasado.

Ranking de Operaciones por Países

Hasta septiembre de 2019, por número de operaciones, Brasil lidera el ranking de países más activos de la región con 934 operaciones (aumento del 3%), y un crecimiento del 2% en el capital movilizado en términos interanuales (USD 41.171m). Le sigue en el listado México, con 216 operaciones (un descenso del 21%), y con un descenso del 16% de su importe con respecto al mismo periodo del año pasado (USD 10.247m).

Por su parte, Chile continúa en el ranking, con 179 operaciones (un aumento del 3%), además de un crecimiento del 47% en el capital movilizado (USD 8.230m). Colombia, por su parte, desplaza a Argentina en el ranking y registra 152 operaciones (aumento del 20%), con un alza del 123% en capital movilizado (USD 5.753m), lo cual se convierte, junto con México y Brasil, en uno de los países con resultados positivos, tanto en el número de operaciones, como en importe.

Entre tanto, Argentina ha descendido un puesto en el ranking, con un registro de 116 operaciones, lo cual representa un 28% menos, así como un descenso del 47% en su importe con respecto al mismo periodo del año pasado (USD 2.960m). Perú, por su parte, ha registrado 93 operaciones (una baja del 22%), con un aumento del 11% en su importe con respecto al mismo periodo del año anterior (USD 6.138m).

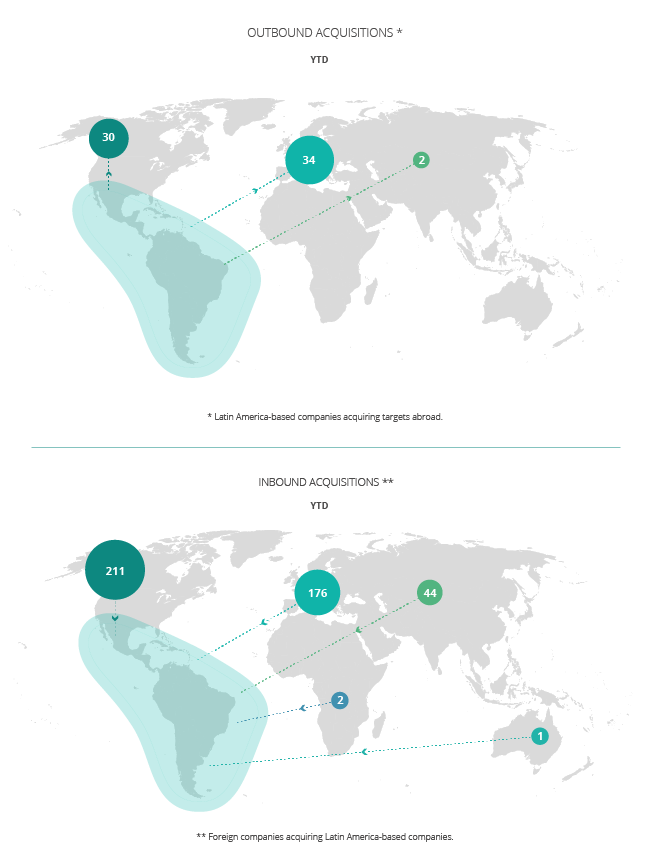

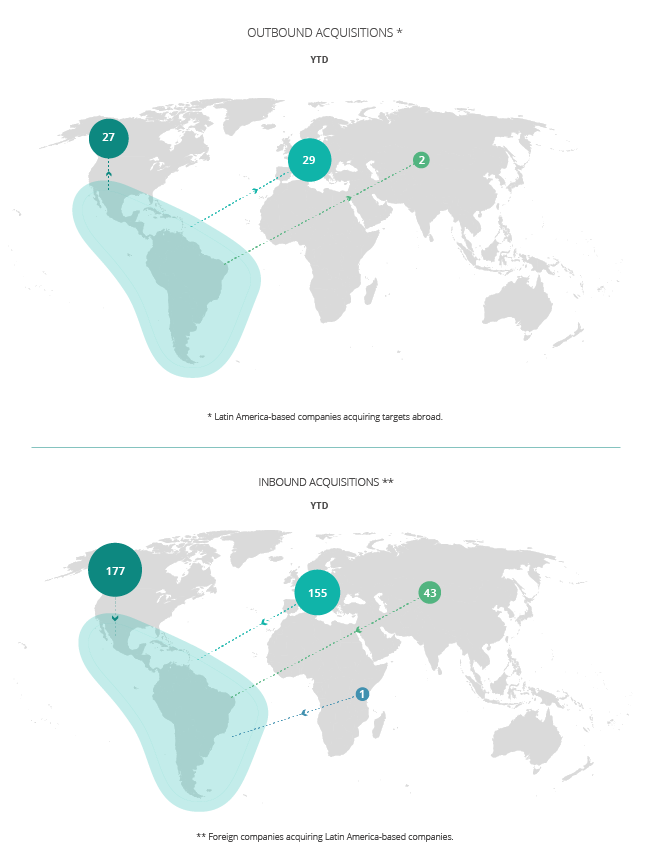

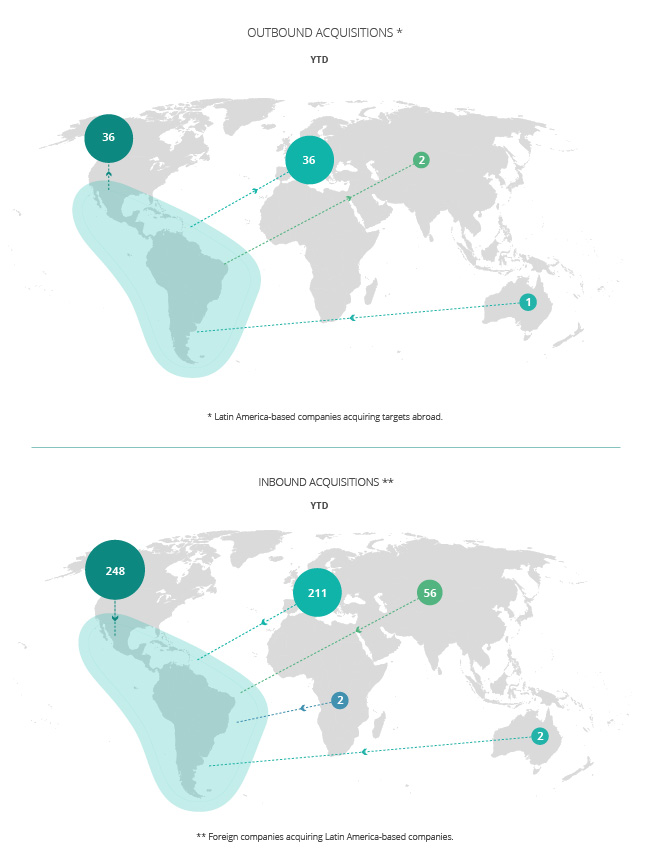

Ámbito Cross-Border

En el ámbito Cross-Border se destaca el apetito inversor de las compañías latinoamericanas en el exterior en el tercer trimestre de 2019, especialmente en Norteamérica y Europa, donde se han llevado a cabo 36 operaciones en cada región. Por su parte, las compañías que más transacciones estratégicas han realizado en América Latina proceden de Norteamérica, con 248 operaciones, Europa (211), y Asia (56).

Transacción Destacada

En el tercer trimestre de 2019, TTR ha seleccionado como transacción destacada la realizada por Carlyle Peru Fund, el cual ha adquirido Atracciones Coney Island (Coney Park).

La transacción, valorada en USD 92,30m, ha estado asesorada por la parte legal por Rebaza, Alcázar & De Las Casas; Cariola Díez Pérez-Cotapos y Payet, Rey, Cauvi, Pérez Abogados. Por la parte financiera, la operación ha estado asesorada por LXG Capital, Scotiabank Perú y The Bank of Nova Scotia (Scotiabank).

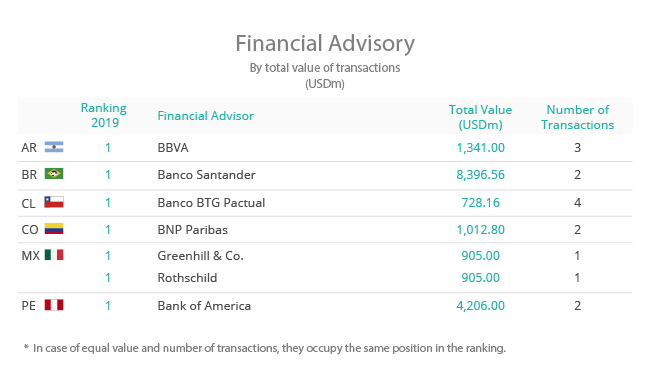

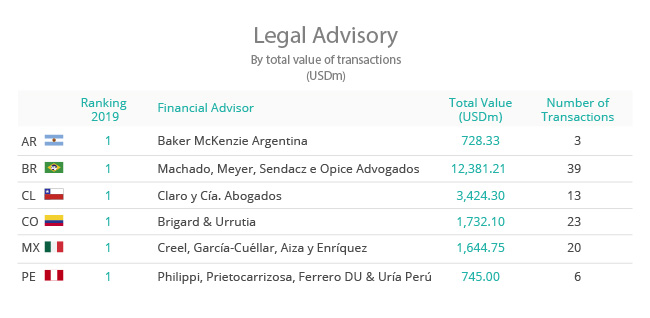

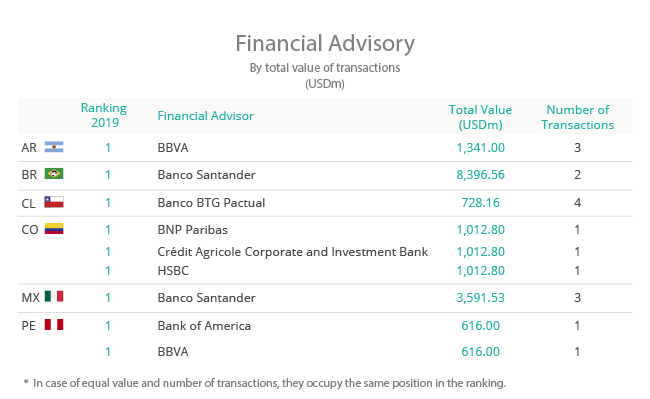

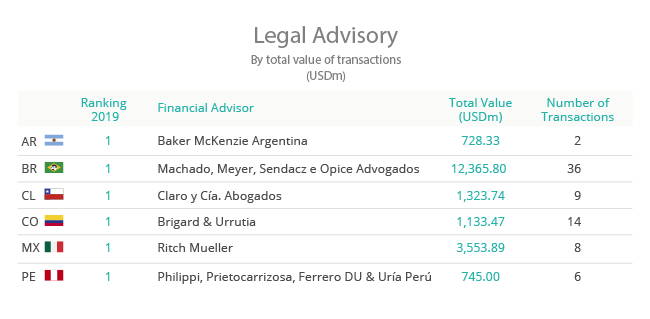

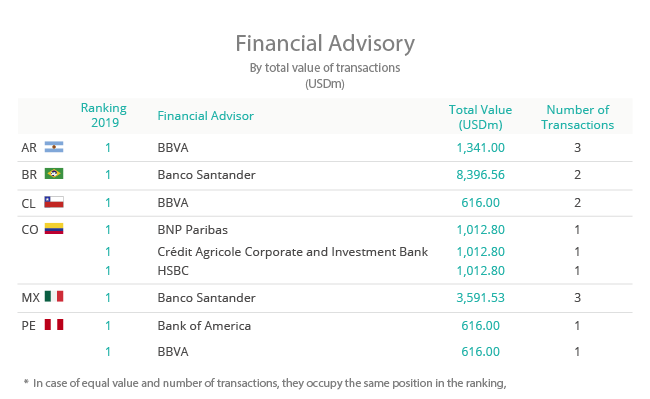

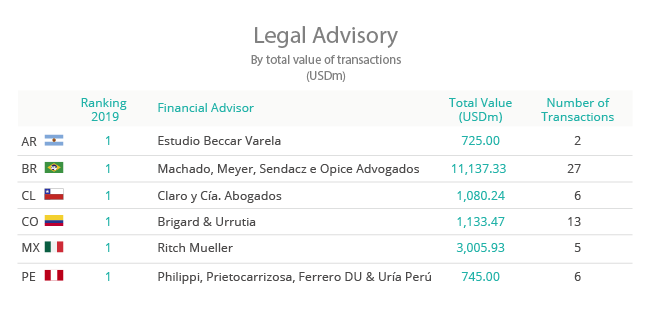

Ranking de Asesores Financieros y Jurídicos