TTR DealMaker Q&A with Bustillo Abogados Partner Javier Bustillo (in EN/ES)

Javier is a Partner of Bustillo Abogados, a boutique commercial law firm that advises startups, private companies and venture capital funds in different types of industries on mergers and acquisitions. His knowledge in this kind of operations and his previous experience in Coca-Cola and Xerox Europe allows him to offer advice in complex operations and to understand the interests of the different parties.

Javier is a Partner of Bustillo Abogados, a boutique commercial law firm that advises startups, private companies and venture capital funds in different types of industries on mergers and acquisitions. His knowledge in this kind of operations and his previous experience in Coca-Cola and Xerox Europe allows him to offer advice in complex operations and to understand the interests of the different parties.

TTR: How would you describe the transactional market in 2018? Do you consider the records to be positive?

JB: In the Mid-Market segment in which Bustillo Abogados is operating, we see a significant increase in operations with respect to previous years. This increase is mainly driven by a greater ease of financing and efforts to improve their market share as well as their geographical positioning, mainly through acquisitions in technology or innovation. After many complicated years for companies, they are now seeking to promote inorganic growth in order to strengthen their strategic positioning. It is also important to highlight the increase in the valuations of companies that are in a process of purchase since, on numerous occasions, they are presented with different purchase offers. In addition to the previously mentioned easy access to financing, this is due to an improvement in expectations of profitabilityin light of the economic recovery. However, it is difficult to say for how long this bullish trend will last.

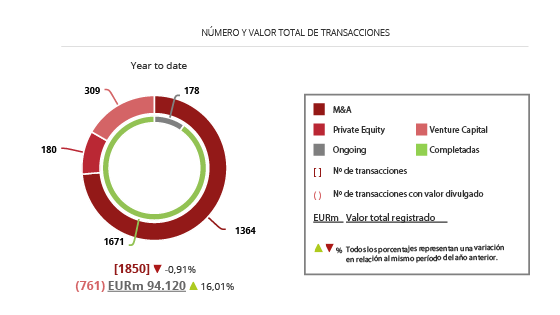

TTR: More than half of the transactions advised by Bustillo Abogados so far this year are Venture Capital transactions. Do you think that the startup universe in Spain has room for growth or have we already reached the peak?

JB: The startup universe in Spain is maturing fast although we are still behind other countries that are several years ahead of us with regards to creating new trends, innovation or know-how. We see a clear approach of large and medium-sized companies to innovation through the acquisition of startups that allow them, among other things, to incorporate innovative technology or accelerate the process of digital transformation. Although the value of the larger operations is increasing, most of them are still of a relatively moderate size compared to other European countries. However, in my view, these differences are going to reduce considering the good work being done in the technological ecosystem in Spain.

TTR: After a period of innovative ideas, would you say that we can expect more disruptive ideas or that new startups that are going to emerge will base their development on the improvement or competition of existing projects?

JB: The technology industry is constantly reinventing itself by seeking to offer innovative products and services that try to respond to the needs generated in our society as is happening now with blockchain for example. In a constantly evolving world, new ideas are emerging every day, attempting to take advantage of business opportunities and fill existing gaps in the market in different areas and sectors. In this context, many startups that are born, seek to simplify processes and jobs that nowadays are too complicated or tedious. However, we cannot forget that many of them bring us closer to realities that were previously unthinkable, such as artificial intelligence or mixed realities, generating at the same time new concerns and desires to which it is necessary to respond.This is why I am convinced that entrepreneurs still have a lot to surprise us with and to revolutionize our lives.

TTR: And from the point of view of investors, in addition to the traditional funds that have been operating in Spain for several years, the numerous Business Angels, and the commitment to Venture Capital by certain banking institutions, is there room for new market players?

JB: From my perception, Corporate Venture Capital is spreading rapidly, where companies that have had some previous experience with startups either through acquisitions, startup accelerators, incubators or others, decide to increase their commitment and establish their own investment structure. The most iconic companies in Spain have been implementing this strategy for some time already, nevertheless now there is a trend that non-listed companies are also wanting to professionalize their investments. The rapid advancement of technology and its direct impact on almost all business models we know, is forcing companies to be vigilant against possible disruptions in their industry. The establishment of a Corporate Venture Capital allows companies toanalyse, select and invest in a large number of startups that may be of interest to them, either because of a specific technology, to expand their existing portfolio of products or services or simply to improve internal work processes. At the being able to acquire only those that are really crucial for their business.

TTR: Do you think that we will see a more specialization within sectors in which these new players may arise? If large companies begin to focus more on areas of investment in Venture Capital internally, could it be the case that the investment criterion is based more on the development of a certain technology necessary for the company than on the economic profitability of the project? Could this be understood as an intermediate step between internal development of technology and outsourcing?

JB: This is precisely the point of Corporate Venture Capital, profitability is no longer seen in purely economic terms, but in many cases these investments are promoted for strategic, business, innovation or human resource reasons. A few decades ago, innovation was always born in the R&D departments of large companies due to the high volume of investment required and the long creation processes, but the lower cost and access to computers has allowed innovation to be transferred to anyone with access to internet. Therefore, companies must also change how and where they invest in order to innovate.

TTR entrevista

TTR: ¿Cómo describiría la situación del mercado transaccional en el año 2018? ¿Considera usted que los registros son positivos?

J.B.G.: En el segmento de Mid-Market en el que nos desenvolvemos en Bustillo Abogados, apreciamos un incremento importante de operaciones con respecto a años anteriores impulsado principalmente por una mayor facilidad de financiación y el afán por mejorar la cuota de mercado y el posicionamiento geográfico, fundamentalmente a través de la adquisiciones en tecnología o innovación. Tras muchos años complicados para las empresas, éstas tratan ahora de potenciar un crecimiento inorgánico con el objetivo de fortalecer su posicionamiento estratégico. También es importante destacar un incremento en las valoraciones de las empresas que se encuentran en proceso de compra al encontrarse, en numerosas ocasiones, con diferentes oferta de compra. Esto se debe, además de por el mencionado acceso a la financiación, por una mejoría en las expectativas de rentabilidad dada la recuperación económica. No obstante, lo que resulta difícil es conocer por cuanto tiempo se podrá mantener esta tendencia alcista.

TTR: Más de la mitad de las operaciones asesoradas por Bustillo Abogados en lo que va de año son operaciones de Venture Capital. ¿Cree usted que el universo startup en España tiene margen de crecimiento o ya hemos alcanzado el cénit?

J.B.G.: El universo startup en España madura a un ritmo muy rápido aunque aún estamos lejos de otros países que nos llevan unos años de ventaja en cuanto a generar nuevas tendencias, innovación o conocimiento. Vemos un claro acercamiento de las grandes y medianas empresas a la innovación mediante la adquisición de startups que les permiten, entre otras cosas, incorporar una tecnología innovadora o acelerar el proceso de transformación digital. Aunque crece la cuantía en las operaciones de mayor tamaño, la mayoría siguen siendo de un tamaño moderado en comparación con otros países europeos, unas diferencias que, desde mi punto de vista, se irán reduciendo al considerar la buena labor que se está haciendo en el ecosistema tecnológico español.

TTR: Tras una etapa de ideas innovadoras, ¿diría usted que cabe esperar más ideas disruptivas, o que las nuevas startups que surjan basarán su desarrollo en la mejora o en la competencia de proyectos existentes?

J.B.G.: La industria tecnológica se reinventa constantemente buscando ofrecer productos y servicios innovadores que tratan de dar respuesta a las necesidades que se generan en nuestra sociedad como esta ocurriendo ahora con blockchain por poner un ejemplo. En un mundo en constante evolución, cada día surgen nuevas ideas que tratan de aprovechar las oportunidades empresariales y ocupar los huecos existentes en el mercado en áreas y sectores de lo más variado. En este escenario, muchas de las startups que nacen, buscan simplificar procesos y trabajos que puedan resultar complicados o tediosos en la actualidad. Sin embargo, no podemos obviar tampoco que muchas de ellas nos acercan a realidades que antes eran impensables como la inteligencia artificial o las realidades mixtas, lo que a su vez, genera nuevas inquietudes y deseos a los que será necesario responder. Es por ello que estoy convencido de que los emprendedores aún tienen mucho con lo que sorprendernos y revolucionar nuestras vidas.

TTR: Y desde el punto de vista de los inversores, además de los fondos tradicionales que llevan varios años operando en España, de los numerosos Business Angels existentes, y de la apuesta por inversiones de Venture Capital que están llevando a cabo determinadas entidades bancarias, ¿hay cabida para nuevos players de mercado?

J.B.G.: Desde mi percepción, se está extendiendo con fuerza el formato de Capital Riesgo Corporativo, donde las empresas que han tenido algún contacto previo con startups ya sea mediante adquisiciones, aceleradoras de proyectos de startups, incubadoras u otras deciden incrementar su compromiso y establecer su propia estructura de inversión. Las empresas más emblemáticas de España llevan tiempo desarrollando esta estrategia si bien es cierto que ahora se percibe un movimiento en las empresas no cotizadas que también buscan profesionalizar sus inversiones. El rápido avance de la tecnología y su impacto tan directo en casi todos los modelos de negocio que conocemos está obligando a las empresas a estar vigilantes ante posibles disrupciones en su industria. El establecimiento de un Capital Riesgo Corporativo permite a las empresas analizar, seleccionar e invertir en un elevado número de startups que puedan ser de su interés, ya sea por una tecnología determinada, porque amplían la cartera existente de productos o servicios o simplemente para mejorar procesos internos de trabajo, pudiendo adquirir solo aquellas que realmente sean determinantes para su negocio.

TTR: ¿Cree usted, por lo tanto, que asistiremos a una especialización más acusada por sectores de los nuevos players que puedan surgir? Si las grandes empresas comienzan a habilitar áreas de inversión en Venture Capital a nivel interno, ¿podría darse el caso de que el criterio de inversión se basase más en el desarrollo de una determinada tecnología necesaria para la empresa que en la rentabilidad económica del proyecto? ¿Podría entenderse esto como un paso intermedio entre desarrollo interno de tecnología y externalización?

J.B.G.: Ese es justo el punto de inflexión en el formato de Capital Riesgo Corporativo dado que ya no se busca únicamente rentabilidad en términos económicos sino que en muchos casos, dichas inversiones vienen promovidas por razones estratégicas, de negocio, de innovación o de recursos humanos. Hace unas décadas la innovación nacía siempre en los departamentos de I+D de las grandes empresas dado el alto volumen de inversión requerido y los largos procesos de creación pero el abaratamiento y el acceso a la computación ha permitido trasladar la innovación a cualquier persona con acceso a internet por lo que las empresas deben también cambiar el cómo y el dónde invierten para innovar.