Entrevista con Pablo Perezalonso, miembro de Ritch Mueller desde 1994 y socio desde 2000. Fue nombrado socio administrador en el 2017. Perezalonso se especializa en operaciones bursátiles, operaciones internacionales bancarias y de financiamiento, temas regulatorios, derivados y mercados de capitales.

Entrevista con Pablo Perezalonso, miembro de Ritch Mueller desde 1994 y socio desde 2000. Fue nombrado socio administrador en el 2017. Perezalonso se especializa en operaciones bursátiles, operaciones internacionales bancarias y de financiamiento, temas regulatorios, derivados y mercados de capitales.

A grandes rasgos ¿Cuál es su valoración general respecto a la marcha del mercado de M&A mexicano durante los primeros meses del año?

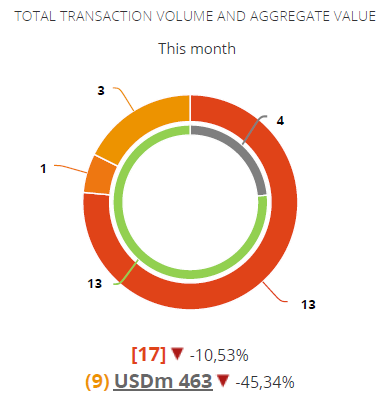

Los primeros meses del año han sido bastante buenos considerando las expectativas por el año electoral, la renegociación de NAFTA y los efectos de las políticas de Trump en la economía mexicana. Es pronto para tener conocimiento de las operaciones registradas hasta mayo, pero según fuentes consultadas, en los primeros 3 meses del año, se registraron 72 fusiones y adquisiciones, contra 61 durante el mismo periodo en el año 2017. Es decir, un incremento del 18%.

Según nuestros registros, el sector financiero y de seguros ha ganado protagonismo en cuanto al volumen de sus operaciones de M&A en comparación con las cifras del mismo periodo en ejercicios anteriores. ¿A qué cree que se debe este incremento? ¿Opina que manifiesta una tendencia?

No consideramos que se deba a algo en particular. Si bien 2017 no fue un año particularmente con muchas transacciones en este sector, 2016 sí lo fue, fue la segunda mayor industria en número de operaciones. Con la nueva Ley para Regular a las Instituciones de Tecnología Financiera (Ley Fintech), consideramos que veremos más inversiones en empresas de tecnología en este sector. Hemos visto algunas operaciones de venta de bancos extranjeros, pero entendemos que esto se debe a temas de organización interna y no a la situación política y económica.

Otro de los sectores más activos en el mercado mexicano es el inmobiliario ¿Podría brindarnos una breve previsión del funcionamiento de dicho sector en 2018?

En el sector inmobiliario empezamos a ver que ciertos clientes están tomando una posición más conservadora respecto de nuevos proyectos hasta que pasen las elecciones y se defina la negociación de NAFTA. En cuanto a proyectos que ya están en marcha seguimos viendo un gran dinamismo en el sector de vivienda y en la parte de logística. En cuando a la parte comercial sigue habiendo mucha actividad aunque en algunos mercados ya estamos viendo una desaceleración en la parte comercial. Por lo que respecta a la parte de oficinas, sobre todo en la Ciudad de México, empezamos a observar un mercado un poco saturado y donde la absorción es más lenta.

En lo que llevamos de año, según nuestros datos, México parece reflejar un creciente interés por las operaciones de inversión en el extranjero. ¿Cuáles cree que pueden ser los motivos? ¿Cree que será una pauta que se mantendrá a lo largo del año?

No lo hemos notado particularmente, pero seguramente se debe a inversionistas buscando seguridad en tanto se define la situación política y la renegociación de NAFTA.

En último lugar, en cuanto a las operaciones de venture capital en el país, ¿cuál cree que es la situación actual de esta área de mercado en México? ¿Qué pronóstico le daría para este ejercicio?

Hemos participado en bastantes operaciones en estos primeros meses, pero también hemos visto como varios proyectos están a la espera de que se resuelva la situación política y económica.