Deal Tracker

www.TTRecord.com

LATIN AMERICA

|

BRAZIL: North American appetite for deals on the rise

Acquisitions by North America buyers increased by around 6% between January and August, 2015, compared to the same period in 2014, according to TTR data ( www.TTRecord.com). The growing appetite for Brazilian assets reverses a downward trend seen between the first eight months of 2013 and the corresponding period in 2014

CHILE: Financial services transactions brisk

Financial services transactions grew 40% in the first eight months of 2015 to 21 deals compared to 15 in the same period in 2014, according to TTR data ( www.TTRecord.com). Cross-border financial services deals are up 150% over the same period.

|

Rankings / League Tables

|

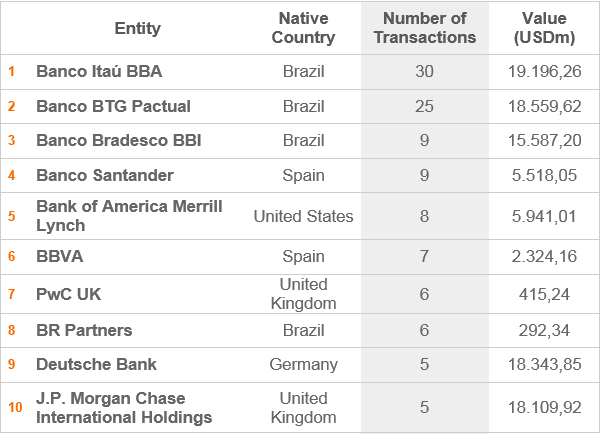

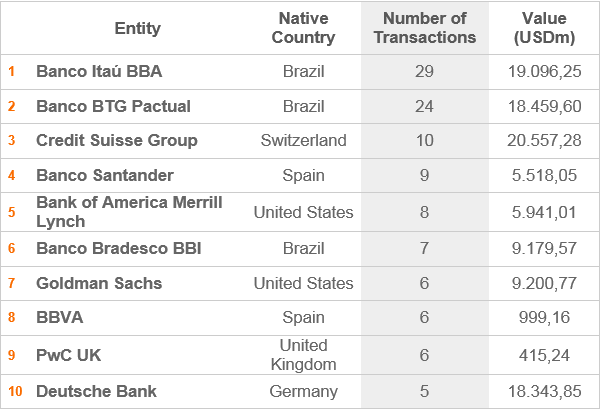

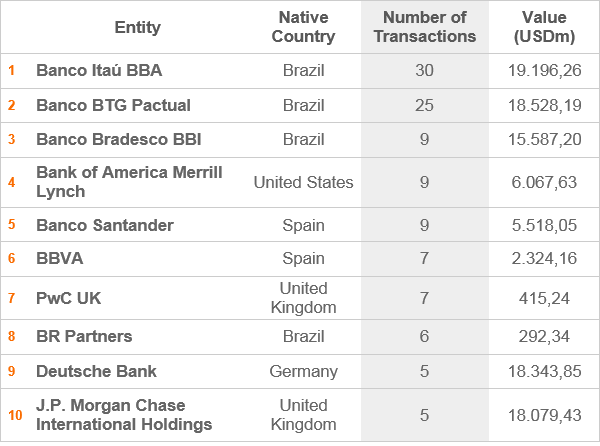

Latin America Ranking – 2015

Financial Advisory – Year to Date (YTD)

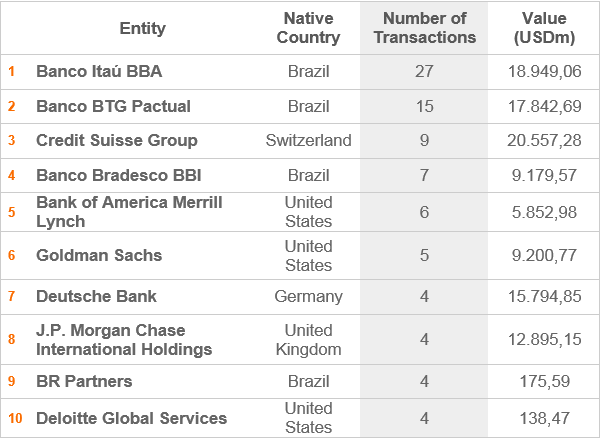

Banco Itaú BBA leads TTR’s Latin America financial advisory ranking at the close of August after advising on 30 transactions worth nearly USD 19.2bn combined. Brazil’s leading bank also led the ranking for the first eight months of 2014, when it’d advised on 47 deals together worth USD 8bn. Banco BTG Pactual follows in second place, as it did a year ago, with 25 transactions under its belt, together worth USD 18.5bn, compared to 27 deals worth USD 10.3bn in the first eight months of 2014. In third place by deal volume, Banco Bradesco BBI closed nine deals by the end of August, worth just under USD 15.6bn in aggregate, up from fifth for the same period in 2014 when it’d closed 10 deals worth USD 4.7bn. BAML and Santander are tied with Bradesco by deal volume, falling into fourth and fifth place, weighted by combined deal value of USD 6bn and USD 5.5bn, respectively. BAML fell from third place in the ranking at this point last year, and Santander from fourth, when both banks had advised on 11 deals. BBVA, in sixth place, and PwC in seventh, have both advised on seven transactions YTD, BR Partners six and Deutsche Bank and JPMorgan five apiece. Of the trailing five in the chart, only Deutsche Bank was among the top 10 in the first eight months of 2014.

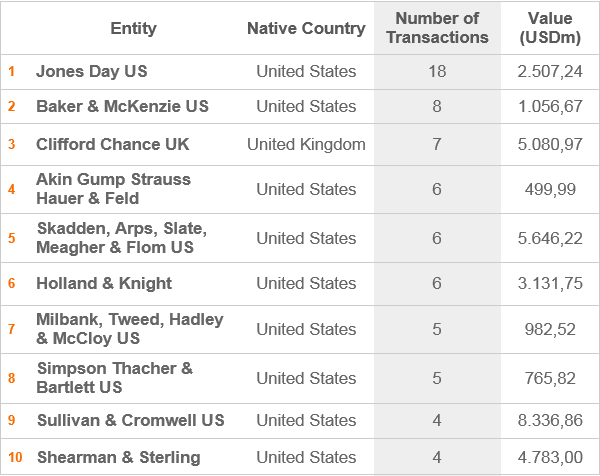

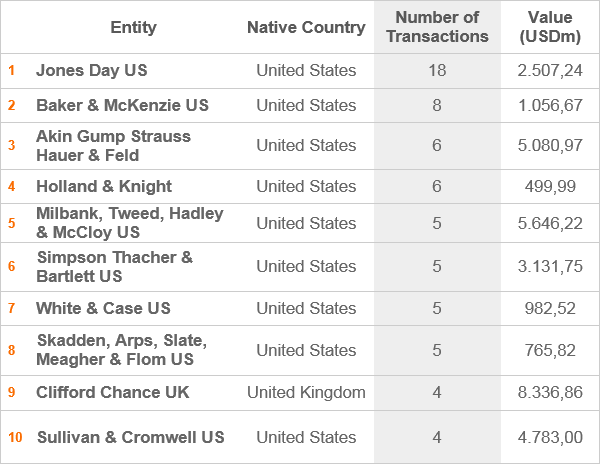

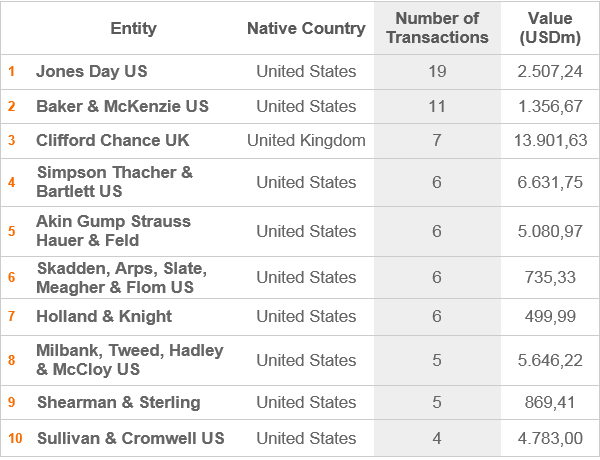

Legal Advisory – Year to Date (YTD)

Legal Advisory – Year to Date (YTD)

Legal Advisory – Year to Date (YTD)

Jones Day dominates the international firms in TTR’s Latin America legal advisory ranking at the close of August after advising on 19 transactions YTD together worth USD 2.5bn. The top firm climbed from third for the corresponding period last year, when it’d advised on 12 deals worth USD 1.9bn. Baker & McKenzie fell from first at this time last year to close August in second place with 11 transactions YTD worth nearly USD 1.4bn combined. Clifford Chance places third by volume, but first in value terms by a long shot, with seven deals worth USD 13.9bn combined. Clifford was not among the top-10 firms by deal volume in the first eights months of 2014. Simpson Thacher & Bartlett placed fourth, with six deals together worth USD 6.6bn, falling from second a year ago when it had advised on 13 deals worth USD 6.5bn combined. Following, also with six deals in their hats, are Akin Gump Strauss Hauer & Feld, alongside Skadden, Arps, Slate, Meagher & Flom, and Holland & Knight, of which only the first firm broke the USD 1bn mark, advising on deals worth USD 5bn in aggregate. Milbank, Tweed, Hadley & McCloy follows in eighth for its five deals worth USD 5.6bn combined. Shearman & Sterling takes ninth, also with five deals, and Sullivan & Cromwell brings up the rear with four deals worth nearly USD 4.8bn in aggregate. ç

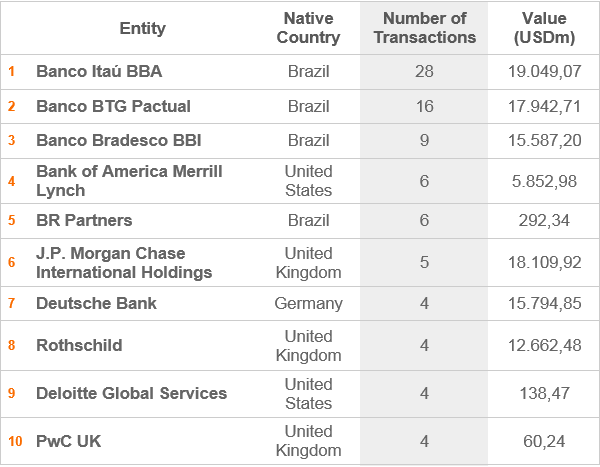

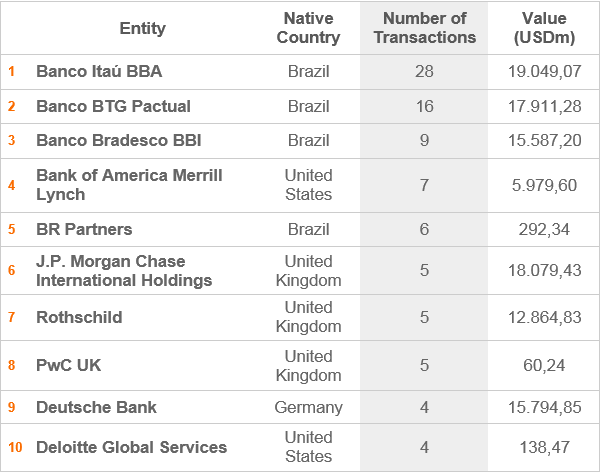

Brazil Ranking – 2015

Financial Advisory – Year to Date (YTD)

Banco Itaú BBA dominates TTR’s Brazil financial advisory ranking at the close of August, with 28 deals worth a combined USD 19bn, leading its peers as it did a year ago when the bank had advised on 37 transactions worth just shy of USD 4bn. BTG Pactual follows in second, with 16 advisory mandates YTD, together worth USD 17.9bn. At the close of August, 2014, BTG Pactual had advised on 23 transactions worth USD 9.3bn and also ranked second. Banco Bradesco BBI climbed from fourth a year ago to close August ranked third, despite a slight decline in deal flow from 11 to nine transactions. Fewer deals were worth more, however: USD 15.6bn YTD in 2015 compared to USD 4.7bn in the first eight months of 2014. BAML placed fourth in the Brazil chart, with seven deals worth USD 6bn in total, ahead of BR Partners, with six deals worth USD 292m. JPMorgan, Rothschild and PwC each have advised on five transactions in Brazil, worth USD 18bn, 12.9bn and USD 60m, respectively. Neither BAML, JPMorgan nor Rothschild placed among the top 10 by the close of August, 2014. PwC climbed two rungs from its tenth-place position at this point last year when its four transactions were together worth USD 834m. Deutsche Bank and Deloitte Global Services have advised on four deals each, YTD, worth USD 15.8bn combined in the case of the former, and USD 138m in the latter. Deutsche Bank and Deloitte too were absent from the top 10 at the close of August, 2014.

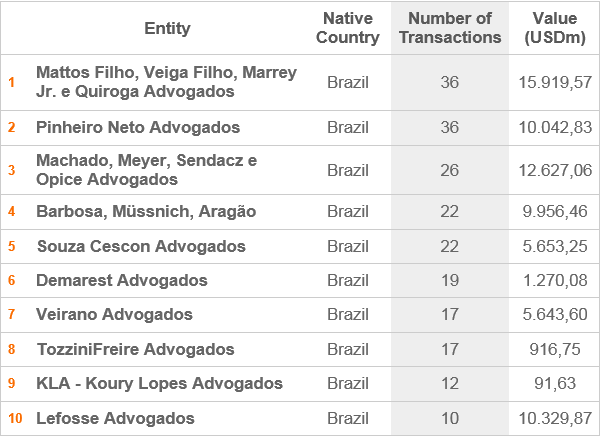

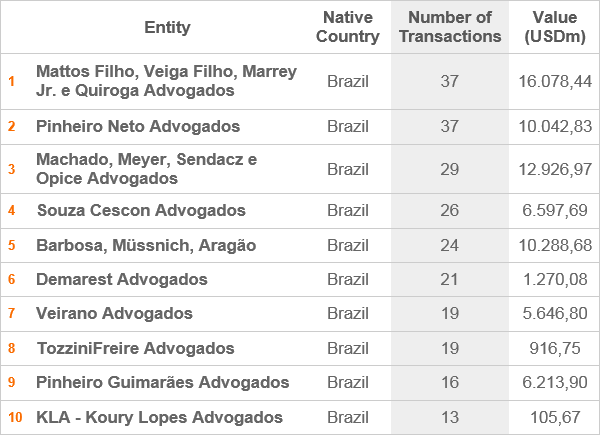

Legal Advisory – Year to Date (YTD)

The competition couldn’t get any fiercer in TTR’s Brazil legal advisory ranking between Mattos Filho, Veiga Filho, Marrey Jr. e Quiroga Advogados and Pinheiro Neto Advogados, each with 37 mandates under their belts, together worth USD 16bn and USD 10bn, respectively. The relative positions were much the same between Brazil’s top two firms at the close of August, 2014 when Mattos Filho had advised on 43 deals and its rival 40, worth USD 8.6bn and USD 6.5bn, respectively. Machado, Meyer, Sendacz e Opice Advogados inched up to third from fourth at this point last year, meanwhile, with 29 mandates YTD worth USD 12.9bn, compared to 31 worth USD 2.2bn a year ago, a 475% jump in combined deal value notwithstanding a 6% drop in volume. Souza, Cescon Advogados inched up from sixth a year ago when it’d advised on 24 deals worth USD 11bn to close August in fourth place with 26 deals under its belt worth USD 6.6bn combined. Barbosa, Müssnich, Aragão climbed from ninth to fifth with 24 transactions worth USD 10.3bn YTD compared to 19 worth USD 4.9bn in the eight-month period that ended 31 August, 2014. Demarest is up 5% by deal volume, enough to climb the chart from eighth to sixth, after advising on 21 deals worth just under USD 1.3bn in aggregate. The firm’s combined deal value fell 40%, however, compared to its 20 deals worth USD 2.1bn a year ago. Veirano has retained the seventh-place position it held at the close of August, 2014, with 19 mandates YTD worth USD 5.6bn combined. Also with 19 deals under its belt, TozziniFreire Advogados fell three spots from fifth to eighth. It’d advised on 27 deals in the eight-month period ending 31 August, 2014, representing a 30% decline in deal volume, while combined deal value declined 73% from USD 3.4bn then to USD 917m YTD in 2015. Pinheiro Guimarães Advogados appears at ninth, with 16 transactions worth USD 6.2bn in aggregate. The firm wasn’t among the top-10 in Brazil at the close of August, 2014. Koury Lopes Advogados brings up the rear, as it did a year ago, with 13 deals worth USD 106m combined compared to 16 worth USD 1.4bn at the end of August, 2014, representing a 19% decline in volume and a 92% drop in aggregate value.

Mexico Ranking – 2015

Financial Advisory – Year to Date (YTD)

BBVA and Pablo Rión y Asociados are neck and neck at the top of TTR’s Mexico financial advisory ranking, in first and second place with four transactions apiece, together worth USD 2bn and USD 81m, respectively, insomuch as deal values have been disclosed. BBVA doubled its deal volume compared to its position a year ago when it placed sixth in the chart. Spanish rival Banco Santander holds third place in the chart, with three transactions together worth USD 864m, compared to one worth USD 1.3bn a year ago when it placed tenth. The fourth-to-eighth place investment banks advised on two transactions each, led by Alfaro, Dávila y Ríos whose pair of transactions is worth USD 2.2bn. Deutsche Bank and Citigroup hold the ninth- and tenth-place positions, with deals valued at USD 2.5bn and USD 1.2bn, respectively. Citigroup placed second and Deutsche Bank third in the corresponding period of 2014, with two deals worth USD 1.7bn together in the case of the former, and two worth USD 1.5bn in the latter.

Legal Advisory – Year to Date (YTD)

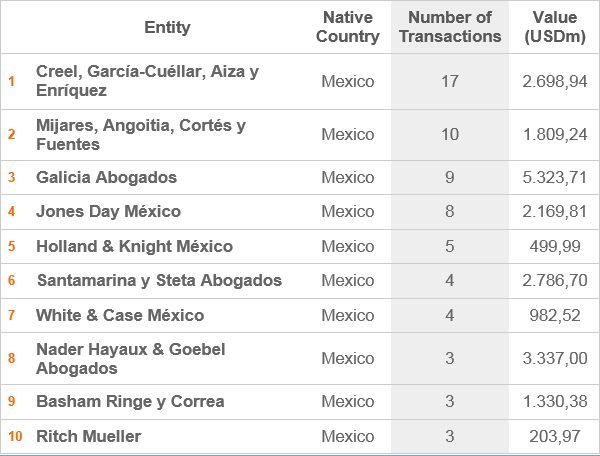

Creel, García-Cuéllar, Aiza y Enríquez have a comfortable lead in TTR’s Mexico legal advisory ranking, as the firm did in the first eight months of 2014. Creel leads despite a 10% decline in deal volume to 18 transactions YTD worth USD 6.2bn combined, and a 28% drop in aggregate value relative to its 20 deals worth USD 8.6bn at the close of August, 2014. Mijares, Angoitia, Cortés y Fuentes holds firm to second place in the ranking, with 13 deals together worth USD 3.1bn compared to the 12 worth USD 2.4bn that garnered it second place a year ago. Galicia Abogados rose three rungs from sixth to take third with 10 deals together worth USD 5.3bn compared to half that number worth 1bn at the close of August, 2014. Jones Day holds fourth place in the chart by deal volume with eight transactions and second by combined value of USD 5.3bn. The US-based firm didn’t place among the top 10 law firms practicing in Mexico in the first eight months of 2014. Nader Hayaux & Goebel Abogados, in fifth, and Holland & Knight, in sixth, have advised on five deals each YTD in 2015, the former leading the chart by combined deal value of USD 8.2bn, the latter lagging in the distance with USD 500m worth of transactions, in aggregate. Holland & Knight rose one spot in the ranking relative to its position at the end of August, 2014, while Nader Hayaux was not among the top 10 a year ago. Santamarina y Steta Abogados, at seventh, advised on four deals in the first eight months of the year, together worth USD 2.8bn, and is tied by volume with Basham Ringe y Correa, also with four transactions, in its case worth USD 1.3bn. Basham also ranked in eighth place for the January-August period in 2014. Ritch Mueller fell precipitously, from third to ninth with three deals YTD worth USD 204m, compared to eight a year ago worth USD 2.8bn, representing a 62.5% decline in volume and a 93% decline in aggregate value. White & Case, also with three transactions under its belt YTD, has met with a similar 50% decline in deal volume and an 88% decline in combined deal value to USD 83m, relative to its performance in the first eight months of 2014, when it’d advised on six deals together worth USD 686m.